Chapter 11 — Autoregressive Models

In previous chapters, we studied:

stationarity

autocorrelation

persistence

unit roots and differencing

We are now ready to build formal stochastic models for stationary time series.

One of the most important and widely used classes of models is the autoregressive (AR) model.

Many economic and financial variables adjust gradually rather than instantaneously. Inflation, unemployment, interest rates, exchange rates, and GDP growth all tend to exhibit inertia or persistence.

Autoregressive models capture this gradual adjustment process mathematically.

Learning Objectives¶

By the end of this chapter, you should be able to:

understand the logic of autoregressive models

define AR() processes

interpret persistence

understand stationarity conditions

interpret ACF and PACF patterns

simulate AR models

estimate simple AR models

perform basic diagnostics

11.1 The Basic Idea¶

A simple model is:

where:

is the current value

measures persistence

is white noise

11.2 The AR(1) Model¶

Mean¶

11.3 Mean-Centered Form¶

11.4 Recursive Representation (Key Insight)¶

By repeated substitution:

11.5 Stationarity¶

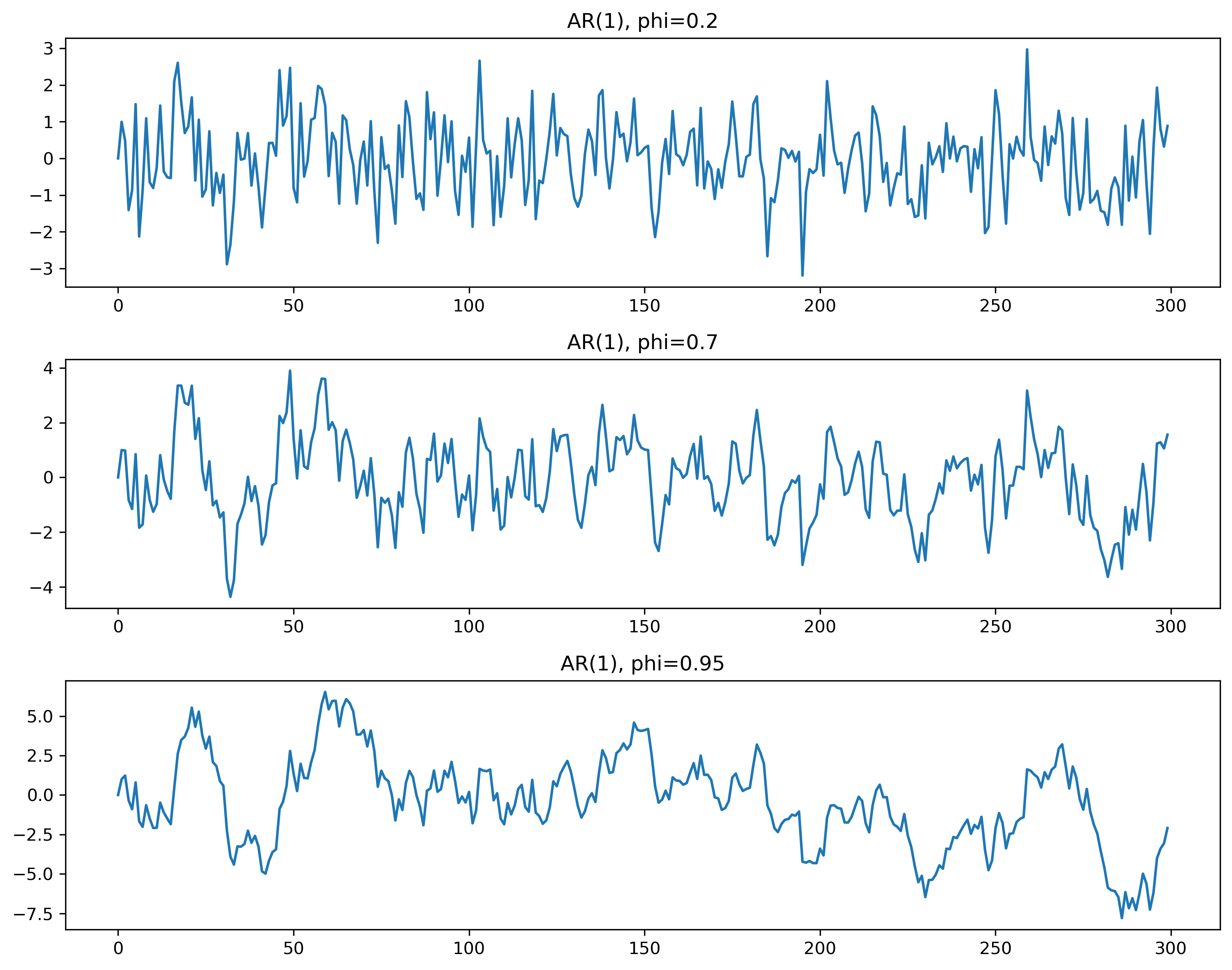

11.6 Simulation¶

Source

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(123)

n = 300

w = np.random.normal(size=n)

phis = [0.2, 0.7, 0.95]

fig, ax = plt.subplots(3,1, figsize=(10,8))

for i, phi in enumerate(phis):

x = np.zeros(n)

for t in range(1,n):

x[t] = phi*x[t-1] + w[t]

ax[i].plot(x)

ax[i].set_title(f"AR(1), phi={phi}")

plt.tight_layout()

plt.savefig("figs/ch10/persistence.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

11.7 Variance¶

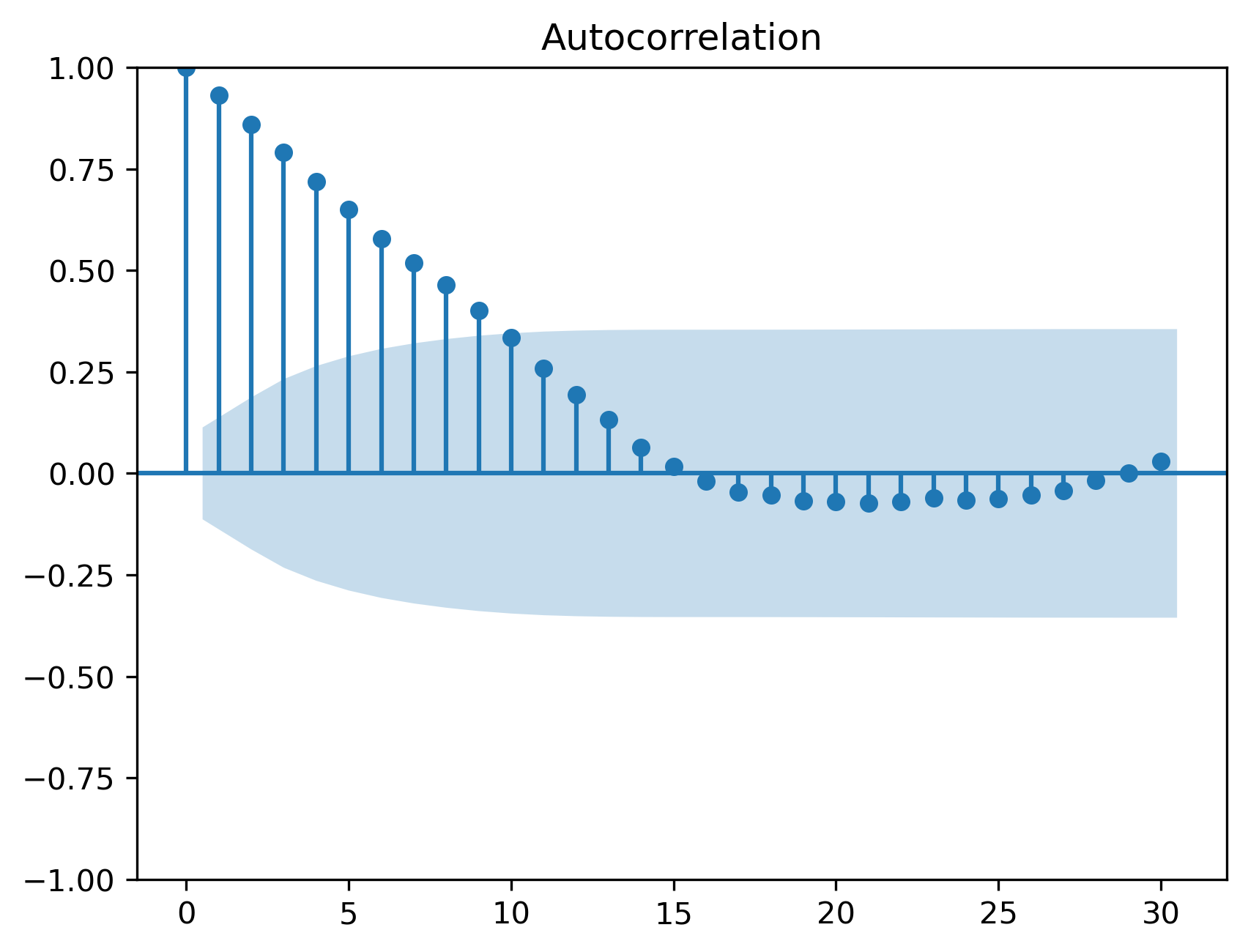

11.8 ACF of AR(1)¶

11.9 Simulated ACF¶

Source

from statsmodels.graphics.tsaplots import plot_acf

plot_acf(x, lags=30)

plt.savefig("figs/ch10/acf.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

11.10 PACF of AR(1)¶

11.11 AR(2) Model¶

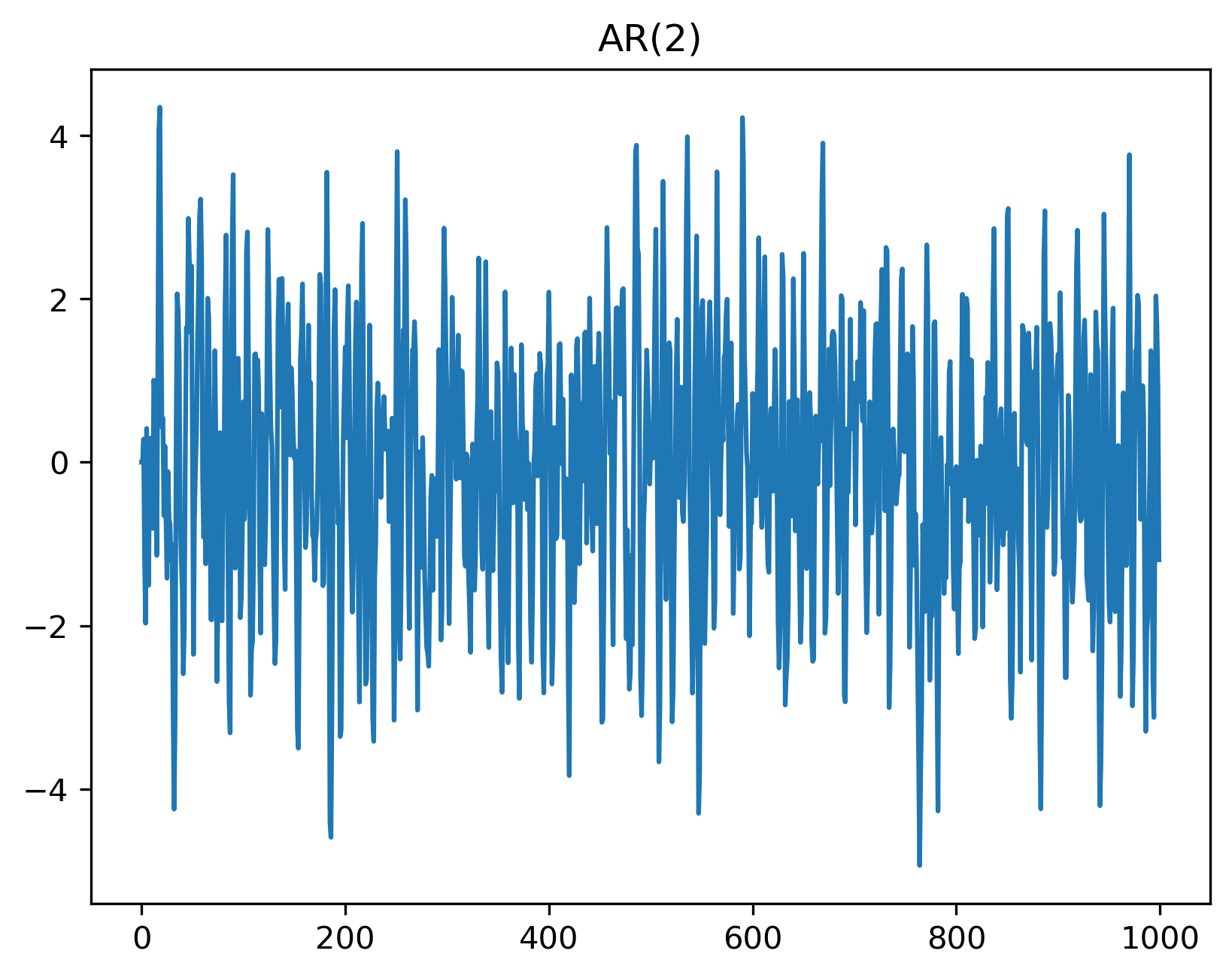

11.12 AR(2) Simulation¶

Source

np.random.seed(123)

phi1, phi2 = 1.0, -0.6

n = 1000

w = np.random.normal(size=n)

x = np.zeros(n)

for t in range(2,n):

x[t] = phi1*x[t-1] + phi2*x[t-2] + w[t]

plt.plot(x)

plt.title("AR(2)")

plt.savefig("figs/ch10/ar2.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

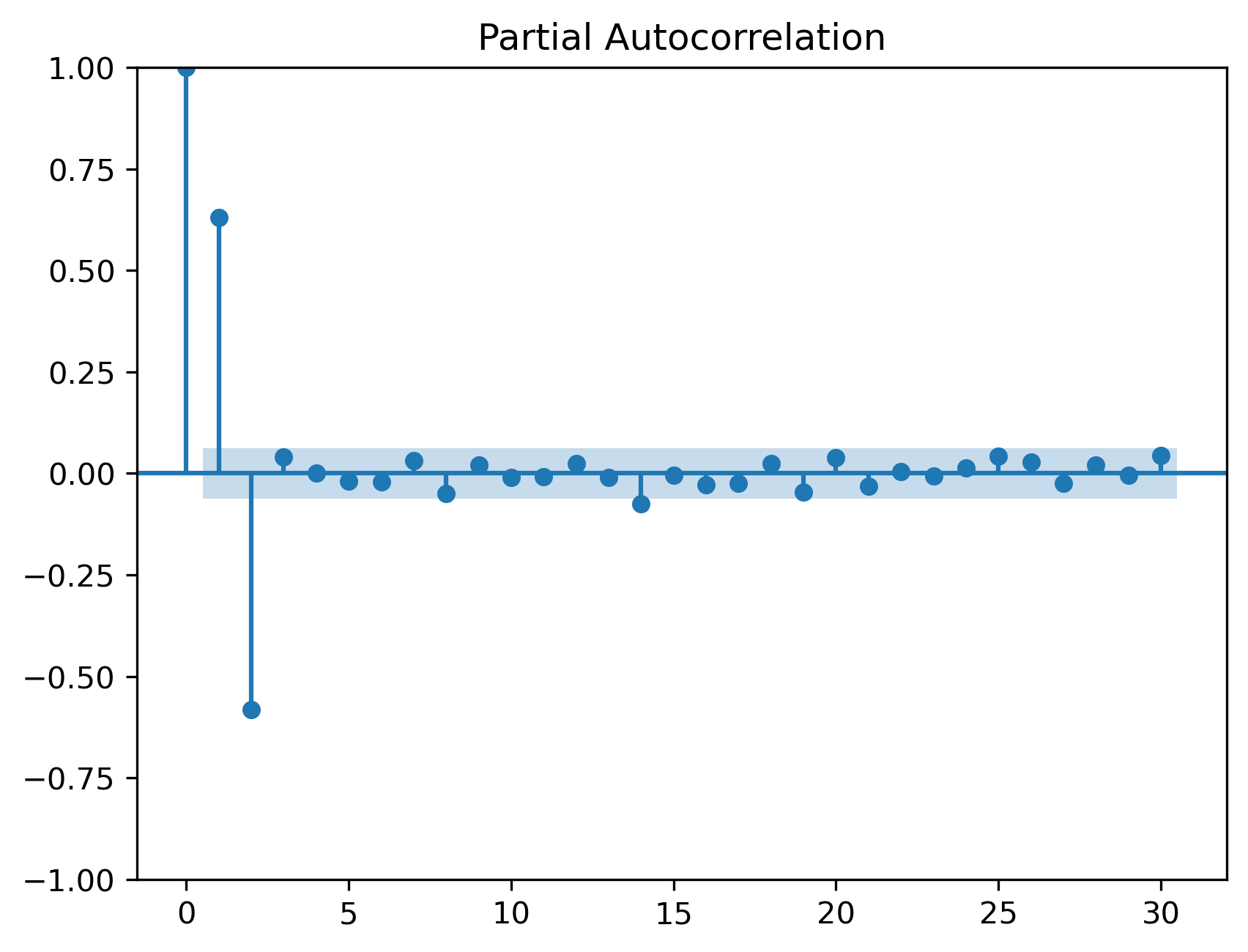

11.13 ACF and PACF for AR(2)¶

Source

from statsmodels.graphics.tsaplots import plot_pacf

plot_acf(x, lags=30)

plot_pacf(x, lags=30)

plt.savefig("figs/ch11/ar2_acf_pacf.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

11.14 General AR(p)¶

11.15 Estimation in Python¶

Source

from statsmodels.tsa.ar_model import AutoReg

model = AutoReg(x, lags=2)

res = model.fit()

print(res.summary()) AutoReg Model Results

==============================================================================

Dep. Variable: y No. Observations: 1000

Model: AutoReg(2) Log Likelihood -1416.520

Method: Conditional MLE S.D. of innovations 1.000

Date: Mon, 04 May 2026 AIC 2841.040

Time: 21:40:24 BIC 2860.663

Sample: 2 HQIC 2848.499

1000

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0386 0.032 -1.218 0.223 -0.101 0.024

y.L1 1.0000 0.026 38.890 0.000 0.950 1.050

y.L2 -0.5850 0.026 -22.746 0.000 -0.635 -0.535

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 0.8547 -0.9894j 1.3074 -0.1366

AR.2 0.8547 +0.9894j 1.3074 0.1366

-----------------------------------------------------------------------------11.16 Residual Diagnostics¶

Source

from statsmodels.stats.diagnostic import acorr_ljungbox

lb = acorr_ljungbox(res.resid, lags=[10,20], return_df=True)

lb| | lb_stat | lb_pvalue |

|---------|------------|-----------|

| 10 | 6.476702 | 0.773750 |

| 20 | 18.268325 | 0.569737 |

11.17 Information Criteria¶

11.18 Common Mistakes¶

11.19 Looking Ahead¶

Next:

MA models

ARMA models

full modeling workflow

Key Takeaways¶

Concept Check¶

Basic¶

What is an autoregressive (AR) model?

What does the parameter represent in an AR(1) model?

What is the role of the error term ?

Intuition¶

What does it mean for a time series to exhibit persistence?

How does the value of affect the behavior of the series?

What happens when is:

close to zero

close to one

negative

Intermediate¶

What is the stationarity condition for an AR(1) model?

Why must shocks decay over time in a stationary process?

What is the difference between:

AR(1)

AR(2)

ACF & PACF¶

What pattern does the ACF of an AR(1) process exhibit?

What pattern does the PACF of an AR(1) process exhibit?

Why does the PACF “cut off” for an AR process?

Finance Insight¶

Why are AR models useful in modeling economic or financial time series?

Why is strong persistence sometimes mistaken for a trend?

Challenge¶

Suppose .

Is the process stationary?

How would it behave in practice?

Interpretation & Practice¶

A time series shows gradual adjustment after shocks.

What type of model might describe this?

Why?

A series appears highly persistent but does not trend upward.

What does this suggest about ?

Is the series likely stationary?

ACF decays slowly and smoothly.

What type of process might this indicate?

PACF shows a large spike at lag 1 and near zero afterward.

What model is suggested?

ACF shows a wavy, oscillating pattern.

What type of model might generate this?

After fitting an AR model, residuals still show autocorrelation.

What does this imply?

What should you do?

Finance Interpretation¶

A return series shows small but positive autocorrelation.

What does this imply about predictability?

Is this consistent with market efficiency?

A volatility series shows strong persistence.

Why might an AR-type structure be useful?

Challenge¶

A model fits the data well but produces poor forecasts.

What might be wrong?

What does this suggest about overfitting?

Numerical Practice¶

AR(1) Simulation Logic¶

Consider the AR(1) process:

with:

Compute

Repeat with:

Compare results

What changes?

Persistence¶

Suppose:

If , how quickly do shocks disappear?

If , how quickly do shocks disappear?

ACF Interpretation¶

Suppose you observe:

What pattern is this?

What does it suggest about ?

Model Identification¶

You observe:

ACF gradually decays

PACF cuts off after lag 2

What model is suggested?

Estimation Output¶

Suppose an estimated AR(1) model gives:

Is the series highly persistent?

Is it stationary?

What does this imply for forecasting?

Diagnostics¶

Suppose the residuals from an AR model show:

significant autocorrelation

What does this imply?

What should you do next?

Challenge¶

Suppose .

What happens to the process?

Why is this problematic?

Suppose you include too many lags in an AR model.

What is the risk?

How can information criteria help?

Appendix 11A — Mathematical Details of AR Models¶

This appendix provides additional insight into the properties of autoregressive models.

These results are not required for basic understanding, but they help explain why AR models behave the way they do.

A.1 Recursive Representation of AR(1)¶

Consider:

Substitute repeatedly:

Continuing:

A.2 Stationarity Condition¶

From the recursive form:

For this to converge, we require:

A.3 Mean of AR(1)¶

Consider:

Take expectations:

In equilibrium:

So:

A.4 Variance of AR(1)¶

From:

Take variance:

In steady state:

So:

A.5 Autocovariance Function¶

We define:

Multiply the AR(1) equation by :

Thus:

Iterating:

A.6 Autocorrelation Function¶

Since:

we obtain:

A.7 Yule–Walker Equation (AR(1))¶

At lag 0:

Rearranging:

This gives the variance result above.

A.8 AR(2): Intuition and Dynamics¶

Consider:

Unlike AR(1), this process can generate:

oscillations

cycles

damped fluctuations

A.9 Characteristic Equation¶

For AR(p):

We define the characteristic equation: