Chapter 13 — ARMA Models

In the previous chapters, we studied:

autoregressive (AR) models

moving average (MA) models

Each captures a different type of dependence:

AR models depend on past values

MA models depend on past shocks

In practice, many time series exhibit both types simultaneously.

This motivates the ARMA model.

Learning Objectives¶

By the end of this chapter, you should be able to:

understand the motivation behind ARMA models

define ARMA() processes

interpret AR and MA components jointly

understand stationarity and invertibility

interpret ACF and PACF behavior

estimate ARMA models

perform diagnostics

13.1 Why Combine AR and MA?¶

AR models:

capture persistence

MA models:

capture temporary shock propagation

But real-world data often show both.

13.2 The ARMA(1,1) Model¶

Interpretation¶

The present depends on:

past values (persistence)

current shocks

past shocks

13.3 Simulation¶

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(123)

n = 400

phi = 0.7

theta = 0.5

w = np.random.normal(size=n)

x = np.zeros(n)

for t in range(1,n):

x[t] = phi*x[t-1] + w[t] + theta*w[t-1]

plt.figure(figsize=(10,4))

plt.plot(x, lw=1)

plt.title(r"ARMA(1,1): $\phi=0.7,\ \theta=0.5$")

plt.savefig("figs/ch13/arma11.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

13.4 Mean¶

Without a constant:

13.5 Stationarity and Invertibility¶

ARMA requires:

Stationarity (AR part)¶

Invertibility (MA part)¶

13.6 Backshift Form¶

13.7 Infinite MA Representation¶

13.8 Infinite AR Representation¶

13.9 ACF and PACF Behavior¶

Why?¶

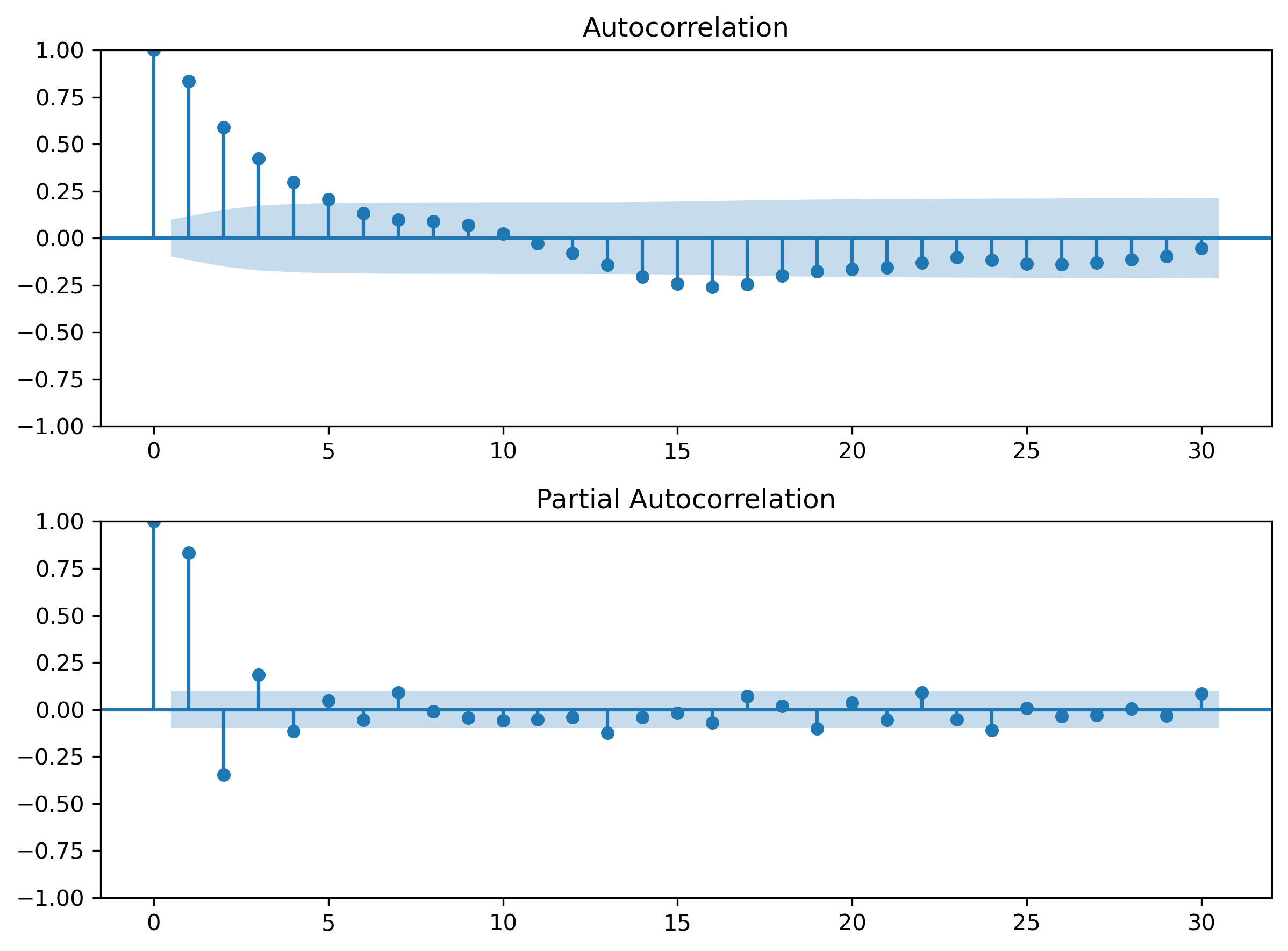

13.10 Simulated ACF/PACF¶

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

fig, ax = plt.subplots(2,1, figsize=(8,6))

plot_acf(x, lags=30, ax=ax[0])

plot_pacf(x, lags=30, method='ywm', ax=ax[1])

plt.tight_layout()

plt.savefig("figs/ch13/arma11_acf_pacf.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

13.11 AR vs MA vs ARMA¶

| Model | ACF | PACF |

|---|---|---|

| AR | tails off | cuts off |

| MA | cuts off | tails off |

| ARMA | tails off | tails off |

13.12 Identification in Practice¶

Steps:

visualize data

ensure stationarity

inspect ACF/PACF

estimate candidates

check diagnostics

compare models

13.13 Estimation¶

import statsmodels.api as sm

model = sm.tsa.ARIMA(x, order=(1,0,1))

res = model.fit()

print(res.summary()) SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 400

Model: ARIMA(1, 0, 1) Log Likelihood -564.412

Date: Mon, 04 May 2026 AIC 1136.824

Time: 22:05:59 BIC 1152.790

Sample: 0 HQIC 1143.147

- 400

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.2646 0.248 -1.068 0.286 -0.750 0.221

ar.L1 0.6901 0.044 15.840 0.000 0.605 0.775

ma.L1 0.5423 0.049 11.081 0.000 0.446 0.638

sigma2 0.9803 0.069 14.148 0.000 0.845 1.116

===================================================================================

Ljung-Box (L1) (Q): 0.07 Jarque-Bera (JB): 0.11

Prob(Q): 0.80 Prob(JB): 0.95

Heteroskedasticity (H): 0.70 Skew: 0.04

Prob(H) (two-sided): 0.04 Kurtosis: 3.01

===================================================================================13.14 Diagnostics¶

from statsmodels.stats.diagnostic import acorr_ljungbox

acorr_ljungbox(res.resid, lags=[10,20], return_df=True)| | lb_stat | lb_pvalue |

|---------|------------|-----------|

| 10 | 4.229114 | 0.936420 |

| 20 | 25.470103 | 0.184034 |

13.15 Information Criteria¶

13.16 Applications¶

ARMA models are used for:

inflation

GDP growth

exchange rates

interest rates

demand forecasting

13.17 Common Mistakes¶

13.18 Looking Ahead¶

Next:

Key Takeaways¶

Concept Check¶

Basic¶

What is an ARMA model?

What are the two components of an ARMA model?

What does the AR component capture?

What does the MA component capture?

Intuition¶

Why do many real-world time series require both AR and MA components?

How does an ARMA model differ from a pure AR or pure MA model?

What happens when both persistence and short-term shocks influence a series?

Intermediate¶

What are the stationarity and invertibility conditions for an ARMA(1,1) model?

Why must both conditions hold?

What is the backshift representation of an ARMA model?

ACF & PACF¶

What pattern does the ACF of an ARMA model exhibit?

What pattern does the PACF of an ARMA model exhibit?

Why do ARMA models not show sharp cutoffs in ACF or PACF?

Interpretation¶

Why is model identification more difficult for ARMA models than for AR or MA models?

Why should ACF and PACF be used cautiously in ARMA identification?

Challenge¶

Suppose a time series exhibits both:

strong persistence

short-lived shock effects

Why is ARMA a natural model?

Interpretation & Practice¶

A time series shows:

gradual decay in ACF

gradual decay in PACF

What type of model might this suggest?

Why?

ACF and PACF do not show clear cutoff patterns.

Why might this happen?

What modeling approach would you take?

A series appears smoother than pure AR but still persistent.

What might this indicate?

A model captures persistence but leaves short-term fluctuations unexplained.

What component might be missing?

A model captures shocks well but fails to capture persistence.

What component might be missing?

Finance Interpretation¶

A financial time series shows:

short-term reaction to news

longer-term persistence

Why might ARMA be appropriate?

A return series appears unpredictable but slightly autocorrelated.

What type of structure might exist?

Diagnostics¶

After estimating an ARMA model, residuals still show autocorrelation.

What does this imply?

What should you do next?

Challenge¶

Two ARMA models fit equally well visually.

How would you choose between them?

Numerical Practice¶

ARMA Construction¶

Consider:

with:

Compute

Comparing Models¶

Compare:

AR(1):

MA(1):

Which shows longer persistence?

Which shows finite shock effects?

ACF Interpretation¶

Suppose you observe:

ACF decays gradually

PACF also decays gradually

What model class is suggested?

Identification¶

You observe:

ACF does not cut off

PACF does not cut off

Why is ARMA a candidate model?

Estimation Output¶

Suppose:

Is the series persistent?

Are shocks temporary or long-lasting?

What does this imply about dynamics?

Diagnostics¶

Suppose residuals show:

significant autocorrelation

What does this imply?

What should be done?

Model Selection¶

Suppose two models produce:

Model A: lower AIC

Model B: lower BIC

What does this suggest?

How would you decide?

Challenge¶

Suppose an ARMA model fits the data well but performs poorly in forecasting.

What might be the issue?

Why is validation important?

Suppose is close to 1 and is large.

What type of behavior would you expect?

Why might this resemble a near-nonstationary process?

A time series shows:

moderate persistence

small but noticeable short-term fluctuations

no clear ACF cutoff

What model would you try first? Why?

Appendix 13A — Additional Insight¶

A.1 Why ACF Tails Off¶

AR component generates:

gradual decay in correlations

MA component adds:

short-term structure

Combined → no cutoff

A.2 Infinite Representations¶

ARMA can be expressed as:

infinite MA (if stationary)

infinite AR (if invertible)