Chapter 10 — Unit Roots and Differencing

In previous chapters, we studied:

persistence

stationarity

autocorrelation

A central question now arises:

The answer lies in the concept of a unit root.

This has major consequences:

standard regression methods may fail

forecasting becomes difficult

statistical inference can be misleading

transformation (differencing) becomes necessary

This chapter introduces:

unit root intuition

random walks revisited

differencing

detrending vs differencing

the Augmented Dickey–Fuller (ADF) test

Learning Objectives¶

By the end of this chapter, you should be able to:

understand what a unit root is

explain why random walks are nonstationary

distinguish stationary and unit root processes

difference a time series

distinguish detrending from differencing

interpret the ADF test intuitively

10.1 Persistence Revisited¶

Recall the random walk:

where:

Each new observation equals:

the previous value

plus a random shock

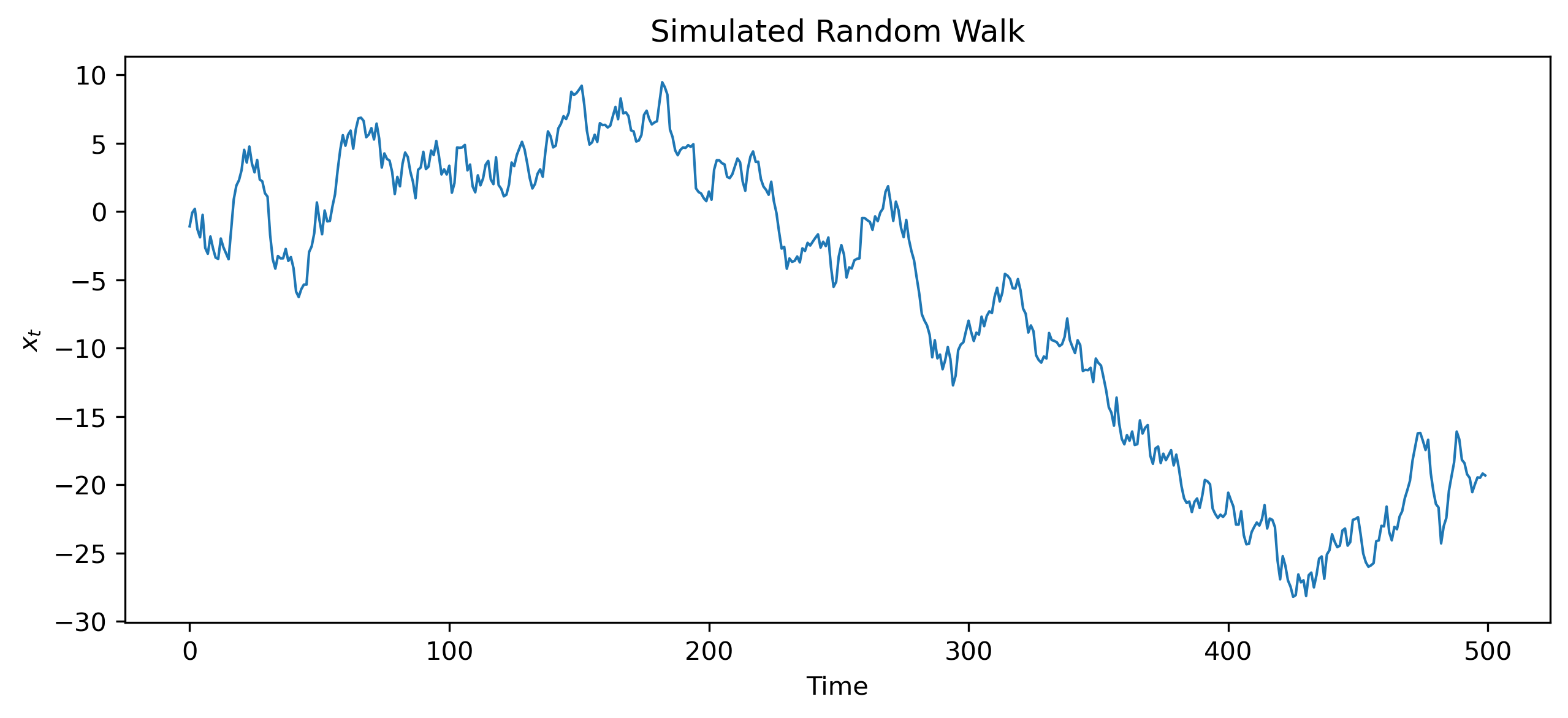

10.2 Simulating a Random Walk¶

Python Code

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(123)

w = np.random.normal(0, 1, 500)

x = np.cumsum(w)

plt.figure(figsize=(10,4))

plt.plot(x, lw=1)

plt.title("Simulated Random Walk")

plt.xlabel("Time")

plt.ylabel("$x_t$")

plt.savefig("figs/ch7/rw.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

10.3 Why Random Walks Matter¶

Random walks are central in economics and finance.

Examples include:

stock prices

exchange rates

some macroeconomic aggregates

The random walk model implies:

strong persistence

unpredictable long-run movement

permanent effects of shocks

10.4 The Unit Root Idea¶

The random walk can be rewritten as:

with:

10.5 Why the Unit Root Matters¶

Consider:

Case 1: ¶

shocks gradually disappear

the series returns toward a stable mean

the process is stationary

Case 2: ¶

shocks never disappear

the series accumulates past shocks

the process becomes nonstationary

10.6 Stationary vs Unit Root Processes¶

Stationary Process¶

stable mean

stable variance

temporary shocks

Unit Root Process¶

drifting behavior

growing variance

permanent shocks

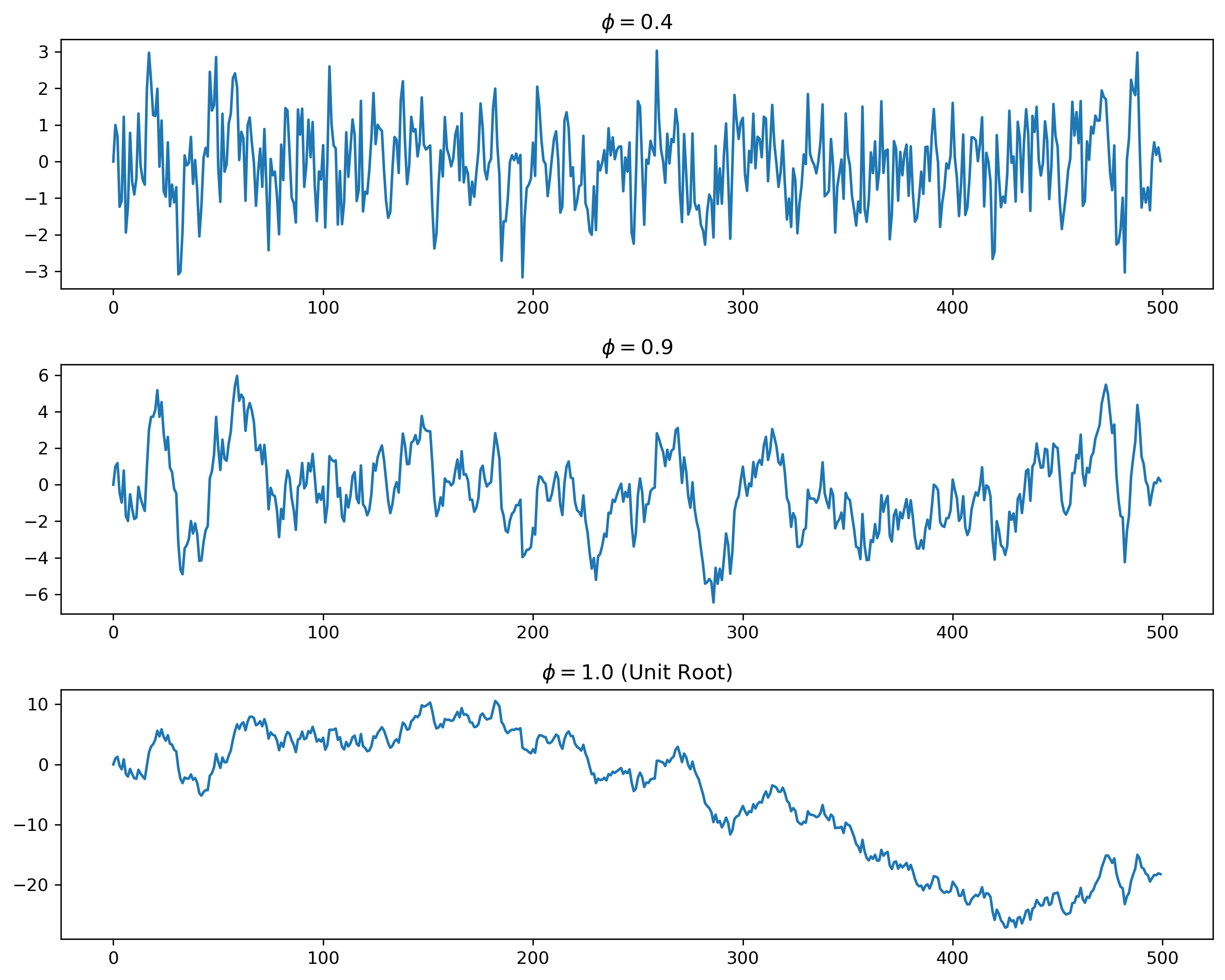

10.7 Simulating Different Levels of Persistence¶

Source

np.random.seed(123)

n = 500

w = np.random.normal(0,1,n)

x1 = np.zeros(n)

x2 = np.zeros(n)

x3 = np.zeros(n)

phi1 = 0.4

phi2 = 0.9

phi3 = 1.0

for t in range(1,n):

x1[t] = phi1*x1[t-1] + w[t]

x2[t] = phi2*x2[t-1] + w[t]

x3[t] = phi3*x3[t-1] + w[t]

fig, ax = plt.subplots(3,1, figsize=(10,8))

ax[0].plot(x1)

ax[0].set_title(r"$\phi = 0.4$")

ax[1].plot(x2)

ax[1].set_title(r"$\phi = 0.9$")

ax[2].plot(x3)

ax[2].set_title(r"$\phi = 1.0$ (Unit Root)")

plt.tight_layout()

plt.savefig("figs/ch10/ar-sim.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

10.8 Differencing¶

A common way to remove unit roots is differencing.

10.9 Differencing a Random Walk¶

For a random walk:

Taking first differences:

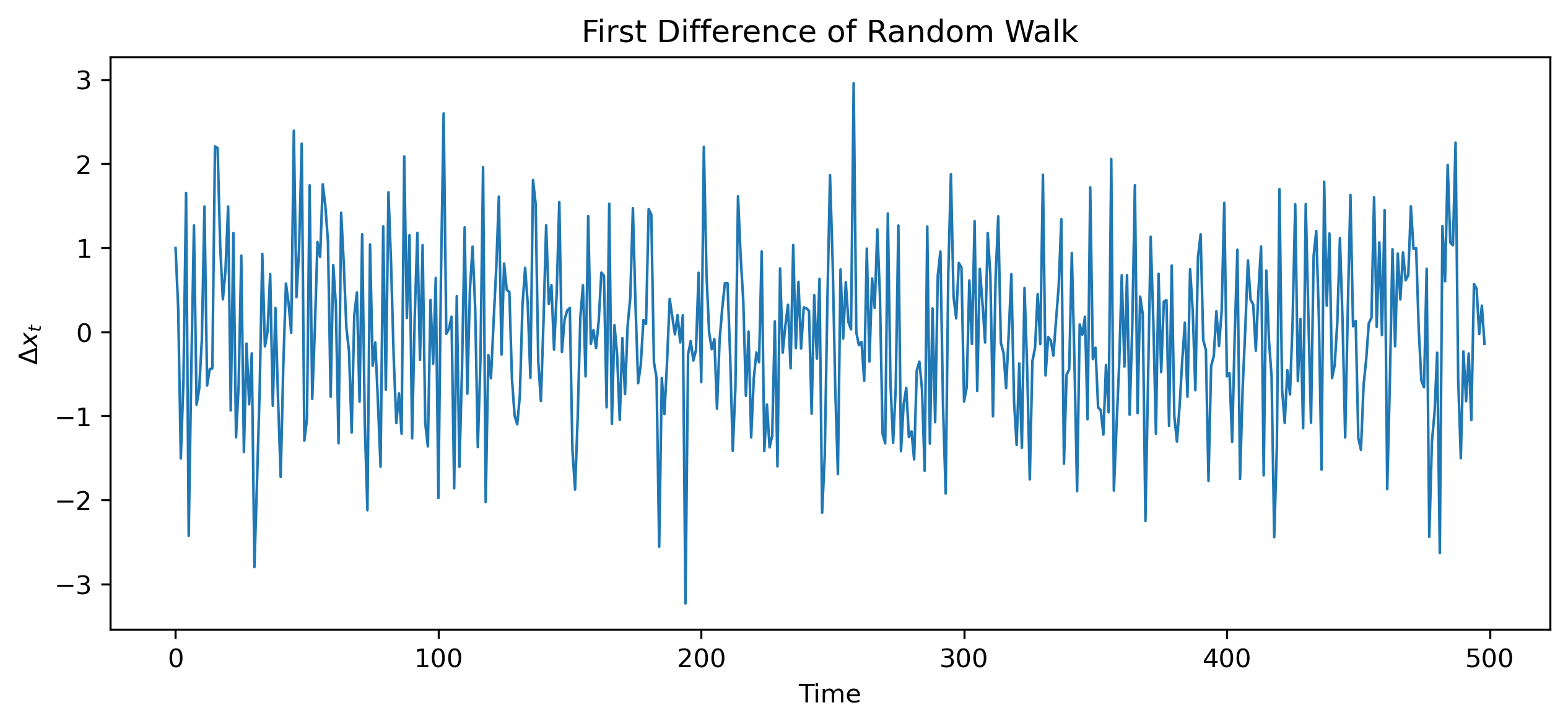

10.10 Simulating Differencing¶

dx = np.diff(x)

plt.figure(figsize=(10,4))

plt.plot(dx, lw=1)

plt.title("First Difference of Random Walk")

plt.xlabel("Time")

plt.ylabel(r"$\Delta x_t$")

plt.savefig("figs/ch10/rw-diff.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

10.11 Integrated Processes¶

A unit root process is said to be integrated of order one.

Example¶

| Series | Order |

|---|---|

| White noise | |

| Random walk |

10.12 Detrending vs Differencing¶

Nonstationarity may arise for different reasons.

Deterministic Trend¶

Suppose:

where is stationary.

Removing the trend may produce stationarity.

Stochastic Trend¶

For a random walk:

detrending alone is insufficient.

Differencing is required.

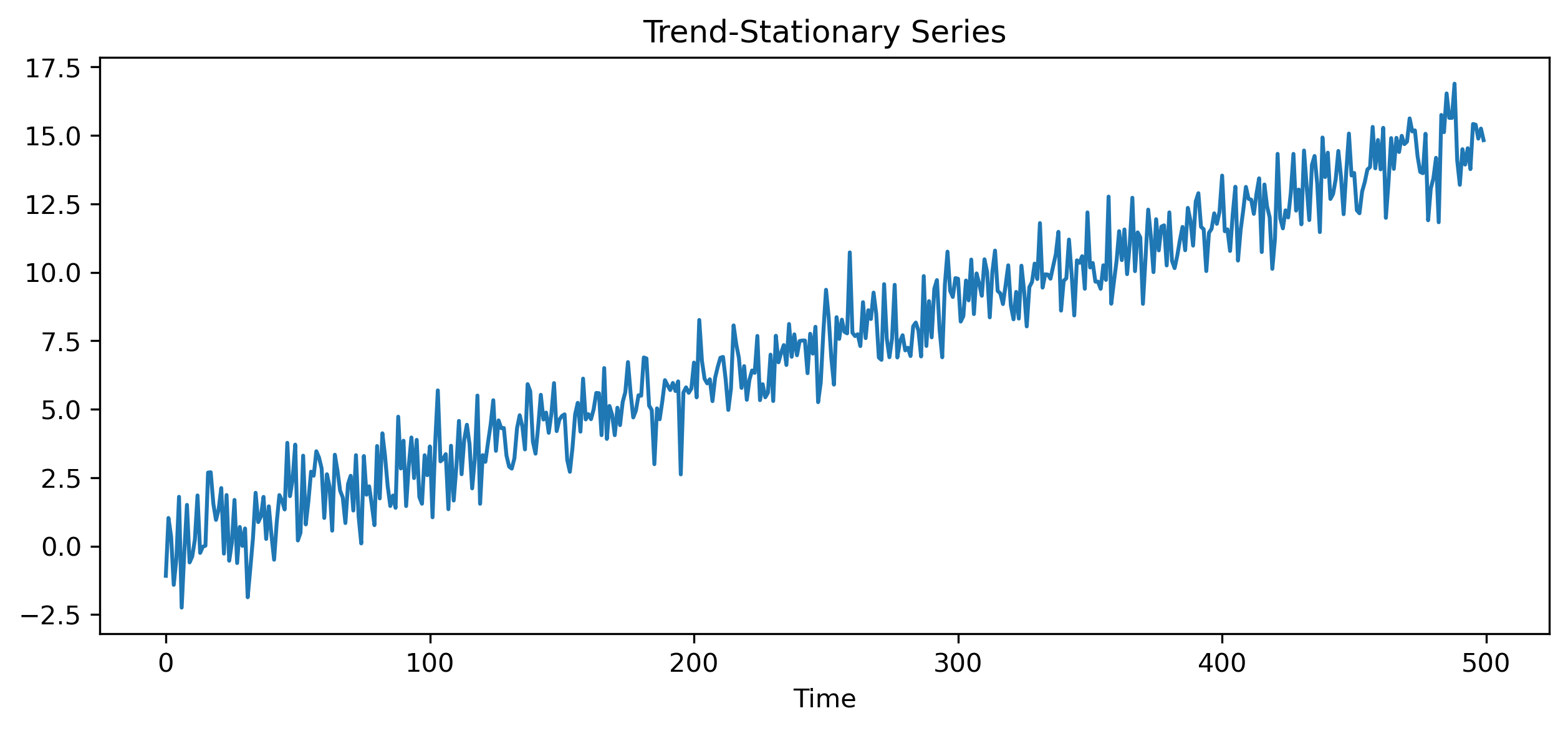

10.13 Visual Comparison¶

Source

np.random.seed(123)

t = np.arange(500)

trend_stationary = 0.03*t + np.random.normal(0,1,500)

plt.figure(figsize=(10,4))

plt.plot(trend_stationary)

plt.title("Trend-Stationary Series")

plt.xlabel("Time")

plt.savefig("figs/ch10/trend.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

10.14 Why Unit Roots Matter¶

Unit roots affect:

forecasting

inference

regression

model selection

This problem becomes central later in:

spurious regression

cointegration

ECM models

10.15 The Dickey–Fuller Test¶

We now need a way to test for unit roots.

Consider:

Subtract from both sides:

or:

where:

Hypotheses¶

10.16 Augmented Dickey–Fuller (ADF) Test¶

Real-world data often exhibit serial correlation.

The Augmented Dickey–Fuller (ADF) test extends the Dickey–Fuller test by including lagged differences:

10.17 Interpreting the ADF Test¶

Reject ¶

evidence against a unit root

series likely stationary

Fail to Reject ¶

insufficient evidence against a unit root

series may be nonstationary

10.18 ADF Testing in Gretl¶

Menu¶

Variable → Unit root tests → Augmented Dickey-FullerTypical Steps¶

Choose variable

Include constant and/or trend if appropriate

Select lag length

Interpret test statistic and p-value

[GRETL Screenshot Placeholder: ADF test dialog][GRETL Screenshot Placeholder: ADF test output]10.19 KPSS Test (Optional)¶

The KPSS test reverses the hypotheses.

KPSS Hypotheses¶

10.20 Looking Ahead¶

In this chapter, we introduced:

unit roots

differencing

ADF testing

We are now ready to build formal stochastic models for stationary time series.

In the next chapters, we study:

autoregressive (AR) models

moving average (MA) models

ARMA and ARIMA models

Key Takeaways¶

Concept Check¶

Basic¶

What is a unit root?

What does it mean for a time series to be nonstationary?

What is a random walk?

Intuition¶

Why do shocks have permanent effects in a unit root process?

Why does a random walk not return to a stable level?

Why is nonstationarity problematic for modeling?

Intermediate¶

What is the purpose of differencing a time series?

What is the difference between:

a stationary process

a unit root process

What is the difference between:

deterministic trend

stochastic trend

Finance Insight¶

Why are stock prices often modeled as random walks?

Why are returns typically stationary?

Challenge¶

Suppose a series becomes stationary after differencing once.

What does this imply about the original series?

Interpretation & Practice¶

A time series shows a strong upward trend and does not return to a stable level.

What does this suggest?

What might be an appropriate transformation?

A series appears to “wander” over time.

What type of process might this be?

What does this imply about shocks?

After differencing, a series fluctuates around zero.

What does this suggest?

Why is this useful?

A regression between two trending series shows a strong relationship.

Why might this be misleading?

What concept does this illustrate?

A series has a deterministic upward trend.

Would differencing or detrending be more appropriate?

Why?

Finance Interpretation¶

A stock price series is nonstationary.

Why is modeling prices directly problematic?

Why are returns preferred?

A return series appears stable over time.

What does this suggest?

Why is this important?

Challenge¶

Suppose you difference a stationary series.

What might happen?

Why is over-differencing a problem?

Numerical Practice¶

Random Walk and Differencing¶

Suppose a random walk is defined as:

with:

shocks: 2, −1, 3, −2

Compute

Compute the first differences:

What do you observe?

What does this suggest?

Identifying Nonstationarity¶

Consider the series:

10, 12, 15, 19, 24

Does this appear stationary?

Compute the first differences

Does the differenced series look more stable?

Trend vs Difference¶

Suppose:

What type of trend is this?

Would differencing remove it?

What would the differenced series look like?

ADF Interpretation (Applied)¶

Consider the following output from an Augmented Dickey–Fuller (ADF) test:

Augmented Dickey-Fuller Test

Test Statistic: -1.85

p-value: 0.67

Lags Used: 2

Observations: 197

Critical Values:

1% level: -3.46

5% level: -2.88

10% level: -2.57What is the null hypothesis of the ADF test?

Compare the test statistic with the critical values.

Is the test statistic more negative than the 5% critical value?

Based on the p-value and test statistic:

Do you reject the null hypothesis?

What does this imply about the series?

What would you do next before modeling this series?

Second Example¶

Now consider:

Augmented Dickey-Fuller Test

Test Statistic: -3.25

p-value: 0.02

Lags Used: 1

Observations: 198

Critical Values:

1% level: -3.46

5% level: -2.88

10% level: -2.57Do you reject the null hypothesis at the 5% level?

What does this imply about stationarity?

Why might the test statistic be compared with critical values rather than relying only on the p-value?

Challenge¶

Suppose the test statistic is close to the critical value.

Why might conclusions be uncertain?

What additional checks could you perform?

Suppose you difference a series twice.

When might this be necessary?

What is the risk of doing this unnecessarily?

Suppose two nonstationary series are regressed on each other.

Why might the results be misleading?

What concept does this relate to?