Chapter 18 — Dynamic Regression and ARDL Models

In the previous chapter, we saw that regressions involving nonstationary variables can produce spurious results.

One common response was to difference the data:

At first glance, this may look like a technical fix. But it is more than that.

This chapter introduces dynamic regression models more generally. These models allow us to study how relationships unfold over time.

Learning Objectives¶

By the end of this chapter, you should be able to:

explain what a dynamic regression model is

distinguish static and dynamic models

understand distributed lag models

understand autoregressive distributed lag (ARDL) models

interpret short-run and long-run effects

diagnose residual autocorrelation

explain why differencing may remove long-run information

understand how dynamic models lead naturally to cointegration and ECM

18.1 From Spurious Regression to Dynamics¶

Recall the differenced regression:

This model no longer explains the level of using the level of . Instead, it explains how changes in one variable are related to changes in another.

For example:

how changes in income affect changes in consumption

how changes in interest rates affect changes in investment

how changes in exchange rates affect changes in exports

This is already a dynamic way of thinking.

18.2 What Is a Dynamic Model?¶

A dynamic model allows current outcomes to depend on time-related information, such as:

past values of the dependent variable

past values of explanatory variables

current and past changes

past shocks

Static vs Dynamic Models¶

A static model is:

This says that responds immediately to .

A dynamic model might be:

Here, depends not only on , but also on its own past value.

18.3 Why Dynamics Matter¶

Many economic relationships do not adjust instantly.

For example:

consumption may respond gradually to income

investment may respond slowly to interest rates

prices may adjust with delays

money demand may depend on past money balances

This makes them especially useful in economics, finance, and business forecasting.

18.4 Distributed Lag Models¶

A natural way to introduce dynamics is to include current and past values of an explanatory variable.

A simple distributed lag model is:

Here:

measures the immediate effect of

measures the effect of last period’s

measures the effect from two periods ago

Short-Run and Cumulative Effects¶

In the distributed lag model:

the short-run effect is:

The cumulative effect over three periods is:

18.5 Autoregressive Distributed Lag Models¶

We now combine two ideas:

lagged dependent variables

lagged explanatory variables

This gives the autoregressive distributed lag model, or ARDL.

where:

is the number of lags of

is the number of lags of

captures persistence in

captures current and lagged effects of

18.6 Interpreting an ARDL Model¶

Consider a simple ARDL(1,1):

The coefficients have different roles:

→ immediate effect

→ delayed effect

→ persistence in

18.7 Short-Run and Long-Run Effects¶

Dynamic models distinguish between:

short-run responses

long-run cumulative effects

For the ARDL(1,1):

the immediate short-run effect is:

If the system is stable, the long-run multiplier is:

More generally:

18.8 Dynamic Interpretation¶

Consider an increase in interest rates.

Its effect on output may not be immediate:

firms may delay investment decisions

households may adjust spending gradually

banks may adjust lending conditions over time

A dynamic model allows this adjustment path to be represented explicitly.

18.9 Differencing as a Restricted Dynamic Model¶

Recall from Chapter 17:

This can be viewed as a restricted dynamic model:

no lagged levels

no persistence term

no long-run structure

This is useful for avoiding spurious regression, but it may discard economically meaningful long-run information.

18.10 Why Differencing Is Not Enough¶

While differencing often solves the spurious regression problem, it comes at a cost.

Differencing may remove:

long-run relationships

equilibrium behavior

information about levels

gradual adjustment mechanisms

This motivates cointegration and the error correction model.

18.11 Looking Ahead: ECM¶

Dynamic models (ARDL) attempt to bridge this gap by modeling:

short-run changes

long-run relationships

in a unified framework.

If two variables share a long-run equilibrium relationship, we may want to model both:

short-run changes

adjustment back toward the long-run relationship

This leads to the Error Correction Model (ECM):

We return to this idea in later chapters.

18.12 Gretl Example: ARDL Model¶

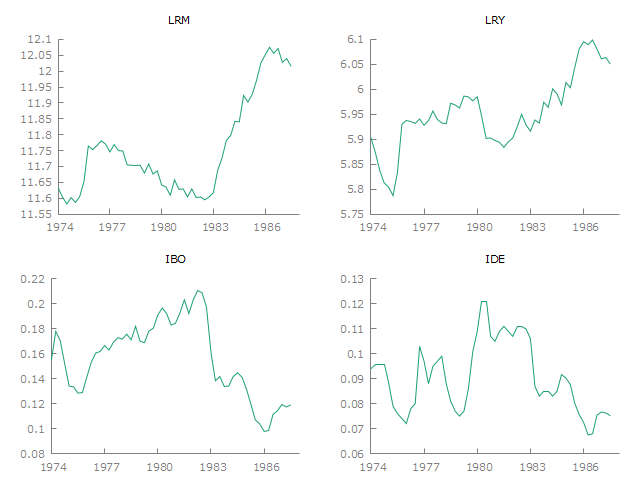

We now estimate a simple ARDL model using the denmark dataset in GRETL.

Step 1: Load the Data¶

Menu¶

File → Open data → Sample file...

Select the denmark data from the GRETL database.

The variables include:

LRM log of real money supply, M2

LRY log of real income

IBO bond rate

IDE bank deposit rate

Figure 1:Denmark macroeconomic data

Step 2: Estimate ARDL(1,1)¶

We estimate:

Menu¶

Model → Ordinary Least Squares

Dependent variable:

LRMRegressors:

LRM(-1) LRY LRY(-1)

To create lags, click the lags... icon in the model specification window.

Command¶

ols LRM const LRM(-1) LRY LRY(-1)Example output:

Model 1: OLS, using observations 1974:2-1987:3 (T = 54)

Dependent variable: LRM

coefficient std. error t-ratio p-value

---------------------------------------------------------

const 0.125046 0.342856 0.3647 0.7169

LRM_1 1.00090 0.0580381 17.25 1.09e-022 ***

LRY 0.630431 0.173817 3.627 0.0007 ***

LRY_1 −0.652328 0.170176 −3.833 0.0004 ***

Mean dependent var 11.75666 S.D. dependent var 0.152858

Sum squared resid 0.044114 S.E. of regression 0.029703

R-squared 0.964377 Adjusted R-squared 0.962240

F(3, 50) 451.2022 P-value(F) 3.49e-36

Log-likelihood 115.3464 Akaike criterion −222.6929

Schwarz criterion −214.7370 Hannan-Quinn −219.6246

rho −0.186568 Durbin's h −1.515760This can be written as:

18.13 Diagnosing ARDL Models¶

After estimating an ARDL model, we need to check whether the model has captured the relevant dynamics.

If residuals still contain autocorrelation, the model is missing some dynamic structure.

What Do We Mean by White Noise Residuals?¶

Residuals should show:

mean near zero

roughly constant variance

no autocorrelation

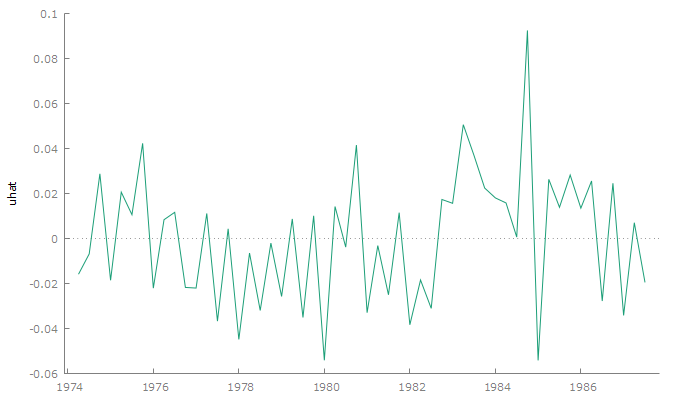

Step 1: Plot Residuals¶

Menu¶

Graph → Time series plot

Select residuals, such as uhat.

You can also right click on the residual variable and select Time series plot.

Command¶

gnuplot uhat --time-series

Figure 2:Residual plot

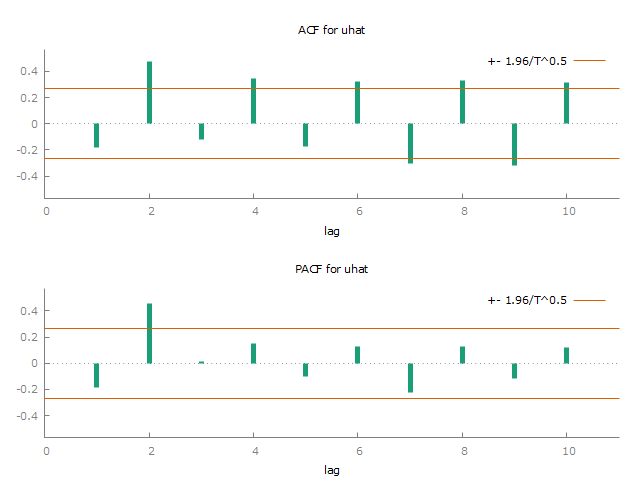

Step 2: Residual Correlogram¶

Menu¶

Select uhat.

Variable → Correlogram

You can also right click on uhat and select Correlogram.

Command¶

corrgm uhat

Figure 3:Correlogram of residuals

Step 3: Formal Test for Serial Correlation¶

In the model window:

Tests → Autocorrelation

GRETL reports tests such as the Breusch–Godfrey test and Ljung–Box Q test.

Example output:

Breusch-Godfrey test for autocorrelation up to order 4

OLS, using observations 1974:2-1987:3 (T = 54)

Dependent variable: uhat

coefficient std. error t-ratio p-value

--------------------------------------------------------

const 0.342059 0.336486 1.017 0.3147

LRY −0.00513435 0.162471 −0.03160 0.9749

LRY_1 0.0773596 0.173429 0.4461 0.6576

LRM_1 −0.0657127 0.0631492 −1.041 0.3035

uhat_1 −0.0607536 0.158039 −0.3844 0.7024

uhat_2 0.427085 0.147320 2.899 0.0057 ***

uhat_3 0.110868 0.162276 0.6832 0.4979

uhat_4 0.240594 0.160901 1.495 0.1417

Unadjusted R-squared = 0.283633

Test statistic: LMF = 4.553230,

with p-value = P(F(4,46) > 4.55323) = 0.0035

Alternative statistic: TR^2 = 15.316197,

with p-value = P(Chi-square(4) > 15.3162) = 0.00409

Ljung-Box Q' = 23.0858,

with p-value = P(Chi-square(4) > 23.0858) = 0.000122What If Residuals Are Not White Noise?¶

If residuals show autocorrelation, possible responses include:

add more lags of

add more lags of

reconsider the model specification

check whether variables are nonstationary

consider cointegration or ECM if levels matter

Important Distinction¶

18.14 Practical Checklist¶

18.15 Common Mistakes¶

18.16 Looking Ahead¶

Dynamic models help us understand how variables adjust over time.

But they do not fully resolve the issue of nonstationarity.

Is it possible to retain long-run information while avoiding spurious regression?

Yes — if a particular combination of nonstationary variables is stationary.

This concept is called cointegration, which we study later.

Key Takeaways¶

Concept Check¶

Basic¶

What is a dynamic regression model?

What is the difference between a static and a dynamic model?

What is a distributed lag model?

Intuition¶

Why do many economic relationships adjust gradually rather than instantly?

What does it mean for effects to “unfold over time”?

Why is including lagged variables important?

ARDL Models¶

What are the two key components of an ARDL model?

What does the lagged dependent variable capture?

What do lagged explanatory variables capture?

Short-Run vs Long-Run¶

What is the short-run effect in a distributed lag model?

What is the long-run multiplier?

Why are these two effects different?

Diagnostics¶

What should residuals look like in a well-specified dynamic model?

Why is residual autocorrelation a problem?

Challenge¶

Why is differencing alone not sufficient for economic modeling?

Interpretation & Practice¶

A static model shows poor fit, but a dynamic model fits well.

What does this suggest?

A model includes lagged dependent variables.

What type of behavior is being captured?

Residuals show strong autocorrelation.

What does this imply?

What should you do?

A model shows strong short-run effects but weak long-run effects.

What might this indicate?

A model shows large long-run multiplier.

What does this imply about persistence?

Trade-Off Interpretation¶

Differencing removes long-run relationships.

Why is this a problem?

A levels regression shows strong relationship but residuals are nonstationary.

What does this imply?

Challenge¶

Why might ARDL be preferred over simple differencing?

Numerical Practice¶

Distributed Lag¶

Suppose:

What is the immediate effect?

What is the cumulative effect?

ARDL(1,1)¶

Suppose:

What is the short-run effect?

Compute the long-run multiplier.

Interpretation¶

If , what does this imply about adjustment speed?

Diagnostics¶

Residual correlogram shows significant spikes.

What does this imply?

Model Improvement¶

What are two ways to improve a poorly specified ARDL model?

Challenge¶

Suppose:

levels regression → spurious

differenced regression → no relationship

What should you try next?

Appendix 18A — Dynamic Models and Long-Run Effects¶

This appendix shows how long-run effects arise from a simple ARDL model.

A.1 A Simple ARDL(1,1)¶

Consider:

A.2 Steady-State Long-Run Equilibrium¶

In the long run, suppose:

Substitute these into the ARDL(1,1) model:

So:

Rearranging:

Therefore:

A.3 Stability Condition¶

For the long-run expression to be meaningful, the process must be dynamically stable.

For ARDL(1,1), this requires:

A.4 Dynamic Adjustment¶

Start again from:

Subtract from both sides:

Since:

we can write:

This expression begins to reveal the link between ARDL and ECM.

A.5 Link to ECM¶

An ECM has the form:

The ECM representation makes this separation explicit.

Appendix 18B — ARDL Bounds Test for Cointegration¶

The ARDL framework can also be used to test for long-run relationships between variables.

This approach is known as the ARDL bounds testing procedure (Pesaran et al.).

B.1 Motivation¶

Recall the key problem:

Levels regression → may be spurious

Differenced regression → loses long-run information

B.2 From ARDL to Error Correction Form¶

Consider an ARDL(1,1):

This can be rewritten as:

where:

B.3 The Bounds Test¶

We test:

No long-run relationshipagainst:

At least one is non-zero → long-run relationship existsB.4 Decision Rule¶

The test uses an F-statistic.

Compare it with two bounds:

Lower bound → assumes variables are stationary

Upper bound → assumes variables are nonstationary

B.5 Why This Is Useful¶

B.6 Intuition¶

B.7 Link to ECM¶

If cointegration is confirmed, we can write:

B.8 Important Caution¶

B.9 Looking Ahead¶

We will study cointegration formally in Chapter 20.