Chapter 14 — ARIMA Models

In the previous chapters, we studied:

autoregressive (AR) models

moving average (MA) models

ARMA models

These models assume that the underlying process is stationary.

However, many economic and financial time series are not stationary.

Examples include:

stock prices

GDP

exchange rates

price indices

These series often exhibit:

trends

persistent drift

unit roots

The solution is to transform the data before modeling.

Learning Objectives¶

By the end of this chapter, you should be able to:

understand the motivation behind ARIMA models

distinguish stationary and integrated processes

understand the role of differencing

define ARIMA() models

interpret the Box–Jenkins workflow

estimate ARIMA models in Gretl

evaluate residual diagnostics and model fit

14.1 Why ARIMA Models?¶

Many real-world time series exhibit strong persistence and nonstationarity.

For example:

stock prices drift over time

GDP tends to grow

inflation may exhibit persistent trends

Applying stationary ARMA models directly to such data may produce misleading results.

14.2 Differencing Revisited¶

Recall the first difference operator:

Differencing removes persistent stochastic trends.

Example: Random Walk¶

Suppose:

Then:

which is white noise.

14.3 Integrated Processes¶

First Difference¶

Second Difference¶

or:

14.4 The ARIMA Model¶

General Form¶

After differencing times:

where:

is the AR polynomial

is the differencing operator

is the MA polynomial

14.5 Understanding the Components¶

AR Component¶

Captures persistence through past values.

I Component¶

Captures nonstationarity through differencing.

MA Component¶

Captures temporary propagation of shocks.

14.6 Example: ARIMA(0,1,0)¶

Consider:

or:

Thus:

14.7 Example: ARIMA(1,1,0)¶

Suppose:

or equivalently:

14.8 Example: ARIMA(0,1,1)¶

Suppose:

Then:

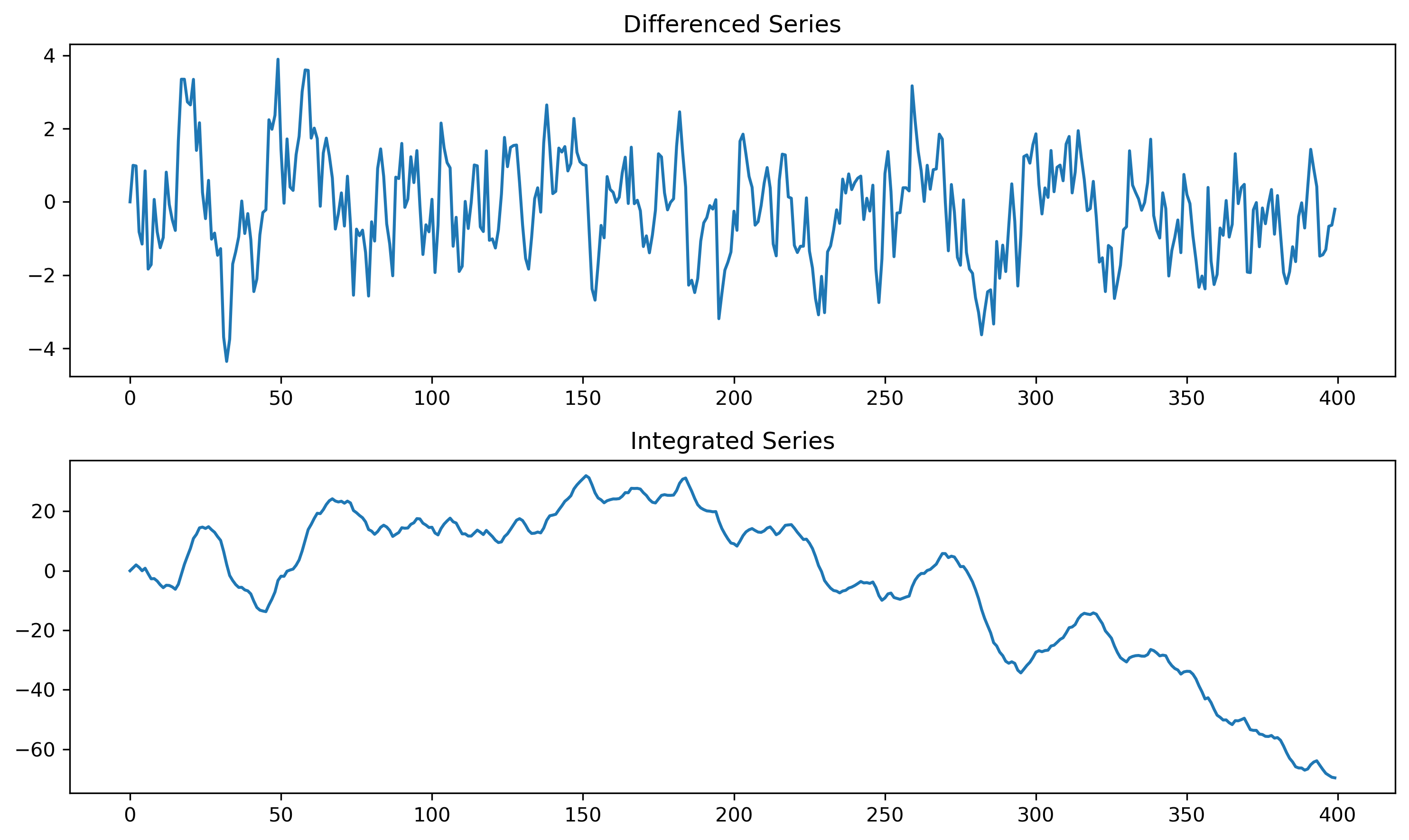

14.9 Simulating an ARIMA Process¶

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(123)

n = 400

phi = 0.7

w = np.random.normal(size=n)

dx = np.zeros(n)

for t in range(1,n):

dx[t] = phi*dx[t-1] + w[t]

x = np.cumsum(dx)

fig, ax = plt.subplots(2,1, figsize=(10,6))

ax[0].plot(dx)

ax[0].set_title("Differenced Series")

ax[1].plot(x)

ax[1].set_title("Integrated Series")

plt.tight_layout()

plt.savefig("figs/ch14/ARIMA.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

14.10 The Box–Jenkins Methodology¶

Classical ARIMA modeling follows the Box–Jenkins approach.

Step 1 — Identification¶

plot the data

check stationarity

difference if necessary

examine ACF/PACF

Step 2 — Estimation¶

Estimate candidate ARIMA models.

Step 3 — Diagnostic Checking¶

Check whether residuals resemble white noise.

Step 4 — Forecasting¶

Generate forecasts and evaluate performance.

14.11 Identifying Differencing Order¶

A series may require differencing if:

it exhibits persistent trends

ACF decays very slowly

unit root tests fail to reject nonstationarity

14.12 Under-Differencing vs Over-Differencing¶

Under-Differencing¶

residual nonstationarity remains

strong persistence persists

Over-Differencing¶

introduces excess noise

may create artificial negative autocorrelation

14.13 ACF and PACF in ARIMA Modeling¶

After differencing:

examine ACF

examine PACF

identify possible AR and MA orders

Typical Patterns¶

| Model | ACF | PACF |

|---|---|---|

| AR() | tails off | cuts off |

| MA() | cuts off | tails off |

| ARMA() | tails off | tails off |

14.14 Estimation in Gretl¶

Menu¶

Model → Time Series → ARIMATypical Workflow¶

plot the series

test for unit roots

difference if needed

inspect ACF/PACF

estimate candidate models

compare AIC/BIC

check residuals

[GRETL Screenshot Placeholder: ARIMA estimation dialog][GRETL Screenshot Placeholder: ARIMA output]14.15 Residual Diagnostics¶

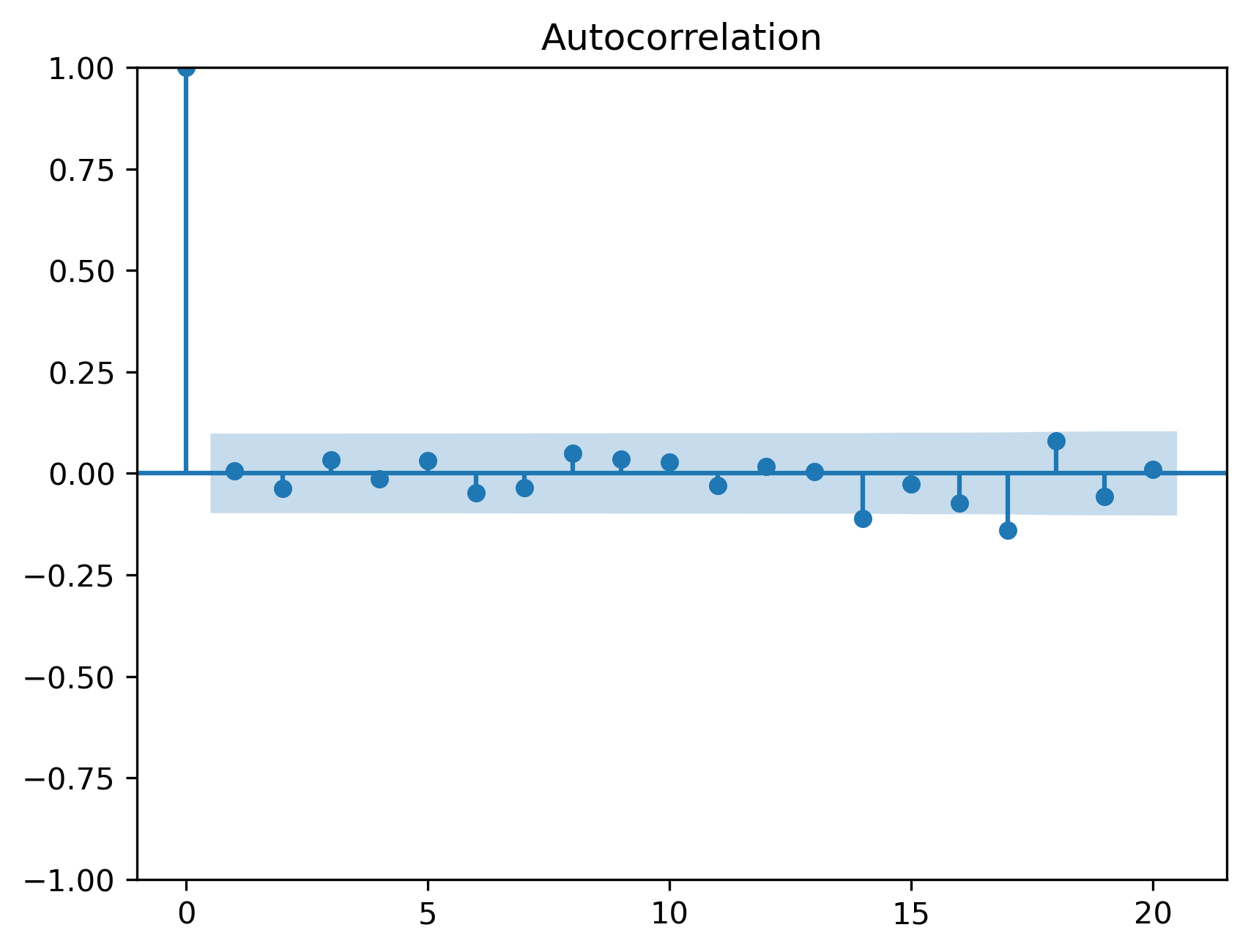

Residuals should resemble white noise.

Residual ACF¶

import statsmodels.api as sm

from statsmodels.graphics.tsaplots import plot_acf

model = sm.tsa.ARIMA(x, order=(1,1,0))

res = model.fit()

plot_acf(res.resid, lags=20)

plt.savefig("figs/ch14/acf.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Ljung–Box Test¶

from statsmodels.stats.diagnostic import acorr_ljungbox

acorr_ljungbox(res.resid, lags=[10,20], return_df=True)| | lb_stat | lb_pvalue |

|---------|------------|-----------|

| 10 | 4.729113 | 0.908524 |

| 20 | 25.169131 | 0.195037 |

14.16 Information Criteria¶

Model selection often uses:

AIC

BIC

Akaike Information Criterion¶

Bayesian Information Criterion¶

14.17 Forecasting with ARIMA Models¶

Once estimated, ARIMA models can generate forecasts.

Multi-Step Forecasts¶

Forecasts are generated recursively using:

past observations

estimated parameters

projected future dynamics

14.18 ARIMA Models in Economics and Finance¶

ARIMA models are widely used for:

GDP forecasting

inflation forecasting

demand forecasting

exchange rates

inventory management

energy consumption

14.19 Common Mistakes¶

14.20 Looking Ahead¶

In this chapter, we extended ARMA models to handle nonstationary series through differencing.

We now move to forecasting and forecast evaluation, where we study:

static vs dynamic forecasting

forecast accuracy

RMSE, MAE, MAPE

Theil’s U statistics

Key Takeaways¶

Concept Check¶

Basic¶

What is an ARIMA model?

What does the “I” in ARIMA represent?

What does differencing do to a time series?

Intuition¶

Why are many economic time series nonstationary?

Why is it problematic to apply ARMA models to nonstationary data?

What is the idea behind transforming data before modeling?

Intermediate¶

What does it mean for a series to be:

What is the difference between first and second differencing?

Why is most real-world data rather than ?

ARIMA Structure¶

What do , , and represent in ARIMA()?

What happens after differencing is applied?

Challenge¶

Suppose a series becomes stationary after differencing once.

What does this imply?

Interpretation & Practice¶

A time series shows a strong upward trend.

What transformation might be needed?

After differencing, the series fluctuates around zero.

What does this suggest?

A series exhibits very slow ACF decay.

What does this indicate?

After differencing, ACF shows AR-type behavior.

What does this suggest?

A series still appears nonstationary after differencing once.

What might you do next?

Finance Interpretation¶

Stock prices are nonstationary.

Why are returns preferred for modeling?

A return series appears stationary.

Why is this useful?

Challenge¶

A model fits well but uses .

Why might this be problematic?

Model Selection (AIC & BIC)¶

Suppose you estimate two ARIMA models:

| Model | AIC | BIC |

|---|---|---|

| ARIMA(1,1,1) | 520 | 540 |

| ARIMA(2,1,2) | 510 | 560 |

Which model is preferred according to AIC?

Which model is preferred according to BIC?

Why might these criteria disagree?

Suppose you estimate:

| Model | AIC | BIC |

|---|---|---|

| ARIMA(1,1,0) | 600 | 610 |

| ARIMA(3,1,2) | 590 | 640 |

Which model has better fit?

Which model penalizes complexity more?

Which would you choose, and why?

Explain the intuition behind:

What does the first term measure?

What does the second term penalize?

Why does BIC typically select simpler models than AIC?

Interpretation¶

A model has very low AIC but performs poorly out-of-sample.

What might be happening?

Why is model validation important?

Challenge¶

Suppose you keep adding lags to improve fit.

What happens to AIC?

What happens to BIC?

Why is this important for model selection?

Numerical Practice¶

Differencing¶

Given:

Compute

Compute second differences.

Identification¶

Suppose:

ACF decays slowly

series trends

What transformation is needed?

Suppose after differencing:

ACF cuts off after lag 1

What model is suggested?

Model Structure¶

Interpret:

What is being modeled?

Diagnostics¶

Residuals still show autocorrelation.

What does this imply?

Challenge¶

Suppose you over-difference a series.

What happens?

Why is this problematic?

Appendix 14A — Understanding Differencing and Integration¶

A.1 First Difference¶

This removes linear stochastic trends.

A.2 Random Walk Example¶

Then:

A.3 Second Difference¶

Used for stronger nonstationarity.

A.4 Why Differencing Works¶

Nonstationary series accumulate shocks:

Differencing removes this accumulation: