Chapter 9 — ACF and PACF

In previous chapters, we introduced dependence, persistence, and stationarity.

We now develop two of the most important tools in time series analysis:

the autocorrelation function (ACF)

the partial autocorrelation function (PACF)

These tools help us understand:

dependence across time

persistence

lag structure

model identification

Learning Objectives¶

By the end of this chapter, you should be able to:

understand autocorrelation and autocovariance

interpret ACF and PACF plots

recognize dependence patterns

distinguish white noise and persistent processes

use ACF/PACF for model identification

9.1 Correlation Across Time¶

In time series analysis, we study relationships such as:

where (h) is the lag.

9.2 Autocovariance and ACF¶

For a weakly stationary process:

The autocorrelation function (ACF) is:

where (\gamma(0) = Var(X_t)).

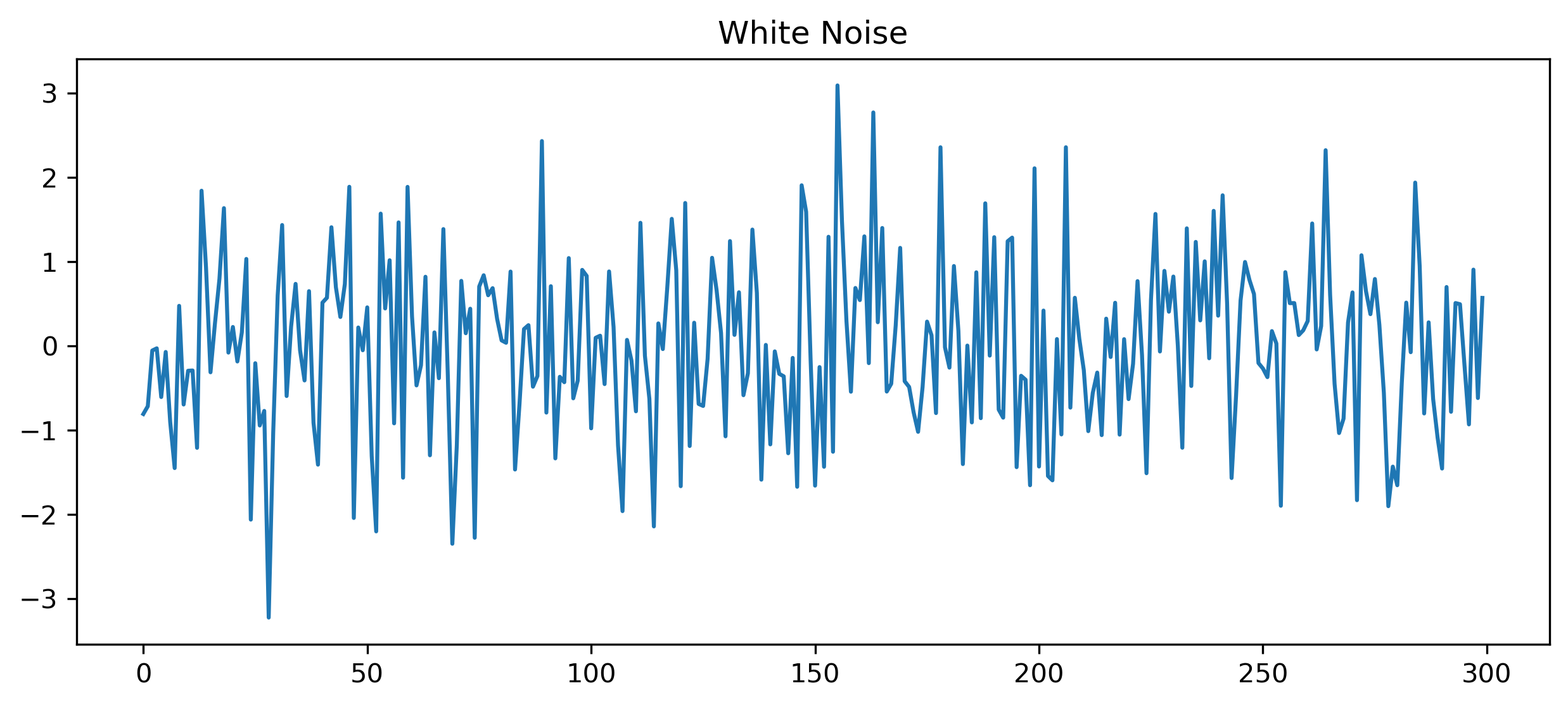

9.3 White Noise: No Dependence¶

Simulation¶

Source

import numpy as np

import matplotlib.pyplot as plt

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

np.random.seed(10101)

wn = np.random.normal(0, 1, 300)

plt.figure(figsize=(10,4))

plt.plot(wn)

plt.title("White Noise")

plt.savefig("figs/ch9/wn.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

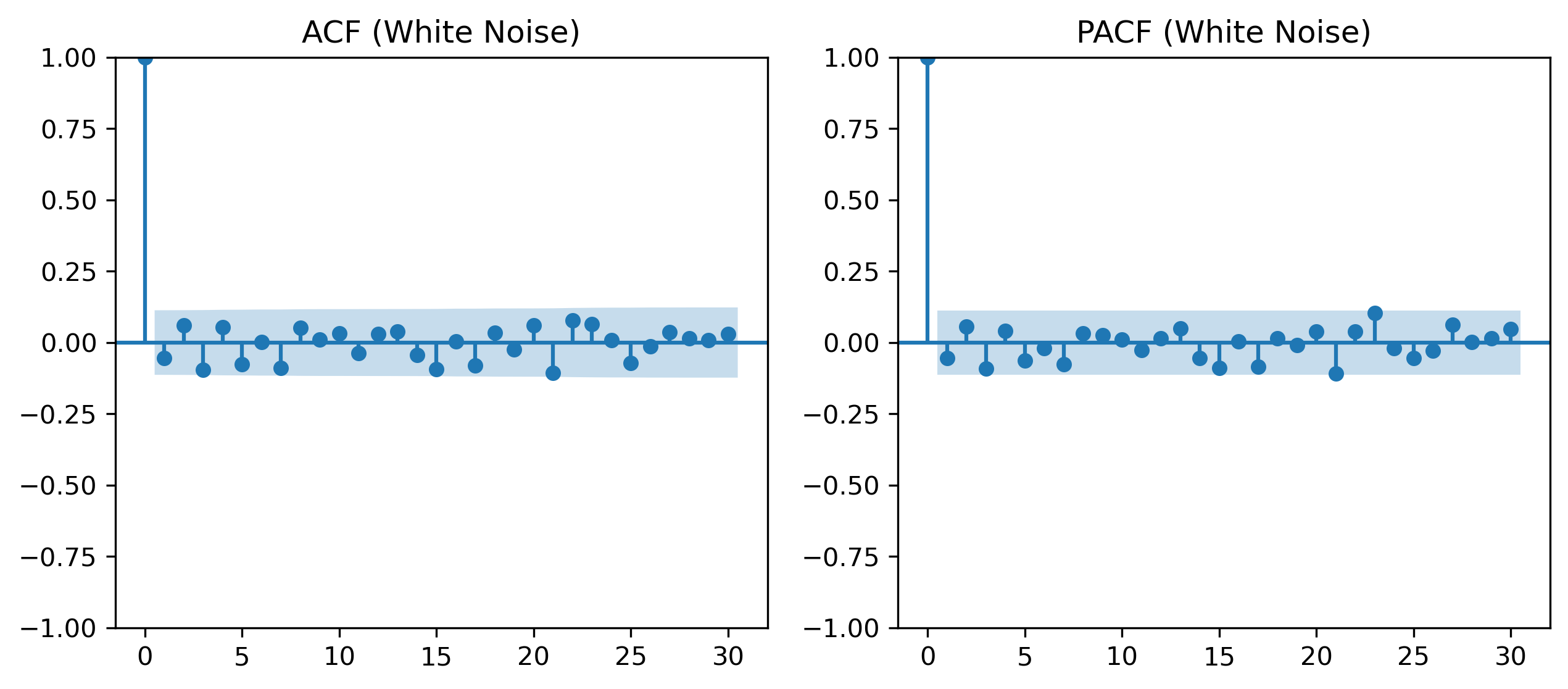

ACF and PACF¶

Source

fig, ax = plt.subplots(1,2, figsize=(10,4))

plot_acf(wn, lags=30, ax=ax[0])

ax[0].set_title("ACF (White Noise)")

plot_pacf(wn, lags=30, ax=ax[1], method="ywm")

ax[1].set_title("PACF (White Noise)")

plt.savefig("figs/ch9/wn_acf_pacf.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

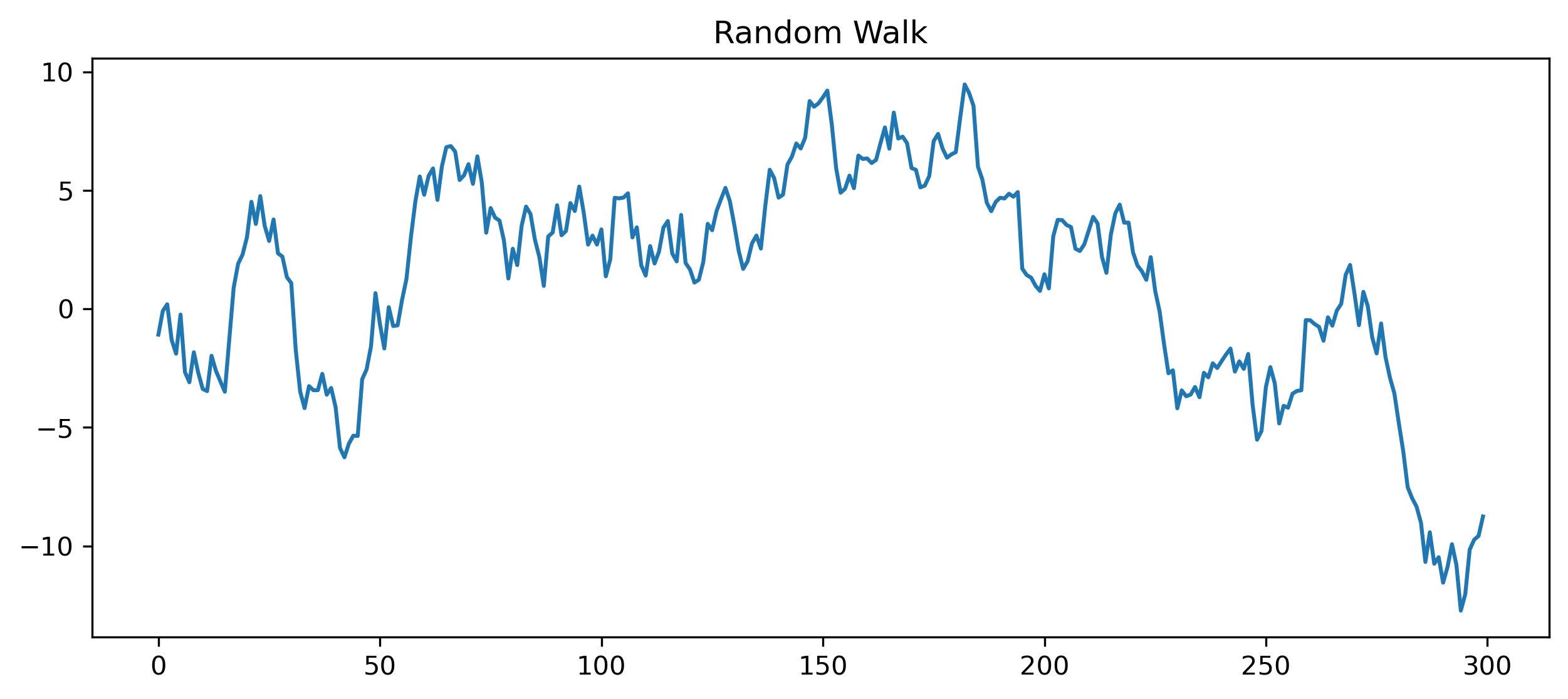

9.4 Persistent Series: Random Walk¶

Simulation¶

Source

np.random.seed(123)

w = np.random.normal(0, 1, 300)

x = np.cumsum(w)

plt.figure(figsize=(10,4))

plt.plot(x)

plt.title("Random Walk")

plt.savefig("figs/ch9/rw.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

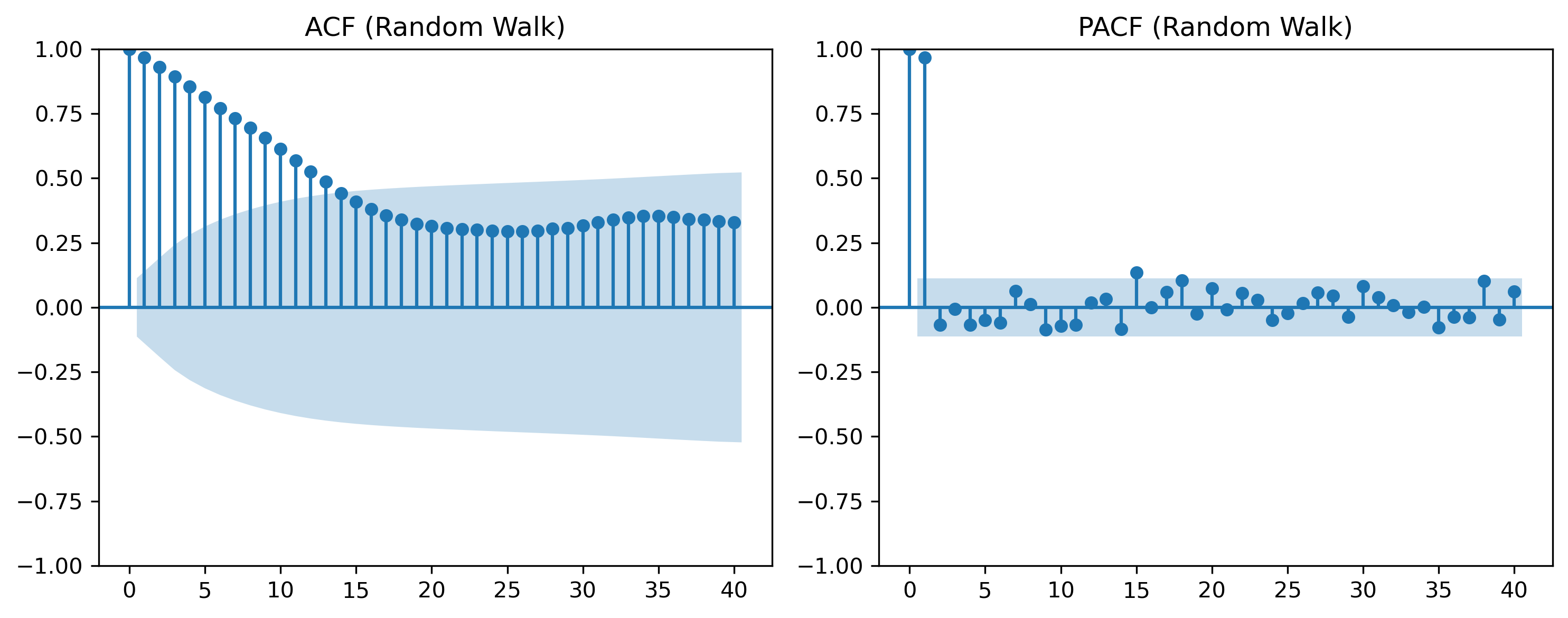

ACF and PACF¶

Source

fig, ax = plt.subplots(1,2, figsize=(10,4))

plot_acf(x, lags=40, ax=ax[0])

ax[0].set_title("ACF (Random Walk)")

plot_pacf(x, lags=40, ax=ax[1], method="ywm")

ax[1].set_title("PACF (Random Walk)")

plt.tight_layout()

plt.savefig("figs/ch9/rw_acf_pacf.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

9.5 Interpreting ACF Patterns¶

White Noise¶

ACF ≈ 0 at all lags

Persistent Series¶

ACF decays slowly

Oscillatory Behavior¶

ACF alternates signs

9.6 Partial Autocorrelation (PACF)¶

The ACF measures total dependence, including indirect effects.

The PACF isolates direct dependence.

9.7 ACF vs PACF (Intuition)¶

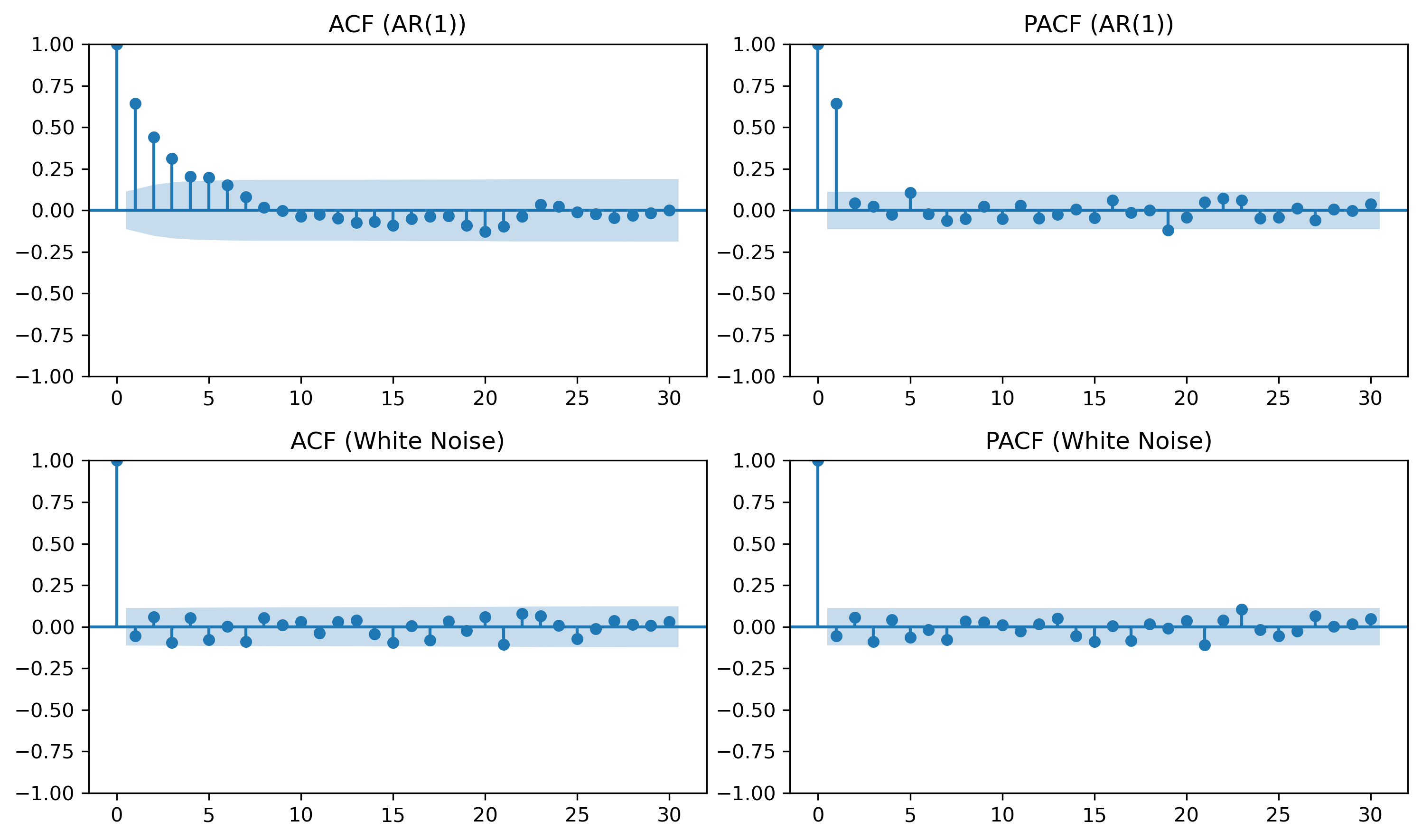

9.8 Visual Comparison¶

Source

np.random.seed(42)

# AR(1)

phi = 0.7

ar = np.zeros(300)

for t in range(1, 300):

ar[t] = phi * ar[t-1] + np.random.normal()

fig, ax = plt.subplots(2,2, figsize=(10,6))

plot_acf(ar, lags=30, ax=ax[0,0])

ax[0,0].set_title("ACF (AR(1))")

plot_pacf(ar, lags=30, ax=ax[0,1], method="ywm")

ax[0,1].set_title("PACF (AR(1))")

plot_acf(wn, lags=30, ax=ax[1,0])

ax[1,0].set_title("ACF (White Noise)")

plot_pacf(wn, lags=30, ax=ax[1,1], method="ywm")

ax[1,1].set_title("PACF (White Noise)")

plt.tight_layout()

plt.savefig("figs/ch9/acf_pacf_.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

9.9 Model Identification (Rule of Thumb)¶

| Model | ACF | PACF |

|---|---|---|

| AR(p) | decays | cuts off at p |

| MA(q) | cuts off at q | decays |

| ARMA | decays | decays |

| White noise | none | none |

9.10 Confidence Bands¶

ACF/PACF plots include approximate bounds:

9.11 Economic and Financial Insight¶

Macroeconomic variables → persistent

Financial returns → weak autocorrelation

Volatility → highly persistent

9.12 Looking Ahead¶

ACF and PACF help diagnose dependence patterns.

Next, we study:

unit roots

nonstationarity

differencing

which explain whether persistence is temporary or permanent.

Key Takeaways¶

Concept Check¶

Basic¶

What is autocorrelation?

What does the autocorrelation function (ACF) measure?

What is a lag?

Intuition¶

Why do we examine correlations across time in a time series?

What does a high autocorrelation at lag 1 suggest?

What does it mean if autocorrelations decay slowly?

Intermediate¶

What is the difference between:

ACF

PACF

Why is PACF useful in time series analysis?

What does it mean if autocorrelations are close to zero at all lags?

Interpretation¶

What pattern would you expect in the ACF of:

white noise

a persistent series

Challenge¶

Suppose the ACF shows strong values at many lags.

What does this suggest about the series?

Why might this indicate nonstationarity?

Interpretation & Practice¶

ACF values are close to zero at all lags.

What type of process is this likely?

Why?

ACF shows a large value at lag 1, then quickly drops to zero.

What does this suggest about dependence?

What type of process might generate this?

ACF decays slowly over many lags.

What does this indicate?

Why might this suggest nonstationarity?

PACF shows a sharp cutoff after lag 1.

What does this imply?

Why is this useful for model identification?

ACF alternates between positive and negative values.

What type of behavior might this indicate?

What does this suggest about the series dynamics?

Finance Interpretation¶

A return series shows very low autocorrelation.

What does this imply about predictability?

How does this relate to market efficiency?

A volatility series shows strong autocorrelation.

What does this suggest?

Why is this important in finance?

Challenge¶

Suppose both ACF and PACF show no clear pattern.

What type of process might this be?

Why is model identification difficult in this case?

Numerical Practice¶

Identifying Autocorrelation¶

Consider the following series:

2, 4, 6, 8, 10

Does this series show dependence over time?

Would you expect high autocorrelation?

Why?

Consider:

3, −1, 2, −2, 1, 0

Does this series appear random?

Would you expect autocorrelation to be high or low?

Lag Interpretation¶

Suppose:

What does this imply?

Is the series highly dependent?

Suppose:

What does this suggest about predictability?

ACF Patterns¶

Match the pattern:

ACF ≈ 0 for all lags

ACF slowly decays

ACF cuts off quickly

To the likely process:

white noise

persistent series

short-memory process

Challenge¶

Suppose a series has:

strong autocorrelation at lag 1

weak autocorrelation afterward

What type of model might describe this?

Why?

Appendix 9A — Understanding PACF¶

The PACF can be interpreted as the correlation between:

and

after removing the effect of intermediate lags.

This can be obtained by:

Regressing on intermediate lags

Regressing on the same variables

Taking the correlation between residuals