Chapter 22 — VAR Models

In earlier chapters, we studied models involving a single time series.

For example:

AR models explained persistence in one variable,

ARIMA models modeled trends and differencing,

forecasting models projected future values from past observations,

ECM models described long-run equilibrium adjustment.

These models are powerful when the focus is a single variable through time.

But many economic and financial systems involve several variables evolving together.

Examples include:

inflation and interest rates,

GDP growth and unemployment,

exchange rates and inflation,

stock returns and volatility,

oil prices and inflation.

Economic systems often involve:

feedback,

interaction,

and dynamic dependence across variables.

Vector autoregression (VAR) models were developed precisely for this purpose.

VAR models allow multiple variables, feedback channels, and dynamic interactions to be modeled jointly.

This chapter introduces:

multivariate dynamics,

vector autoregressions,

lag selection,

stability,

and VAR forecasting.

The emphasis remains intuition-first and applications-oriented.

Learning Objectives¶

By the end of this chapter, you should be able to:

explain the intuition behind VAR models

distinguish univariate and multivariate models

estimate VAR models

select lag lengths

interpret lagged interactions

perform basic VAR forecasting

interpret VAR results economically

22.1 Why Multivariate Models?¶

Economic variables rarely move independently.

For example:

inflation influences interest rates,

interest rates influence investment,

investment influences GDP,

GDP influences unemployment.

A univariate AR model ignores these interactions.

VAR models attempt to capture them directly.

22.2 From AR Models to VAR Models¶

Recall the AR(1) model:

The current value depends on:

its own past,

plus a shock.

Extending to Multiple Variables¶

Suppose we have two variables:

inflation,

interest rate.

A VAR allows each variable to depend on:

its own lags,

and lags of the other variable.

22.3 A Simple VAR(1)¶

A two-variable VAR(1) may be written:

where:

= inflation,

= interest rate.

22.4 Why VAR Models Became Popular¶

VAR models became highly influential in macroeconomics and finance because they provide a flexible framework for studying dynamic interactions across variables.

Christopher Sims argued that many macroeconomic systems should be modeled jointly rather than through isolated single equations.

This contrasts with traditional regression models where some variables are treated as purely explanatory.

22.5 Endogenous and Exogenous Variables¶

In many regression models:

some variables are explanatory,

others are dependent.

VAR models are different.

This means:

inflation may affect interest rates,

but interest rates may also affect inflation.

The relationship is dynamic and simultaneous through time.

22.6 Reduced Form VARs¶

The most common VAR specification is the reduced form VAR.

A reduced form VAR expresses each variable as a function of lagged values of all variables in the system.

Example¶

Suppose we model:

inflation,

unemployment,

interest rate.

Then each equation includes:

lags of inflation,

lags of unemployment,

lags of interest rates.

22.7 VAR(p) Models¶

A VAR with multiple lags is written as VAR().

For example:

VAR(1),

VAR(2),

VAR(4).

General Form¶

where:

is a vector of variables,

are coefficient matrices,

is a vector of shocks.

As the number of variables and lags increases, estimation becomes more complex.

22.8 Stationarity in VAR Models¶

Stationarity remains important in multivariate time series models.

Standard VAR models are typically estimated using stationary variables.

If variables are nonstationary:

spurious relationships may emerge,

statistical inference becomes unreliable,

and forecasts may become unstable.

Common Approaches¶

If variables are nonstationary:

difference the data,

or use cointegration and VECM methods.

We studied unit roots and cointegration earlier in the book.

Differencing may remove important long-run information when variables are cointegrated.

22.9 Example: Inflation and Interest Rates¶

Suppose inflation rises persistently.

Central banks may respond by:

increasing interest rates.

But higher interest rates may later reduce:

inflation,

investment,

economic activity.

VAR models attempt to capture these dynamic feedback effects.

22.10 Estimating a VAR in Python¶

We now estimate a simple VAR using financial data.

The system contains two variables:

SPY daily log returns,

a rolling 20-day volatility proxy.

This example is useful because returns and volatility often interact dynamically.

For example:

large negative returns may be followed by higher volatility,

high-volatility periods may affect subsequent returns,

and both variables may display persistence through time.

import yfinance as yf

import pandas as pd

import numpy as np

from statsmodels.tsa.api import VAR

# Download SPY data

spy = yf.download(

"SPY",

start="2015-01-01",

auto_adjust=False

)

# Extract adjusted close prices

prices = spy["Adj Close"]

# Compute daily log returns in percent

returns = 100 * np.log(

prices / prices.shift(1)

)

# Rolling 20-day volatility proxy

volatility = returns.rolling(20).std()

# Combine variables

data = pd.concat(

[returns, volatility],

axis=1

)

data.columns = [

"Returns",

"Volatility"

]

data = data.dropna()

# Estimate VAR(2)

model = VAR(data)

results = model.fit(2)

print(results.summary()) Summary of Regression Results

==================================

Model: VAR

Method: OLS

Date: Thu, 07, May, 2026

Time: 16:08:54

--------------------------------------------------------------------

No. of Equations: 2.00000 BIC: -4.95229

Nobs: 2830.00 HQIC: -4.96572

Log likelihood: -983.966 FPE: 0.00692024

AIC: -4.97330 Det(Omega_mle): 0.00689585

--------------------------------------------------------------------

Results for equation Returns

================================================================================

coefficient std. error t-stat prob

--------------------------------------------------------------------------------

const 0.003909 0.037664 0.104 0.917

L1.Returns -0.116688 0.018935 -6.162 0.000

L1.Volatility -0.517839 0.271001 -1.911 0.056

L2.Returns 0.051612 0.018954 2.723 0.006

L2.Volatility 0.572478 0.271108 2.112 0.035

================================================================================

Results for equation Volatility

================================================================================

coefficient std. error t-stat prob

--------------------------------------------------------------------------------

const 0.009302 0.002573 3.615 0.000

L1.Returns -0.008181 0.001294 -6.324 0.000

L1.Volatility 1.176947 0.018513 63.574 0.000

L2.Returns -0.006876 0.001295 -5.310 0.000

L2.Volatility -0.186193 0.018520 -10.053 0.000

================================================================================

Correlation matrix of residuals

Returns Volatility

Returns 1.000000 -0.122110

Volatility -0.122110 1.00000022.11 Reading VAR Output¶

A VAR output table may initially appear overwhelming.

Remember:

each equation has its own dynamics,

each variable depends on lagged values of all variables,

and feedback effects accumulate through time.

Rather than focusing immediately on individual coefficients, it is often more useful to ask broader questions:

Which variables appear persistent?

Which cross-variable effects appear strongest?

Do relationships appear economically plausible?

Do shocks appear temporary or long-lasting?

This is one reason impulse response analysis becomes especially important in multivariate time series models.

22.12 Choosing Lag Lengths¶

One important decision is:

How many lags should be included?Too few lags:

omit important dynamics.

Too many lags:

waste degrees of freedom,

increase estimation noise.

Information Criteria¶

VAR lag lengths are often selected using:

AIC,

BIC,

HQIC.

Intuition¶

These criteria balance:

model fit,

and model complexity.

22.13 Lag Selection in Python¶

lag_selection = model.select_order(10)

print(lag_selection.summary()) VAR Order Selection (* highlights the minimums)

==================================================

AIC BIC FPE HQIC

--------------------------------------------------

0 -0.7217 -0.7174 0.4859 -0.7201

1 -4.917 -4.904 0.007321 -4.912

2 -4.967 -4.946 0.006962 -4.960

3 -4.991 -4.962 0.006797 -4.981

4 -5.028 -4.990 0.006550 -5.015

5 -5.046 -4.999 0.006436 -5.029

6 -5.060 -5.006 0.006343 -5.041

7 -5.071 -5.007 0.006278 -5.048

8 -5.078 -5.006 0.006232 -5.052

9 -5.089 -5.009* 0.006166 -5.060*

10 -5.090* -5.002 0.006155* -5.058

--------------------------------------------------In practice:

economic intuition,

diagnostics,

and forecasting performance

also matter.

22.14 Stability of VAR Models¶

A stable VAR system eventually absorbs shocks.

After temporary disturbances:

variables gradually return toward typical behavior,

dynamic effects decay,

and forecasts remain bounded.

An unstable system may instead produce explosive dynamics.

Intuition¶

Suppose a shock temporarily increases inflation.

In a stable system:

inflation eventually settles,

interest rates stabilize,

and the system returns toward normal dynamics.

In an unstable system:

responses may grow larger over time,

feedback effects may amplify,

and forecasts may explode unrealistically.

Stability and Dynamic Systems¶

VAR models are dynamic systems.

Small changes today may influence future periods through recursive feedback.

A stable system prevents these effects from growing indefinitely.

This idea becomes especially important when studying:

impulse responses,

dynamic forecasting,

and long-horizon simulations.

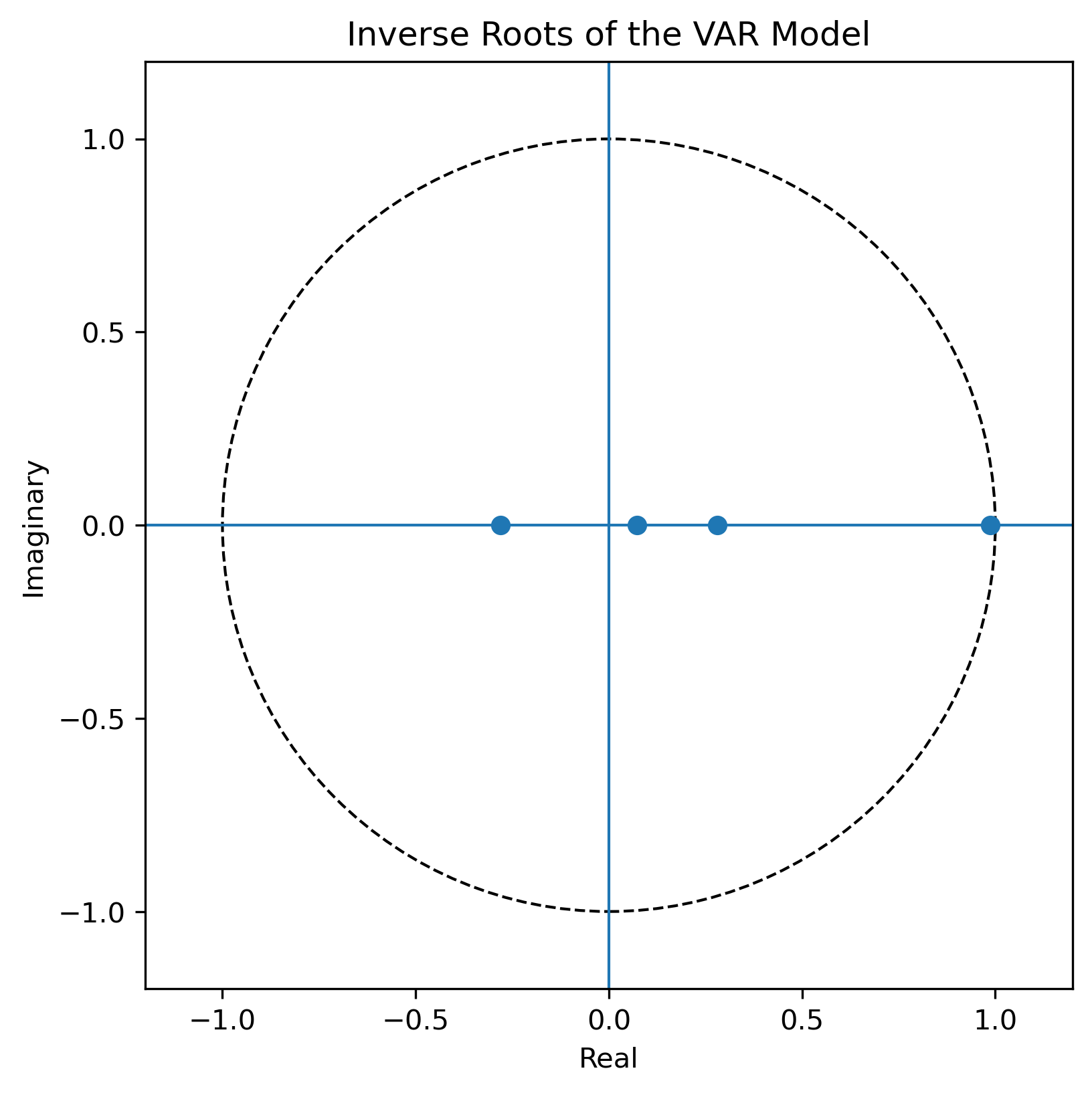

22.15 Inverse Roots and Stability¶

One common way to assess VAR stability is through inverse roots plots.

A stable VAR requires all inverse roots to lie inside the unit circle.

Intuition¶

The unit circle acts like a stability boundary.

Inside the circle → stable dynamics Outside the circle → unstable or explosive dynamics

Add this inverse-roots code¶

import matplotlib.pyplot as plt

import numpy as np

# Statsmodels reports roots of the VAR characteristic polynomial.

# Stability requires these roots to lie outside the unit circle.

# Inverse roots should therefore lie inside the unit circle.

inverse_roots = 1 / results.roots

fig, ax = plt.subplots(figsize=(6,6))

circle = plt.Circle(

(0, 0),

1,

fill=False,

linestyle="--"

)

ax.add_artist(circle)

ax.scatter(

inverse_roots.real,

inverse_roots.imag

)

ax.axhline(0, linewidth=1)

ax.axvline(0, linewidth=1)

ax.set_xlim(-1.2, 1.2)

ax.set_ylim(-1.2, 1.2)

ax.set_aspect("equal")

ax.set_title("Inverse Roots of the VAR Model")

ax.set_xlabel("Real")

ax.set_ylabel("Imaginary")

plt.savefig("figs/ch22/inverse_roots.png", dpi=300, bbox_inches="tight")

plt.close()

22.16 Forecasting with VAR Models¶

VAR models are widely used for forecasting because they incorporate:

multiple variables,

dynamic interactions,

and recursive feedback effects.

Unlike univariate models, VAR forecasts allow information from several variables to influence future predictions jointly.

22.17 Dynamic Forecasting in VAR Models¶

VAR forecasts are recursive.

Forecasts for future periods depend partly on previous forecasts.

For example:

depends partly on:

This recursive structure allows VAR models to capture rich dynamic interactions across variables.

Intuition¶

Suppose stock-market volatility rises unexpectedly.

The VAR may predict:

lower future returns,

which then influence future volatility,

which then feed back into later forecasts.

This creates dynamic forecast paths rather than isolated predictions.

22.18 VAR Forecasting in Python¶

VAR models are widely used for forecasting.

Because they incorporate:

multiple variables,

interactions,

and dynamic feedback,

they often outperform simple univariate models.

Example: VAR Forecasting¶

forecast = results.forecast(

data.values[-2:],

steps=10

)

forecast_df = pd.DataFrame(

forecast,

columns=data.columns

)

print(forecast_df) Returns Volatility

0 -0.007599 0.600904

1 0.130212 0.588281

2 0.027692 0.588780

3 0.039283 0.591609

4 0.031460 0.595456

5 0.032598 0.599441

6 0.032200 0.603460

7 0.032506 0.607443

8 0.032688 0.611383

9 0.032922 0.61527522.19 Beyond Coefficients: Dynamic Responses¶

VAR coefficient tables alone are often difficult to interpret economically.

Because variables interact dynamically through time, economists frequently analyze systems using:

impulse response functions (IRFs),

and forecast error variance decomposition (FEVD).

These tools help trace:

how shocks propagate,

how long effects persist,

and which shocks matter most.

The next chapter develops these ideas in detail.

22.20 Common Applications of VAR Models¶

VARs are widely used in:

macroeconomics,

monetary policy,

finance,

exchange-rate analysis,

business-cycle analysis.

Financial Applications¶

Examples include:

stock returns and volatility,

exchange rates and interest rates,

oil prices and inflation.

22.21 Gretl Example: Estimating a VAR¶

Gretl provides built-in tools for VAR estimation.

Step 1¶

Load multiple time series.

Example:

inflation,

interest rate,

GDP growth.

Step 2¶

Menu:

Model → Time Series → VARStep 3¶

Choose:

variables,

lag length,

deterministic terms.

[GRETL Screenshot Placeholder: VAR specification window]Gretl Diagnostics¶

After estimation, GRETL provides:

residual diagnostics,

stability tests,

impulse responses,

variance decomposition.

[GRETL Screenshot Placeholder: VAR output]22.23 Common Mistakes¶

22.24 Looking Ahead¶

VAR models provide a flexible framework for studying interacting time series systems.

But coefficient tables alone rarely provide the clearest economic interpretation.

The next chapter introduces impulse response functions (IRFs), which trace how shocks propagate dynamically through multivariate systems.

We will move from:

Key Takeaways¶

Concept Check¶

Basic¶

What is a VAR model?

How does a VAR differ from a univariate AR model?

What does it mean for all variables in a VAR to be endogenous?

Intuition¶

Why are multivariate models important in economics?

What type of interactions can VAR models capture?

Why is it unrealistic to model macroeconomic variables in isolation?

Structure¶

In a VAR(1), what variables appear on the right-hand side?

What does VAR() mean?

Why does the number of parameters increase quickly in VAR models?

Stationarity¶

Why is stationarity important in VAR models?

What are the consequences of estimating a VAR with nonstationary data?

Challenge¶

Why are VAR coefficients often difficult to interpret directly?

Interpretation & Practice¶

A VAR model shows that:

inflation depends on past interest rates

interest rates depend on past inflation

What type of relationship does this suggest?

A VAR is estimated with too few lags.

What might happen?

A VAR is estimated with too many lags.

What problem might arise?

A model includes multiple variables with strong feedback.

Why might a VAR be appropriate?

Lag Selection¶

AIC suggests 5 lags, BIC suggests 2 lags.

Why might these differ?

Which might you prefer?

Stationarity¶

Variables appear to be nonstationary.

What should you do before estimating a VAR?

Numerical Practice¶

VAR Interpretation¶

Consider a VAR(1):

Does depend on past ?

Does depend on past ?

Lag Structure¶

Suppose you increase lag length from 1 to 4.

What happens to:

number of parameters?

estimation complexity?

Information Criteria¶

Suppose:

| Lag | AIC | BIC |

|---|---|---|

| 1 | -4.5 | -4.4 |

| 2 | -4.8 | -4.6 |

| 3 | -4.9 | -4.5 |

Which lag is chosen by AIC?

Which by BIC?

Interpretation¶

Suppose a variable responds strongly to its own lag.

What does this suggest?

Diagnostics¶

Residuals show autocorrelation.

What does this imply?

What should be done?

Challenge¶

Suppose a VAR includes 5 variables and 4 lags.

Why might this be problematic?

Interpretation¶

A coefficient on lagged inflation is positive and significant.

What does this imply?

Why might interpretation still be limited?

Challenge¶

Why should VAR results be interpreted using IRFs rather than raw coefficients?

Forecasting with VAR

Why might VAR models outperform univariate models?

What makes VAR forecasts dynamic?

Interpretation¶

Forecasts depend on previous forecasts.

Why?

Why might VAR forecasts still perform poorly in practice?

Appendix 22A — Why VARs Became Influential¶

VARs became highly influential because they offered a systematic way to model rich dynamics across multiple time series.

Earlier macroeconomic models often relied heavily on strong theoretical restrictions.

VARs instead emphasized:

empirical dynamics,

flexible interactions,

and forecasting performance.

This made them especially attractive for applied macroeconomics and finance.

Appendix 22B — Dynamic Forecasting¶

VAR forecasts are dynamic because future values depend recursively on previous forecasts.

For example:

depends partly on:

This recursive structure is one reason VAR forecasting can capture complex dynamic interactions across variables.