Chapter 17 — Spurious Regression

In earlier chapters, we learned that many time series are nonstationary. We also saw that random walks can drift over time even when they are generated only by random shocks.

We now study one of the most important warnings in applied time series regression:

This problem is especially common when working with nonstationary data, such as random walks or trending variables.

Learning Objectives¶

By the end of this chapter, you should be able to:

explain what spurious regression means

understand why nonstationary series can produce misleading regression results

recognize warning signs such as high and persistent residuals

use residual diagnostics to detect problems

understand why differencing may solve the problem

distinguish spurious regression from cointegration

17.1 The Basic Problem¶

Suppose we regress one time series on another:

In ordinary regression analysis, a statistically significant might suggest that is related to .

But with time series data, especially nonstationary data, this conclusion can be misleading.

This is the problem of spurious regression.

The model may report:

high

statistically significant coefficients

convincing-looking results

But these are driven by shared trending behavior — not by a true economic relationship.

17.2 Why Nonstationarity Creates Trouble¶

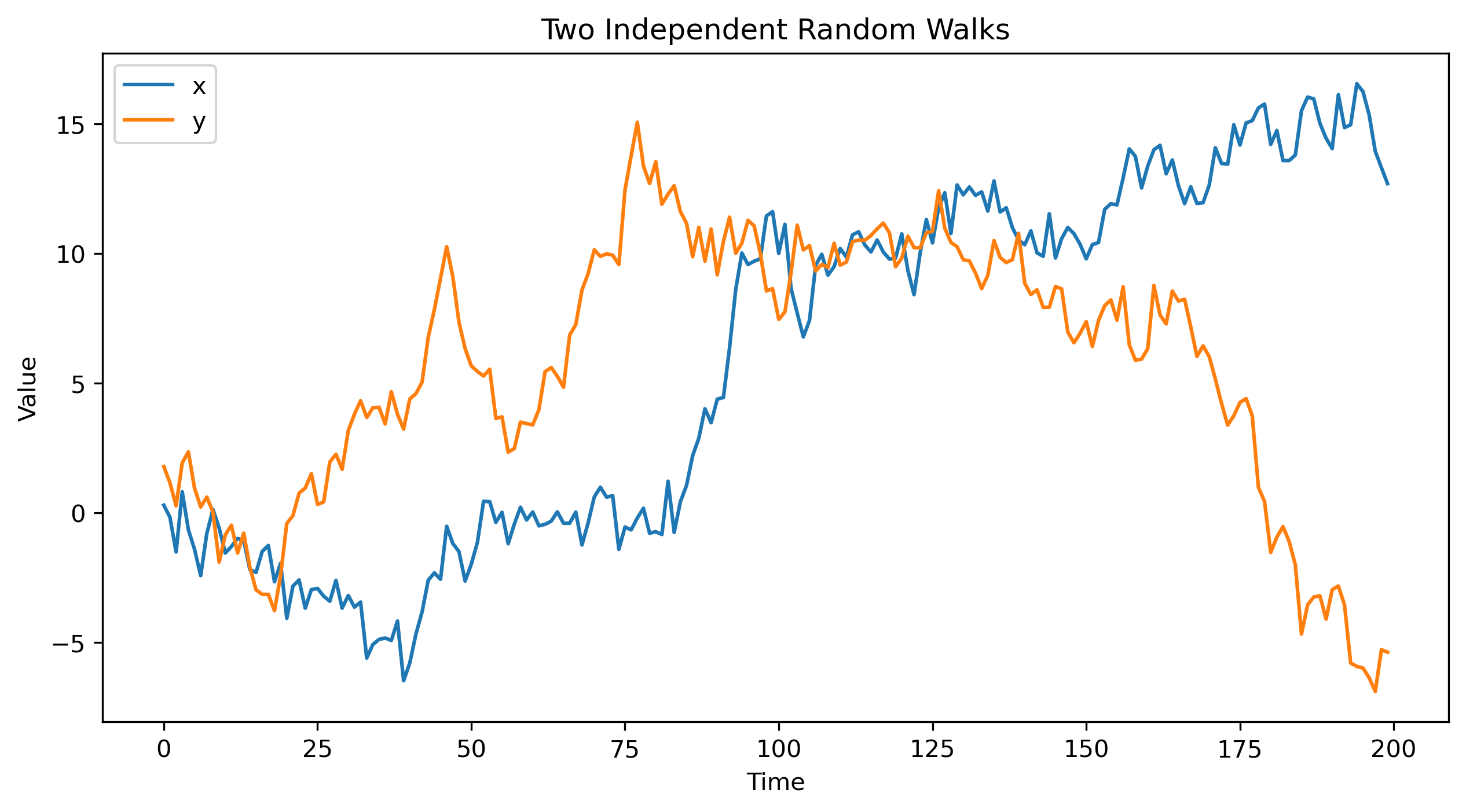

Consider two independent random walks:

and

where and are independent white noise processes.

By construction, there is no true relationship between and .

Yet both series may drift over time.

If two unrelated random walks drift in similar directions over a sample period, a regression may interpret that common movement as evidence of a relationship.

17.3 Symptoms of Spurious Regression¶

A spurious regression often produces:

high

significant t-statistics

low Durbin–Watson statistic

persistent residuals

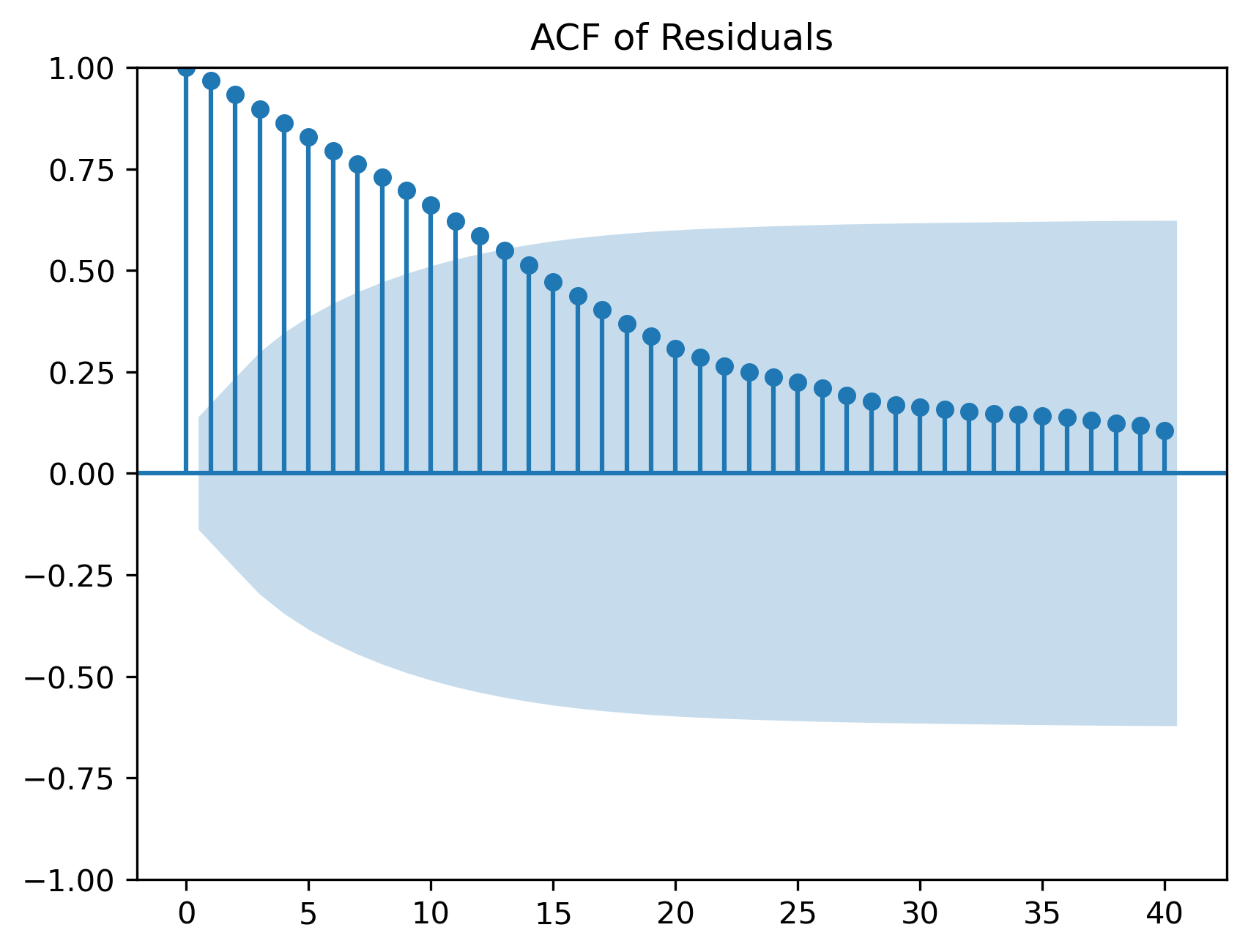

residual autocorrelation

This is one reason why time series regression requires additional diagnostic checks.

17.4 A Simple Simulation¶

Let us simulate two independent random walks.

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(124)

n = 200

u = np.random.standard_normal(n)

v = np.random.standard_normal(n)

x = np.cumsum(u)

y = np.cumsum(v)

plt.figure(figsize=(10, 5))

plt.plot(x, label="x")

plt.plot(y, label="y")

plt.title("Two Independent Random Walks")

plt.xlabel("Time")

plt.ylabel("Value")

plt.legend()

plt.savefig("figs/ch17/rw.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

17.5 Regressing One Random Walk on Another¶

Now regress on :

import statsmodels.api as sm

X = sm.add_constant(x)

model = sm.OLS(y, X)

results = model.fit()

print(results.summary()) OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.001

Model: OLS Adj. R-squared: -0.004

Method: Least Squares F-statistic: 0.2312

Date: Wed, 29 Apr 2026 Prob (F-statistic): 0.631

Time: 14:10:42 Log-Likelihood: -607.38

No. Observations: 200 AIC: 1219.

Df Residuals: 198 BIC: 1225.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 5.4880 0.469 11.692 0.000 4.562 6.414

x1 0.0249 0.052 0.481 0.631 -0.077 0.127

==============================================================================

Omnibus: 15.351 Durbin-Watson: 0.038

Prob(Omnibus): 0.000 Jarque-Bera (JB): 16.030

Skew: -0.654 Prob(JB): 0.000330

Kurtosis: 2.538 Cond. No. 12.0

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.The output will often show a statistically significant coefficient, even though the two variables were generated independently.

This is the essence of spurious regression.

17.6 Why This Is Problematic¶

Both and are nonstationary random walks.

Standard regression inference relies on assumptions that are violated in this setting.

This can lead to:

misleading t-statistics

invalid p-values

false confidence in the estimated relationship

17.7 Residual Diagnostics¶

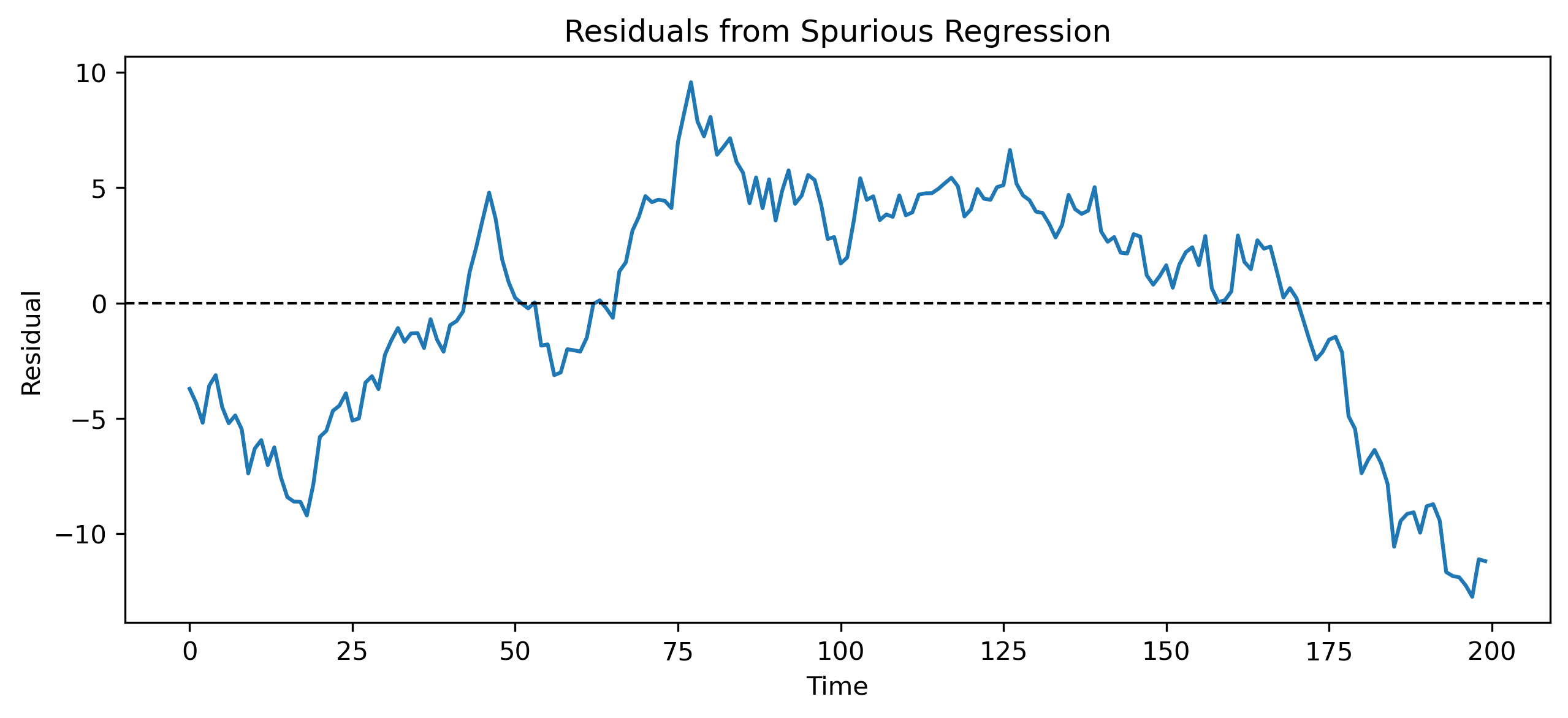

A key diagnostic is to examine the residuals.

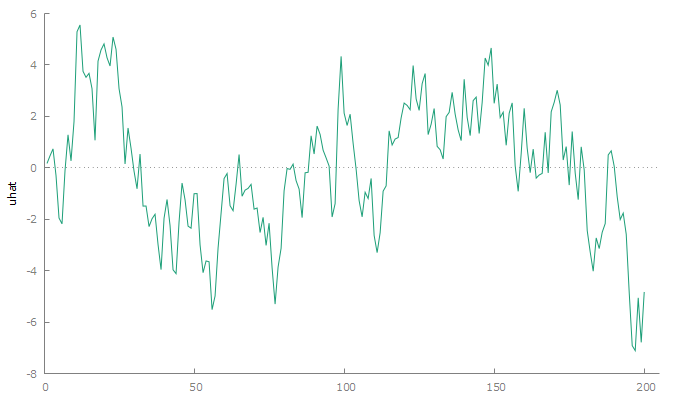

If a regression relationship is meaningful, the residuals should be stationary.

If the residuals remain nonstationary, the regression has not captured a stable relationship.

Residual Plot¶

uhat = results.resid

plt.figure(figsize=(10, 4))

plt.plot(uhat, linewidth=1.5)

plt.axhline(0, color="black", linestyle="--", linewidth=1)

plt.title("Residuals from Spurious Regression")

plt.xlabel("Time")

plt.ylabel("Residual")

plt.savefig("figs/ch17/res.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Residual ACF¶

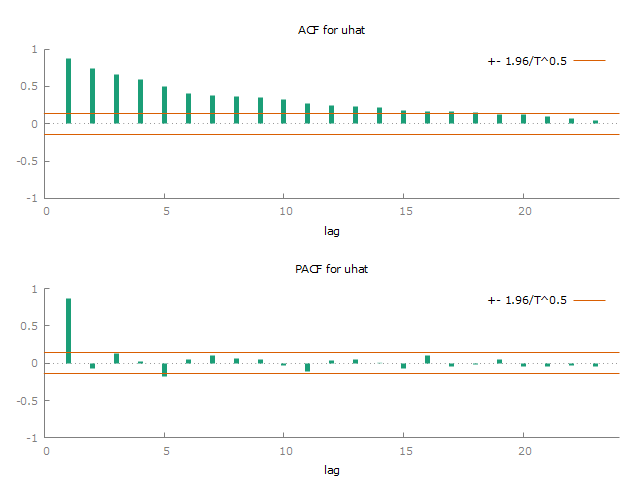

from statsmodels.graphics.tsaplots import plot_acf

plot_acf(uhat, lags=40)

plt.title("ACF of Residuals")

plt.savefig("figs/ch17/res_acf.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

17.8 Unit Root Testing¶

To formally check nonstationarity, we can perform unit root tests.

For the original series, we expect:

to be nonstationary

to be nonstationary

For a spurious regression, residuals are often nonstationary as well.

from statsmodels.tsa.stattools import adfuller

def adf_summary(series, name):

result = adfuller(series)

print(f"ADF test for {name}")

print(f"ADF statistic: {result[0]:.4f}")

print(f"p-value: {result[1]:.4f}")

print("Critical values:")

for key, value in result[4].items():

print(f" {key}: {value:.4f}")

print()

adf_summary(x, "x")

adf_summary(y, "y")

adf_summary(uhat, "residuals")ADF test for x

ADF statistic: -0.7378

p-value: 0.8367

Critical values:

1%: -3.4638

5%: -2.8763

10%: -2.5746

ADF test for y

ADF statistic: -0.6210

p-value: 0.8662

Critical values:

1%: -3.4636

5%: -2.8762

10%: -2.5746

ADF test for residuals

ADF statistic: -0.5837

p-value: 0.8746

Critical values:

1%: -3.4636

5%: -2.8762

10%: -2.574617.9 Fixing the Problem: Differencing¶

A common solution is to difference the data.

Instead of estimating:

we estimate:

where:

and:

Regression in Differences¶

d_x = np.diff(x)

d_y = np.diff(y)

D_X = sm.add_constant(d_x)

diff_model = sm.OLS(d_y, D_X)

diff_results = diff_model.fit()

print(diff_results.summary()) OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.005

Model: OLS Adj. R-squared: -0.000

Method: Least Squares F-statistic: 0.9755

Date: Wed, 29 Apr 2026 Prob (F-statistic): 0.325

Time: 14:14:36 Log-Likelihood: -279.21

No. Observations: 199 AIC: 562.4

Df Residuals: 197 BIC: 569.0

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0405 0.070 -0.576 0.565 -0.179 0.098

x1 0.0719 0.073 0.988 0.325 -0.072 0.215

==============================================================================

Omnibus: 0.339 Durbin-Watson: 1.967

Prob(Omnibus): 0.844 Jarque-Bera (JB): 0.181

Skew: -0.067 Prob(JB): 0.914

Kurtosis: 3.063 Cond. No. 1.08

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.This is what we should expect, because the two random walks were generated from independent shocks.

17.10 Interpretation¶

Spurious regression arises because nonstationary series can move together over time even when there is no true relationship.

Differencing often solves the problem by removing the stochastic trend.

However, differencing is not always the final answer.

Sometimes nonstationary variables really do move together because of a long-run equilibrium relationship.

This leads to the idea of cointegration.

17.11 Connection to Cointegration¶

There is one important exception to the warning about regressions in levels.

In other words:

nonstationary residuals → spurious regression

stationary residuals → possible cointegration

We return to this idea in Chapter 20.

17.12 GRETL Example¶

We now reproduce the simulation and regression in GRETL.

Step 1: Create Data in GRETL¶

Menu¶

Set up for data entry:

File → New data setSelect:

Time series: T = 200Choose frequency:

Other

This creates an index variable.

Then generate two white-noise variables:

Add → Random variable → Normal distribution

Generate:

uv

Then create cumulative sums:

Add → Define new variable

Use:

x = cum(u)

y = cum(v)Command¶

nulldata 200

set seed 124

series u = normal()

series v = normal()

series x = cum(u)

series y = cum(v)Step 2: Plot the Series¶

Menu¶

Graph → Time series plot

Select:

xy

Command¶

gnuplot x y --time-series --with-lines

Figure 1:Two independent random walks

Step 3: Run the Spurious Regression¶

Menu¶

Model → Ordinary Least Squares

Dependent variable:

yIndependent variable:

x

Command¶

ols y const xExample output:

Model 1: OLS, using observations 1-200

Dependent variable: y

coefficient std. error t-ratio p-value

---------------------------------------------------------

const 0.578591 0.295706 1.957 0.0518 *

x 0.660102 0.0333565 19.79 8.40e-049 ***

Mean dependent var −4.061555 S.D. dependent var 4.385945

Sum squared resid 1285.510 S.E. of regression 2.548033

R-squared 0.664188 Adjusted R-squared 0.662492

F(1, 198) 391.6158 P-value(F) 8.40e-49

Log-likelihood −469.8470 Akaike criterion 943.6941

Schwarz criterion 950.2907 Hannan-Quinn 946.3636Step 4: Save and Plot Residuals¶

Menu¶

In the regression window:

Save → Residuals

Command¶

series uhat = $uhat

gnuplot uhat --time-series --with-lines

Figure 2:Residuals from the spurious regression

The residuals still show persistent behavior.

Step 5: Check Residual Autocorrelation¶

Menu¶

Variable → Correlogram

Select uhat.

If you do not see this option, go to:

Data → Dataset structure...

and select:

Time series → Other

You can also right click on uhat and select Correlogram.

Command¶

corrgm uhat

Figure 3:Correlogram of residuals

Step 6: ADF Tests¶

Menu¶

Variable → Unit root tests → Augmented Dickey-Fuller

Test:

xyuhat

Command¶

adf 0 x

adf 0 y

adf 0 uhatIt is often better to use the menu because GRETL can help determine an appropriate lag length for the ADF test.

Example output for x:

Augmented Dickey-Fuller test for x

testing down from 14 lags, criterion AIC

sample size 199

unit-root null hypothesis: a = 1

test with constant

including 0 lags of (1-L)x

model: (1-L)y = b0 + (a-1)*y(-1) + e

estimated value of (a - 1): -0.0224933

test statistic: tau_c(1) = -1.57309

asymptotic p-value 0.4964Example output for y:

Augmented Dickey-Fuller test for y

testing down from 14 lags, criterion AIC

sample size 199

unit-root null hypothesis: a = 1

test with constant

including 0 lags of (1-L)y

estimated value of (a - 1): -0.0198401

test statistic: tau_c(1) = -1.22352

asymptotic p-value 0.6666Example output for uhat:

Augmented Dickey-Fuller test for uhat

testing down from 14 lags, criterion AIC

sample size 195

unit-root null hypothesis: a = 1

test with constant

including 4 lags of (1-L)uhat

estimated value of (a - 1): -0.117113

test statistic: tau_c(1) = -2.93493

asymptotic p-value 0.04143Step 7: Difference the Data¶

Menu¶

Select x and y, right click, and choose:

Add differences

Command¶

series d_x = diff(x)

series d_y = diff(y)Step 8: Re-estimate the Regression in Differences¶

Menu¶

Model → Ordinary Least Squares

Dependent variable:

d_yIndependent variable:

d_x

Command¶

ols d_y const d_xExample output:

Model 2: OLS, using observations 2-200 (T = 199)

Dependent variable: d_y

coefficient std. error t-ratio p-value

-------------------------------------------------------

const −0.0721970 0.0706927 −1.021 0.3084

d_x −0.0574247 0.0647031 −0.8875 0.3759

Mean dependent var −0.068429 S.D. dependent var 0.994910

Sum squared resid 195.2089 S.E. of regression 0.995444

R-squared 0.003982 Adjusted R-squared -0.001073

F(1, 197) 0.787676 P-value(F) 0.375886

Log-likelihood −280.4549 Akaike criterion 564.9099

Schwarz criterion 571.4965 Hannan-Quinn 567.5757

rho 0.000807 Durbin-Watson 1.97873217.13 Practical Checklist¶

17.14 Common Mistakes¶

17.15 Looking Ahead¶

Spurious regression teaches us a central lesson:

In the next chapter, we introduce dynamic regression models, including distributed lag models and ARDL models.

These models allow us to study how variables affect each other over time.

Key Takeaways¶

Concept Check¶

Basic¶

What is spurious regression?

Why can two unrelated time series appear to be related?

What role does nonstationarity play in spurious regression?

Intuition¶

Why do random walks tend to drift over time?

How can two independent random walks appear to move together?

Why is a high not reliable evidence of a relationship in time series data?

Intermediate¶

What assumptions of classical regression are violated with nonstationary data?

Why are t-statistics and p-values unreliable in spurious regressions?

What is the key diagnostic principle involving residuals?

Diagnostics¶

What does it mean if regression residuals are nonstationary?

Why is residual autocorrelation a warning sign?

Fixing the Problem¶

Why does differencing often remove spurious relationships?

Challenge¶

Can a regression in levels ever be valid with nonstationary variables?

Explain.

Interpretation & Practice¶

A regression produces:

high

significant coefficient

strong trend in residuals

What does this suggest?

Two variables trend upward over time.

Regression shows strong relationship.

What is the key concern?

Residuals from a regression appear highly persistent.

What does this imply?

After differencing, the regression coefficient becomes insignificant.

What does this suggest about the original relationship?

ADF test fails to reject unit root for residuals.

What does this imply?

Suppose inflation and GDP both trend upward.

Regression suggests a strong relationship.

What must you check before concluding causality?

Challenge¶

A regression in levels produces stationary residuals.

What does this suggest?

What concept does this relate to?

Numerical Practice¶

Random Walk Construction¶

Suppose:

with shocks:

and .

Compute

Differencing¶

Using the values above:

Compute

Interpretation¶

Why is stationary but is not?

Regression Output¶

Suppose a regression produces:

coefficient significant

residuals highly autocorrelated

What is the likely problem?

ADF Interpretation¶

Suppose you estimate a regression between two time series and obtain the following ADF test results:

| Series | ADF p-value |

|---|---|

| 0.82 | |

| 0.76 | |

| residuals | 0.80 |

What do these results suggest about and ?

Are the residuals stationary?

Is the regression likely to be spurious?

Now consider an alternative case:

| Series | ADF p-value |

|---|---|

| 0.88 | |

| 0.91 | |

| residuals | 0.02 |

What do these results suggest about and ?

Are the residuals stationary?

What does this imply about the regression?

What concept does this relate to?

Why is it possible for and to be nonstationary, but the residuals to be stationary?

Model Comparison¶

Suppose:

Levels regression shows strong relationship

Differences regression shows no relationship

What conclusion should you draw?

Challenge¶

Suppose you regress two random walks and obtain:

significant coefficient

high

Why is this misleading?

What underlying property causes this?

Suppose residuals are stationary.

What does this imply?

What is the next step in analysis?

Appendix 17A — Why Nonstationarity Leads to Spurious Regression¶

This appendix provides an intuitive but slightly more formal explanation of why regressions involving nonstationary time series can produce misleading results.

A.1 Setup¶

Consider two independent random walks:

Assume:

and are independent

there is no true relationship between and

A.2 Accumulation of Shocks¶

A random walk can be written as:

so its variance is:

This is the defining feature of nonstationarity.

A.3 Persistent Trending Behavior¶

Because shocks accumulate:

both and tend to drift over time

they exhibit persistent trending behavior

Even though these trends are random, they can look systematic in finite samples.

A.4 The Regression Problem¶

Now consider the regression:

The OLS estimator is:

This expression is written in simplified mean-zero form. The same intuition applies when an intercept is included.

A.5 Why the Estimator Misbehaves¶

Even though and are independent:

both contain persistent trends

large values of may coincide with large values of

both and can grow because shocks accumulate

A.6 Failure of Standard Inference¶

Standard regression theory assumes:

constant variance

weak dependence

stable distributions over time

But with nonstationary data:

variance increases with time

shocks have long-lasting effects

observations are highly dependent

A.7 Residual Behavior¶

If the regression were meaningful, the residuals should be stationary.

However:

often inherits nonstationarity from and .

A.8 Big Picture¶

A.9 How to Fix the Problem¶

There are two main approaches:

difference the data, focusing on short-run relationships

test for cointegration, recovering possible long-run relationships