Part I Capstone — Working with Financial Data

In Part I, we introduced:

time series data,

financial returns,

probability and uncertainty,

and the statistical foundations needed for later chapters.

This capstone integrates these ideas through a small applied project using real financial data.

The exercises below combine:

data collection,

visualization,

return calculations,

probability concepts,

and interpretation.

The goal is not only to compute statistics, but also to think economically about what the data represent.

Learning Goals¶

By completing this capstone, you should be able to:

download and organize financial data

compute simple and log returns

visualize prices and returns

interpret volatility

understand stylized facts of financial data

connect statistical concepts with financial interpretation

Background: Financial Time Series¶

Financial markets generate enormous quantities of time series data.

Examples include:

stock prices,

exchange rates,

interest rates,

commodity prices,

cryptocurrency prices.

Raw price data alone are often difficult to interpret statistically.

For this reason, analysts usually transform prices into:

Returns provide a more meaningful measure of financial performance and risk.

Dataset¶

We will use:

SET Indexthe ETF tracking the Thai SET index.

You may later replace this with:

S&P 500 index,

Korean KOSPI,

exchange rates,

or other assets.

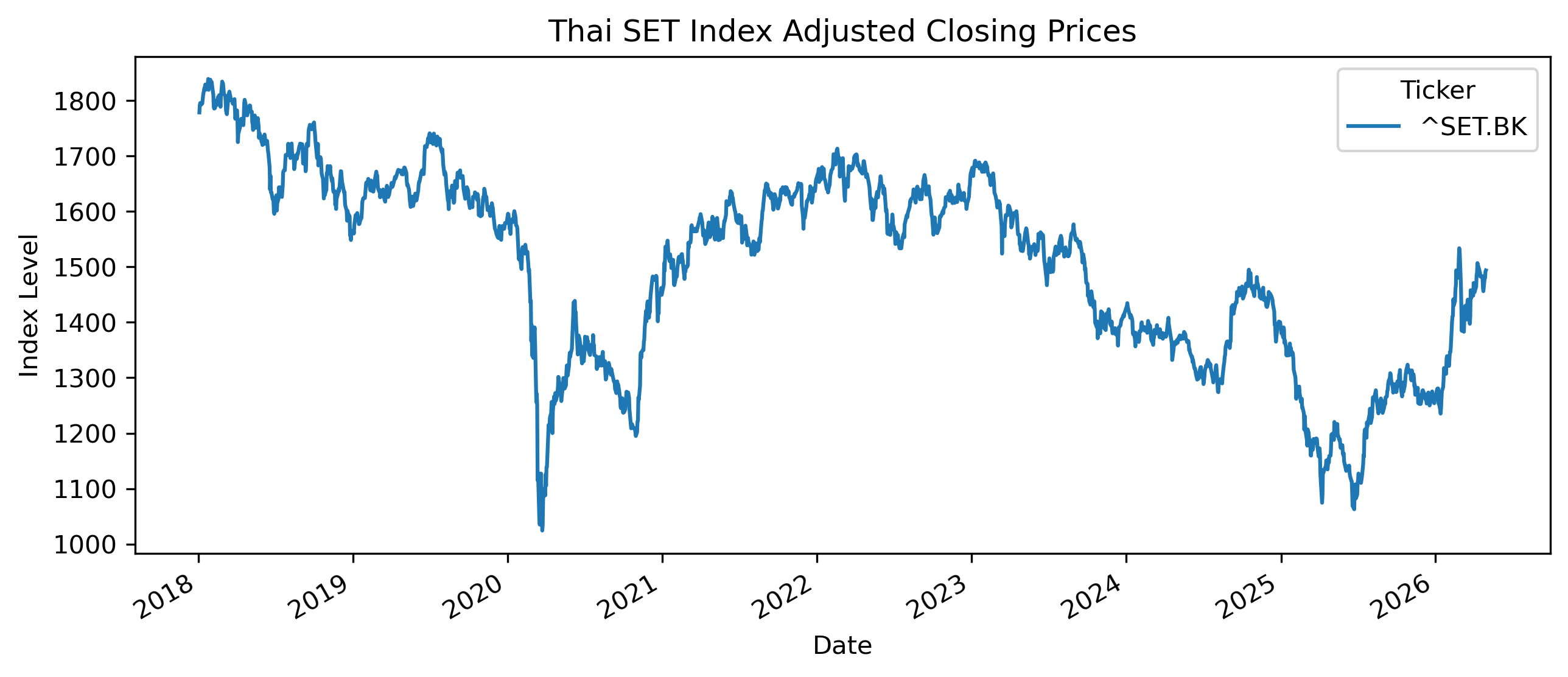

Exercise 1 — Downloading and Visualizing Prices¶

We begin by downloading adjusted price data.

import yfinance as yf

import matplotlib.pyplot as plt

# Download SET Index data

set_index = yf.download(

"^SET.BK",

start="2018-01-01",

auto_adjust=False

)

# Adjusted closing prices

prices = set_index["Adj Close"]

# Plot

prices.plot(figsize=(10,4))

plt.title("Thai SET Index Adjusted Closing Prices")

plt.ylabel("Index Level")

plt.xlabel("Date")

plt.savefig("figs/ch4_/set.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

# Save CSV file

set_index.to_csv(

"figs/ch4_/set.csv")Questions¶

Does the series appear stationary?

Can you identify periods of:

rapid growth,

sharp decline,

unusual volatility?

Why might adjusted prices be preferable to raw prices?

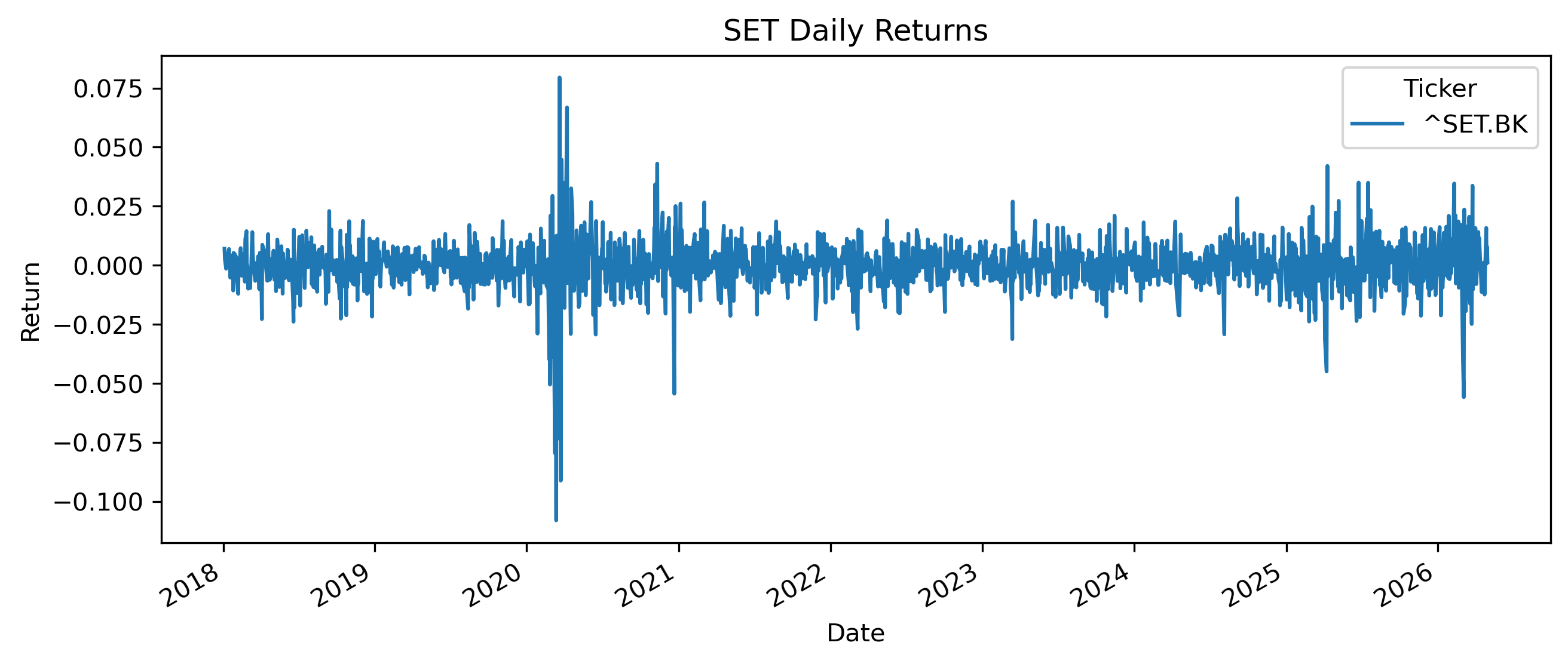

Exercise 2 — Computing Returns¶

We now compute simple returns.

returns = prices.pct_change().dropna()

returns.head()Plotting Returns¶

returns.plot(figsize=(10,4))

plt.title("SET Daily Returns")

plt.ylabel("Return")

plt.savefig("figs/ch4_/returns.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Questions¶

How does the return series differ visually from the price series?

Does the return series appear more stationary?

Can you identify periods of elevated volatility?

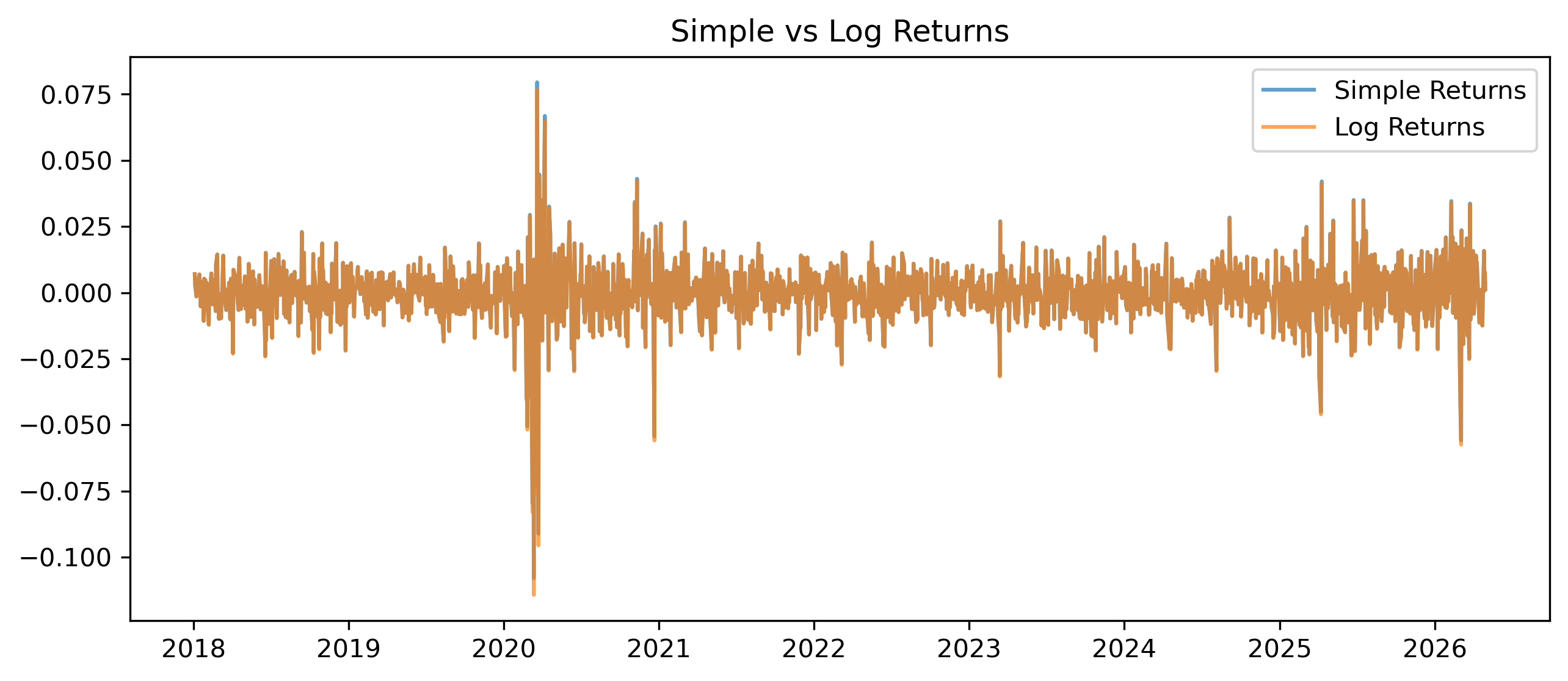

Exercise 3 — Simple vs Log Returns¶

We now compute log returns.

import numpy as np

log_returns = np.log(

prices / prices.shift(1)

).dropna()

log_returns.head()Comparing Returns¶

comparison = plt.figure(figsize=(10,4))

plt.plot(

returns.index,

returns,

label="Simple Returns",

alpha=0.7

)

plt.plot(

log_returns.index,

log_returns,

label="Log Returns",

alpha=0.7

)

plt.legend()

plt.title("Simple vs Log Returns")

plt.savefig("figs/ch4_/returns2.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Questions¶

Are simple and log returns very different for daily data?

Why do economists and finance researchers often prefer log returns?

Under what circumstances might differences become larger?

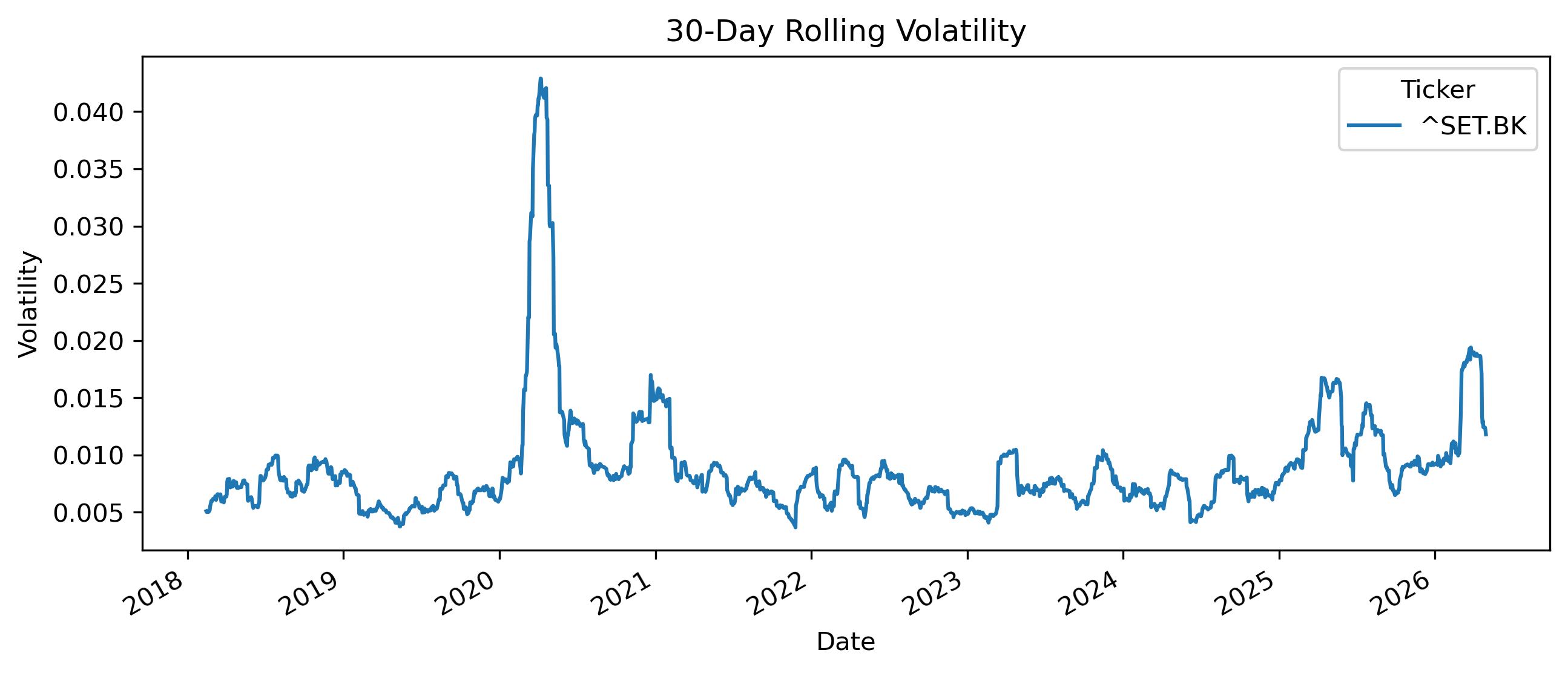

Exercise 4 — Measuring Volatility¶

Volatility measures variability in returns.

One simple measure is the standard deviation.

Daily Volatility¶

returns.std()Rolling Volatility¶

rolling_vol = returns.rolling(30).std()

rolling_vol.plot(figsize=(10,4))

plt.title("30-Day Rolling Volatility")

plt.ylabel("Volatility")

plt.savefig("figs/ch4_/rol_vol.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Questions¶

Does volatility appear constant over time?

Can you identify periods of volatility clustering?

Why might volatility matter for investors?

This becomes central later when we study:

ARCH models,

and GARCH models.

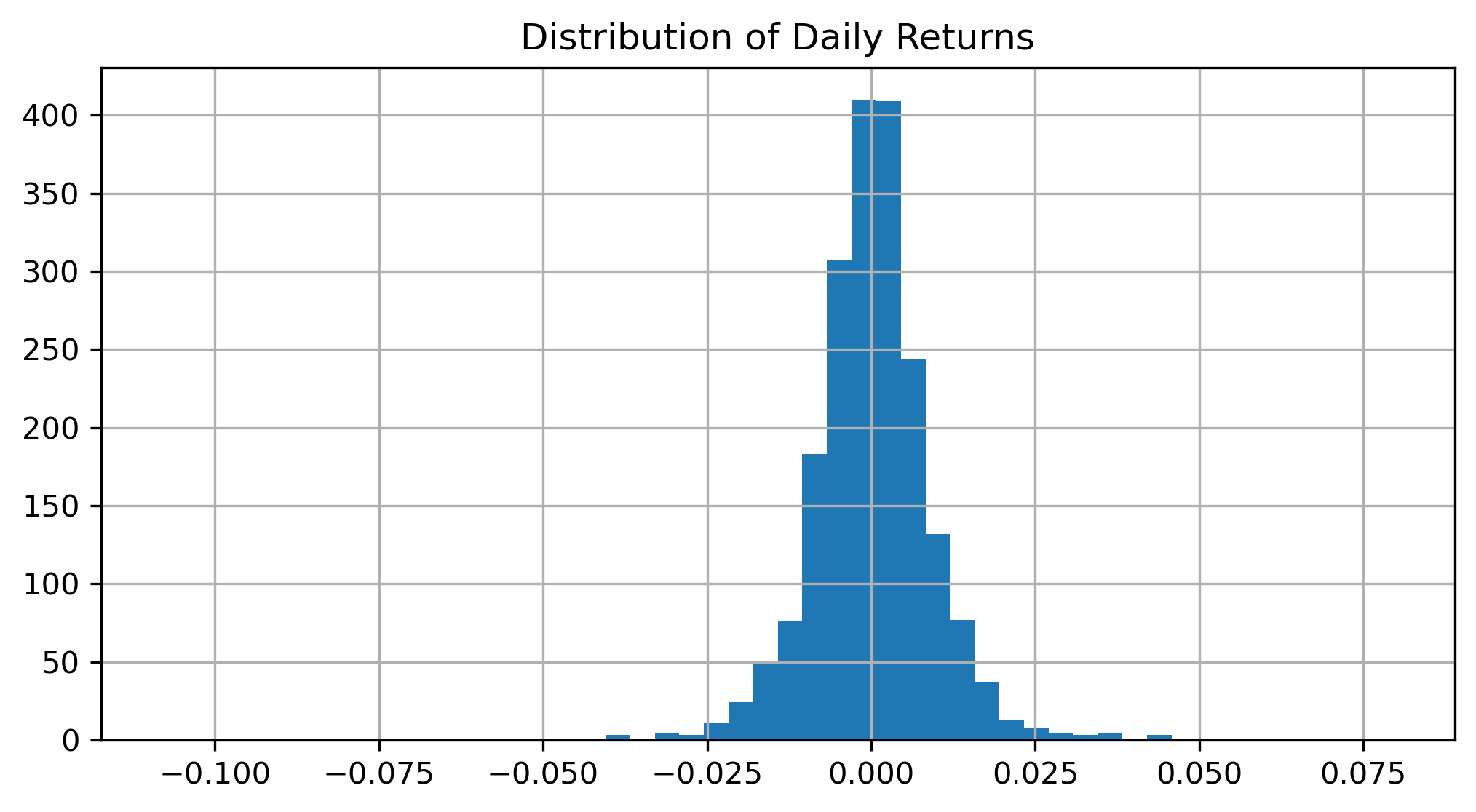

Exercise 5 — Distribution of Returns¶

We now examine the distribution of returns.

returns.hist(

bins=50,

figsize=(8,4)

)

plt.title("Distribution of Daily Returns")

plt.savefig("figs/ch4_/ret_dist.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Questions¶

Does the distribution appear perfectly normal?

Are extreme observations present?

Why might extreme returns matter in finance?

Exercise 6 — Comparing Assets¶

We now compare multiple assets.

aapl = yf.download(

"AAPL",

start="2018-01-01",

auto_adjust=False

)["Adj Close"]

nflx = yf.download(

"NFLX",

start="2018-01-01",

auto_adjust=False

)["Adj Close"]

comparison = plt.figure(figsize=(10,4))

plt.plot(

aapl / aapl.iloc[0],

label="Apple"

)

plt.plot(

nflx / nflx.iloc[0],

label="NetFlix"

)

plt.legend()

plt.title("Normalized Stock Prices")

plt.show()Questions¶

Why do we normalize prices before comparison?

Which asset performed better over the sample?

Which asset appears more volatile?

Exercise 7 — Short Selling and Negative Returns¶

Suppose an investor expects prices to fall.

One possible strategy is:

A short seller:

borrows an asset,

sells it today,

and hopes to repurchase it later at a lower price.

Example¶

Suppose:

| Day | Price |

|---|---|

| 1 | 100 |

| 2 | 90 |

Long Position Return¶

The investor loses 10%.

Short Position Return¶

The short seller gains 10%.

Questions¶

Why are short positions risky?

Why can short-selling losses become very large?

Why might short-selling be economically useful?

Exercise 8 — Interpreting Stylized Facts¶

Using the exercises above, identify examples of:

volatility clustering,

fat tails,

trends,

noise,

nonstationarity.

These patterns strongly influence modern time series modeling.

Mini Project — Exploring Thai Financial Data¶

Choose one Thai financial asset, such as:

SET Index,

SET50,

Thai baht exchange rate,

a major Thai stock.

Then:

Download the data.

Compute returns.

Plot prices and returns.

Measure volatility.

Compare simple and log returns.

Discuss stylized facts.

Gretl Version¶

The same exercises can also be performed in Gretl and/or Excel.

Downloading Data¶

Import CSV or Excel financial data.

Plotting Data¶

Menu:

Variable → Time series plotComputing Returns¶

Menu:

Add → Define new variableExample:

return = (P - P(-1))/P(-1)Or.

Right click on AdjClose and Add percent change...

Histogram¶

Menu:

Variable → Frequency distribution

Common Mistakes¶

Looking Ahead¶

Part II begins studying:

trends,

smoothing,

filtering,

and trading indicators.

We move from:

toward: