Chapter 4 — Visualizing Time Series

Before estimating models or producing forecasts, we should first look carefully at the data.

Visualization is one of the most important steps in time series analysis.

A graph often reveals features that summary statistics alone may hide.

This chapter introduces:

plotting time series,

trends,

cycles,

seasonality,

noise,

rolling averages,

and visual interpretation.

The emphasis is practical and intuition-first.

Learning Objectives¶

By the end of this chapter, you should be able to:

plot and interpret time series data

identify trends and cycles visually

distinguish signal from noise

recognize seasonality

understand rolling averages

compare multiple time series visually

use Python and Gretl to visualize data

4.1 Why Visualization Matters¶

Time series data often contain rich structure.

Plots may reveal:

trends,

volatility,

structural breaks,

outliers,

cycles,

persistence,

seasonality.

A model estimated without visual inspection may miss important features of the data.

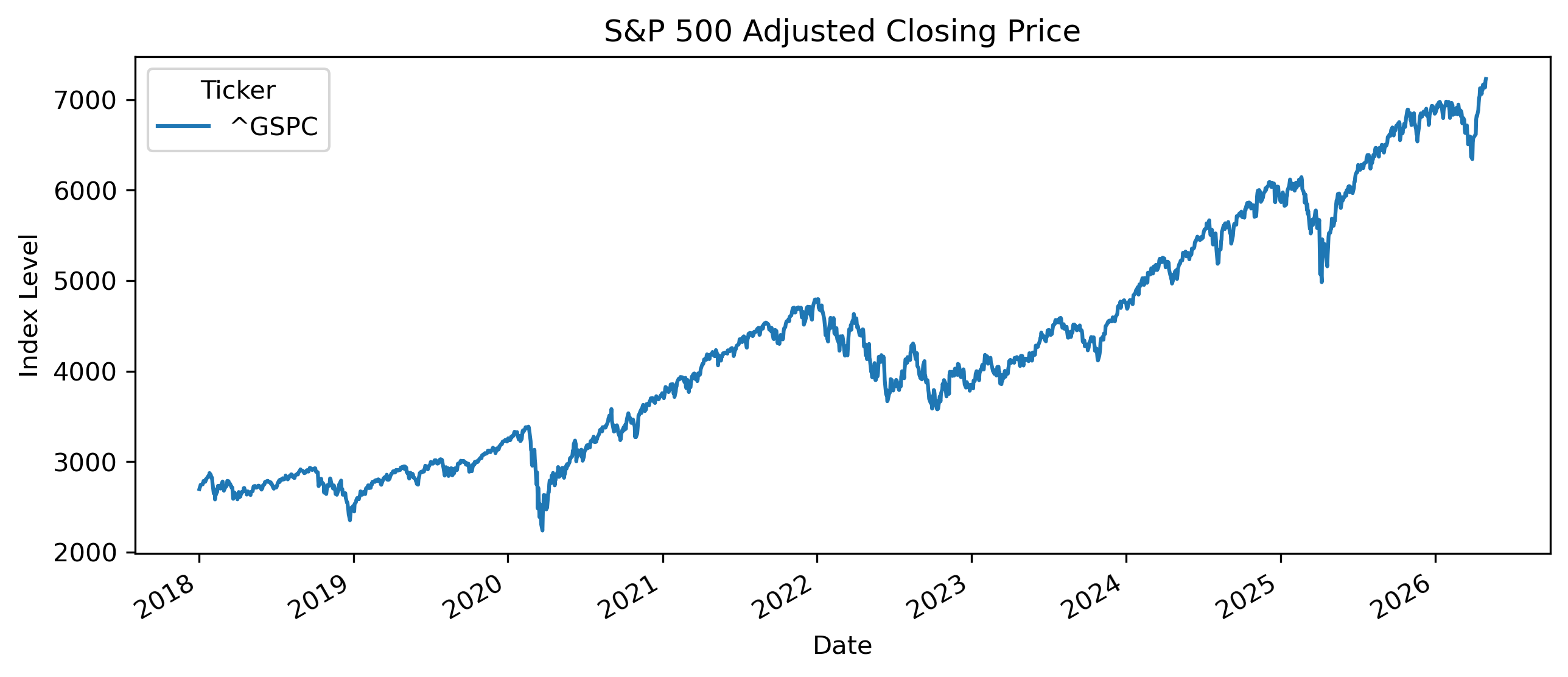

4.2 A First Example¶

We begin with a simple example using stock market data.

import yfinance as yf

import matplotlib.pyplot as plt

sp500 = yf.download("^GSPC", start="2018-01-01", auto_adjust=False)

sp500["Adj Close"].plot(figsize=(10,4))

plt.title("S&P 500 Adjusted Closing Price")

plt.xlabel("Date")

plt.ylabel("Index Level")

plt.savefig("figs/ch4/sp500.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

4.3 Components of a Time Series¶

Many time series contain several components.

A useful decomposition is:

Trend¶

A trend represents long-run movement.

Examples include:

long-run GDP growth,

rising stock market indices,

long-run inflation trends.

Cycles¶

Cycles are medium-run fluctuations around the trend.

Examples include:

business cycles,

housing cycles,

commodity cycles.

Seasonality¶

Seasonality refers to regular repeating patterns.

Examples include:

tourism seasons,

holiday shopping,

electricity demand,

agricultural harvest cycles.

Noise¶

Noise represents unpredictable random fluctuations.

4.4 Trends in Economic Data¶

Many macroeconomic variables display strong trends.

Examples include:

GDP,

population,

prices,

productivity.

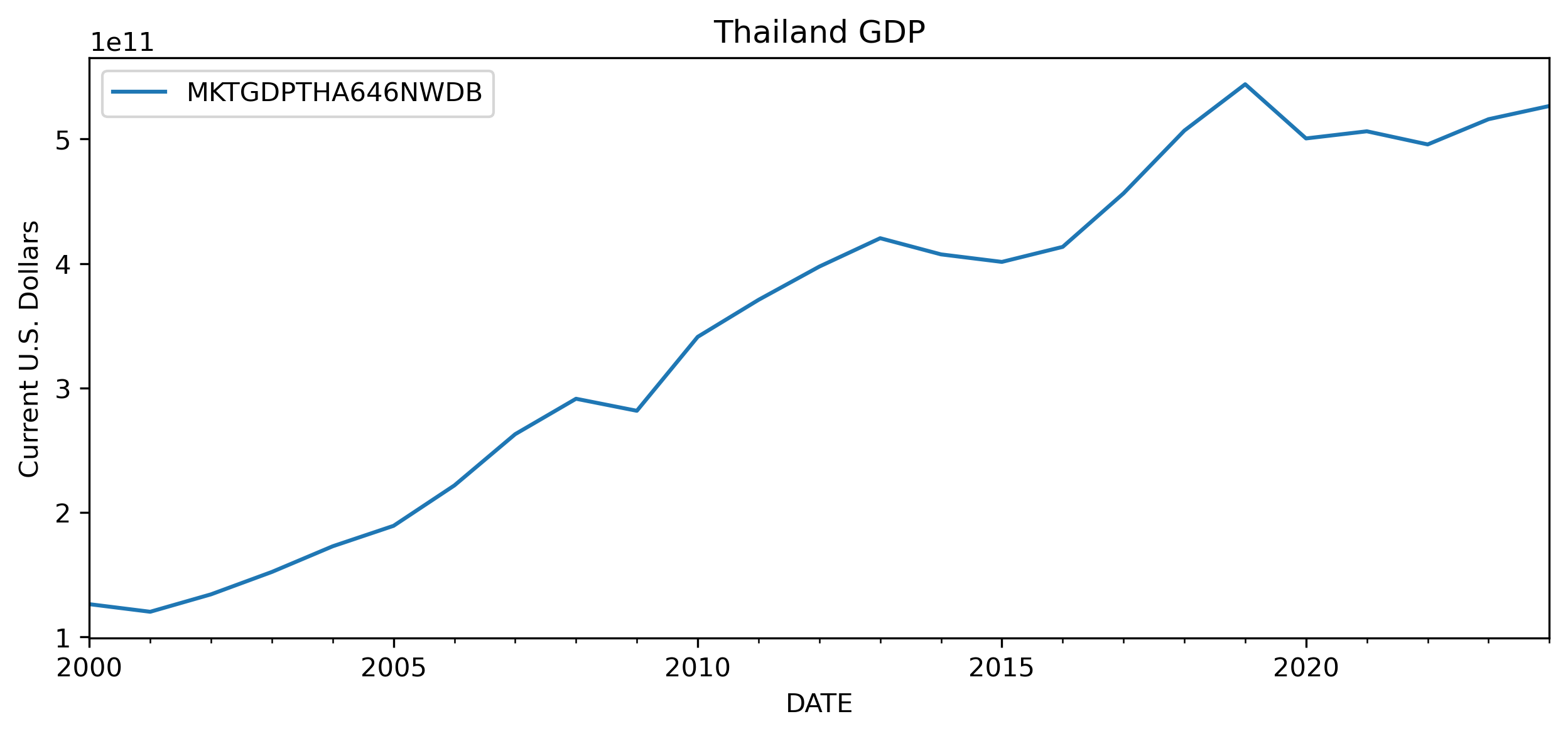

Example: GDP¶

# !pip install pandas_datareader

import pandas_datareader.data as web

import matplotlib.pyplot as plt

thai_gdp = web.DataReader(

"MKTGDPTHA646NWDB",

"fred",

start="2000-01-01"

)

thai_gdp.plot(figsize=(10,4))

plt.title("Thailand GDP")

plt.ylabel("Current U.S. Dollars")

plt.savefig("figs/ch4/thai_gdp.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

This has important implications for modeling and forecasting later in the book.

4.5 Trends vs Stationarity¶

Some time series fluctuate around relatively stable levels.

Others drift persistently upward or downward.

4.6 Seasonality¶

Seasonality refers to repeating patterns linked to the calendar.

Examples include:

higher retail sales during holidays,

tourism peaks,

electricity demand during summer,

agricultural cycles.

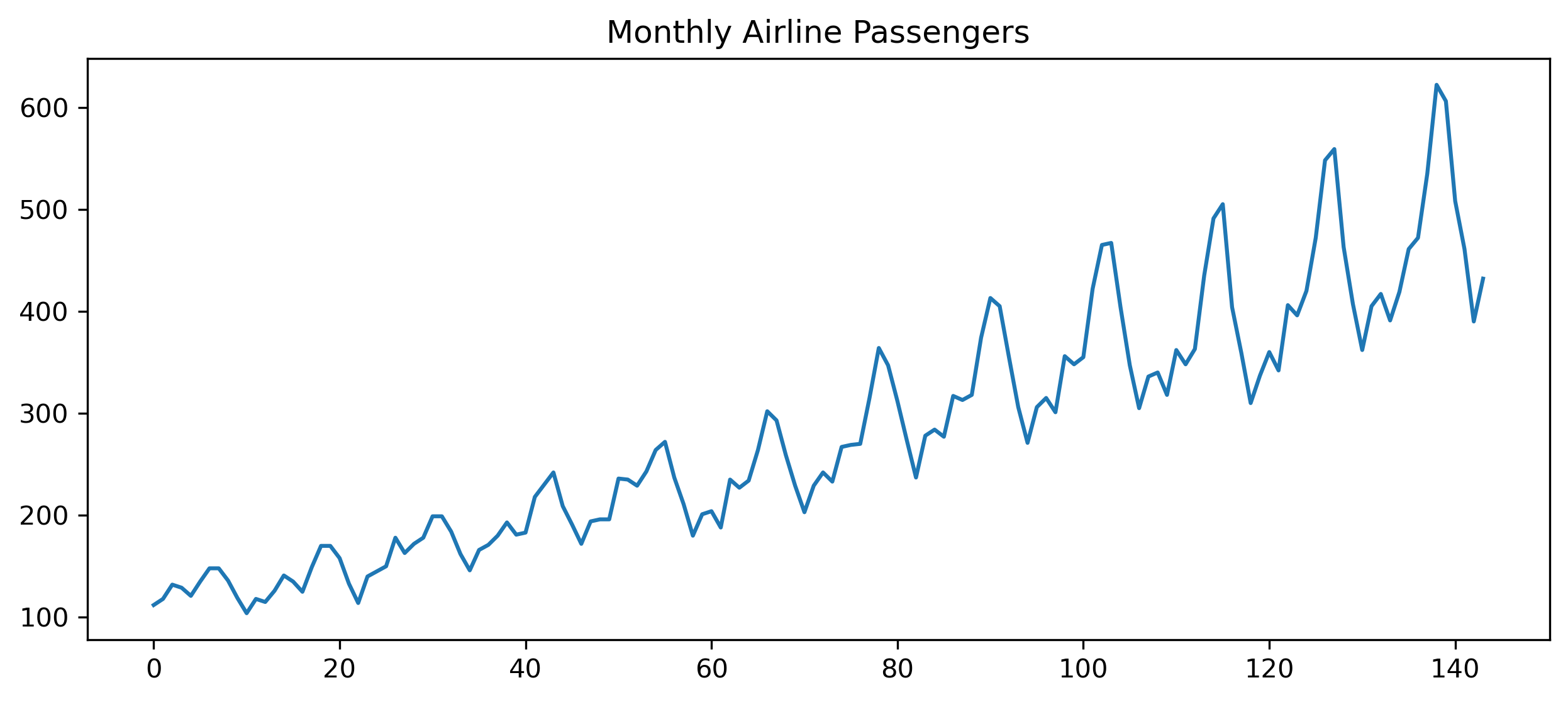

Example: Monthly Airline Passengers¶

# import matplotlib.pyplot as plt

import pandas as pd

url = "https://raw.githubusercontent.com/jbrownlee/Datasets/master/airline-passengers.csv"

df = pd.read_csv(url)

df["Passengers"].plot(figsize=(10,4))

plt.title("Monthly Airline Passengers")

plt.savefig("figs/ch4/airline.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

The fluctuations repeat systematically through time.

4.7 Cycles¶

Economic cycles differ from seasonality.

Seasonality repeats regularly.

Business cycles are more irregular.

Examples include:

recessions,

expansions,

commodity booms,

housing booms.

4.8 Noise and Random Fluctuations¶

Not all movements are meaningful.

Time series often contain substantial randomness.

This is especially important in finance.

Short-run market movements may contain substantial noise.

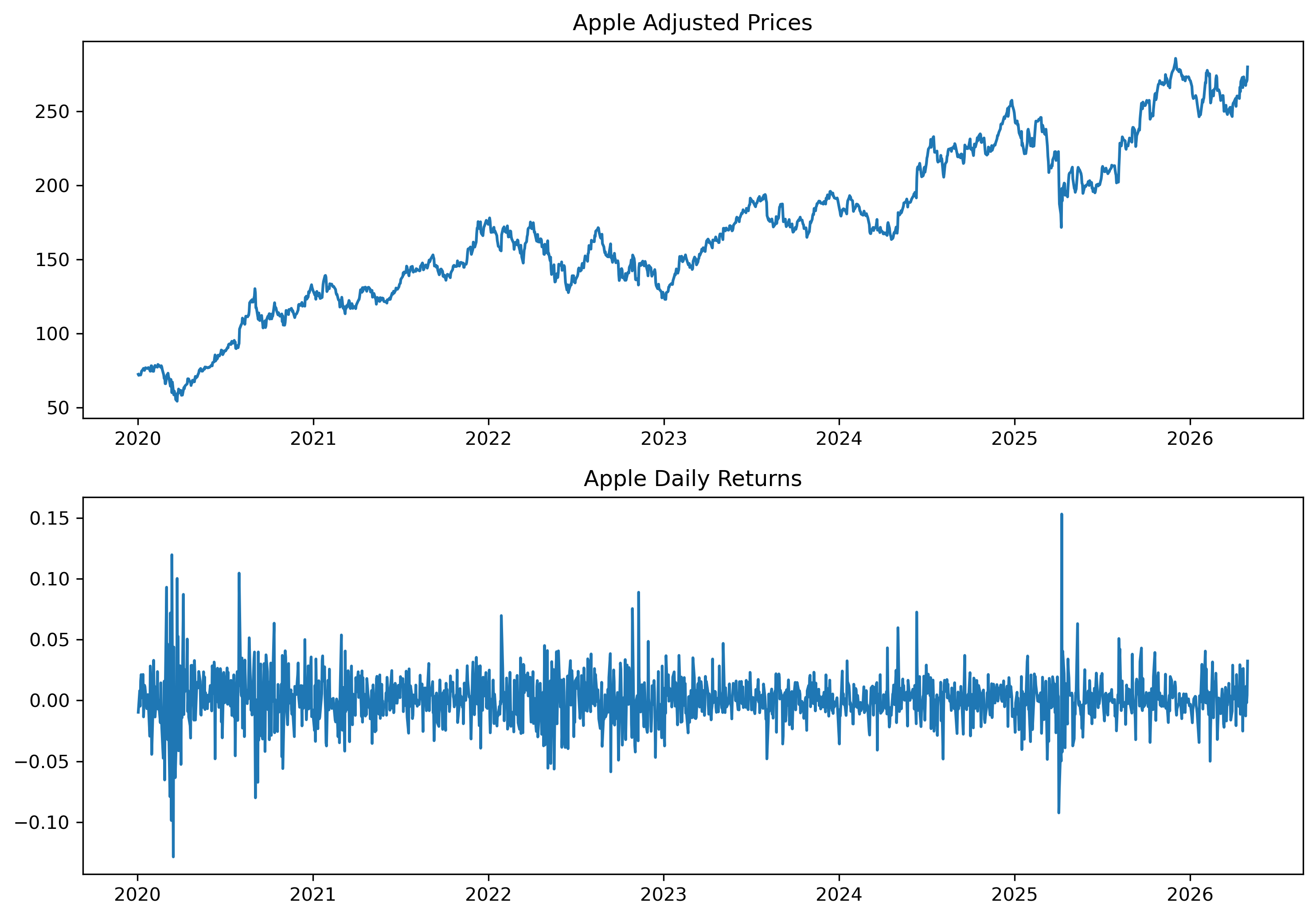

4.9 Visualizing Financial Returns¶

Prices and returns often behave very differently.

# import yfinance as yf

# import matplotlib.pyplot as plt

# import pandas as pd

aapl = yf.download("AAPL", start="2020-01-01", auto_adjust=False)

prices = aapl["Adj Close"]

returns = prices.pct_change()

fig, ax = plt.subplots(2,1, figsize=(10,7))

ax[0].plot(prices)

ax[0].set_title("Apple Adjusted Prices")

ax[1].plot(returns)

ax[1].set_title("Apple Daily Returns")

plt.tight_layout()

plt.savefig("figs/ch4/aapl.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

4.10 Volatility Clustering¶

Financial returns often display changing volatility.

Periods of calm are followed by periods of turbulence.

This phenomenon becomes central later in ARCH and GARCH models.

4.11 Structural Breaks¶

Some time series experience sudden changes.

These are called structural breaks.

Examples include:

financial crises,

policy regime changes,

pandemics,

wars.

Example¶

The COVID-19 pandemic caused dramatic movements in:

stock prices,

unemployment,

GDP,

exchange rates.

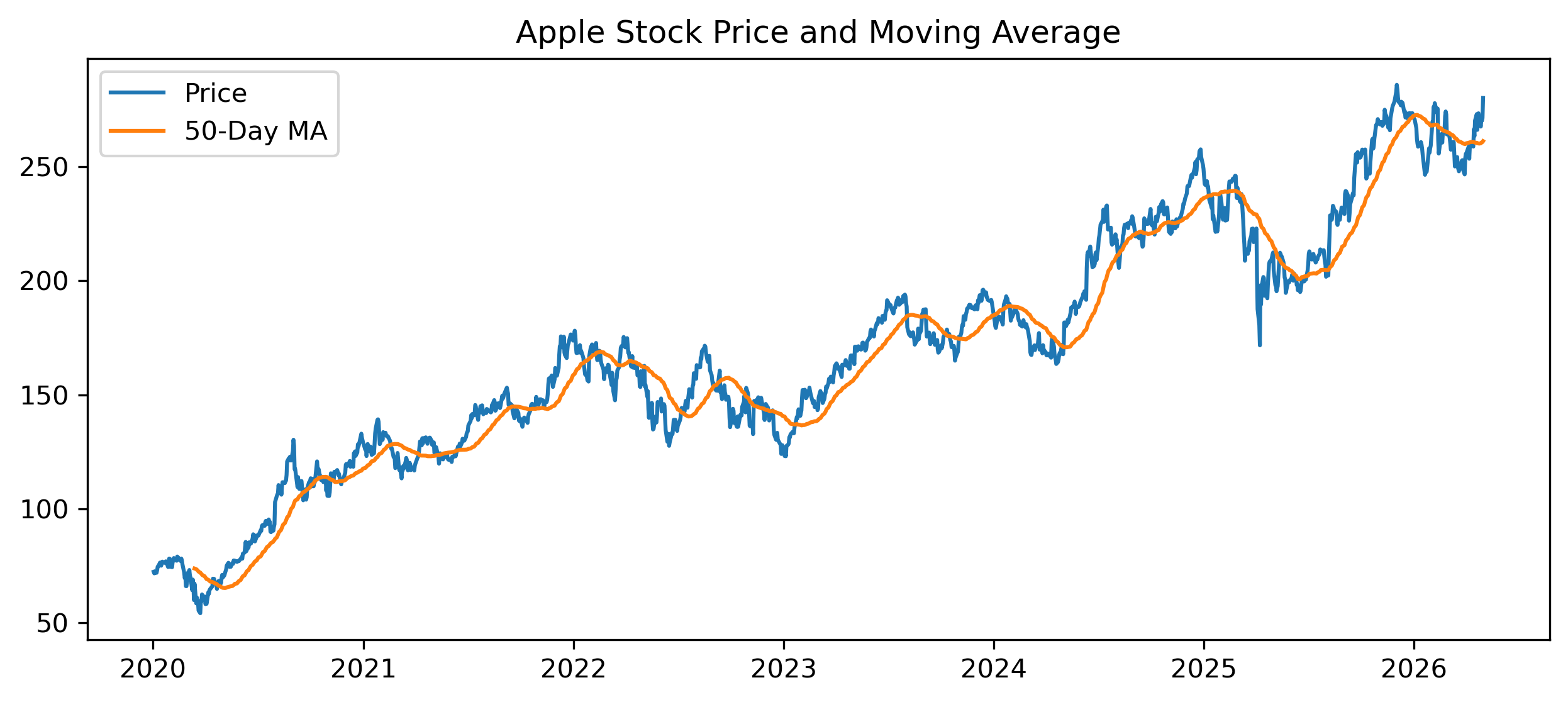

4.12 Rolling Averages¶

A rolling average smooths short-run fluctuations.

This helps reveal longer-run patterns.

Simple Rolling Average¶

A rolling average over periods is:

Example¶

# import yfinance as yf

# import matplotlib.pyplot as plt

aapl = yf.download("AAPL", start="2020-01-01", auto_adjust=False)

prices = aapl["Adj Close"]

ma50 = prices.rolling(50).mean()

plt.figure(figsize=(10,4))

plt.plot(prices, label="Price")

plt.plot(ma50, label="50-Day MA")

plt.legend()

plt.title("Apple Stock Price and Moving Average")

plt.savefig("figs/ch4/rolling.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

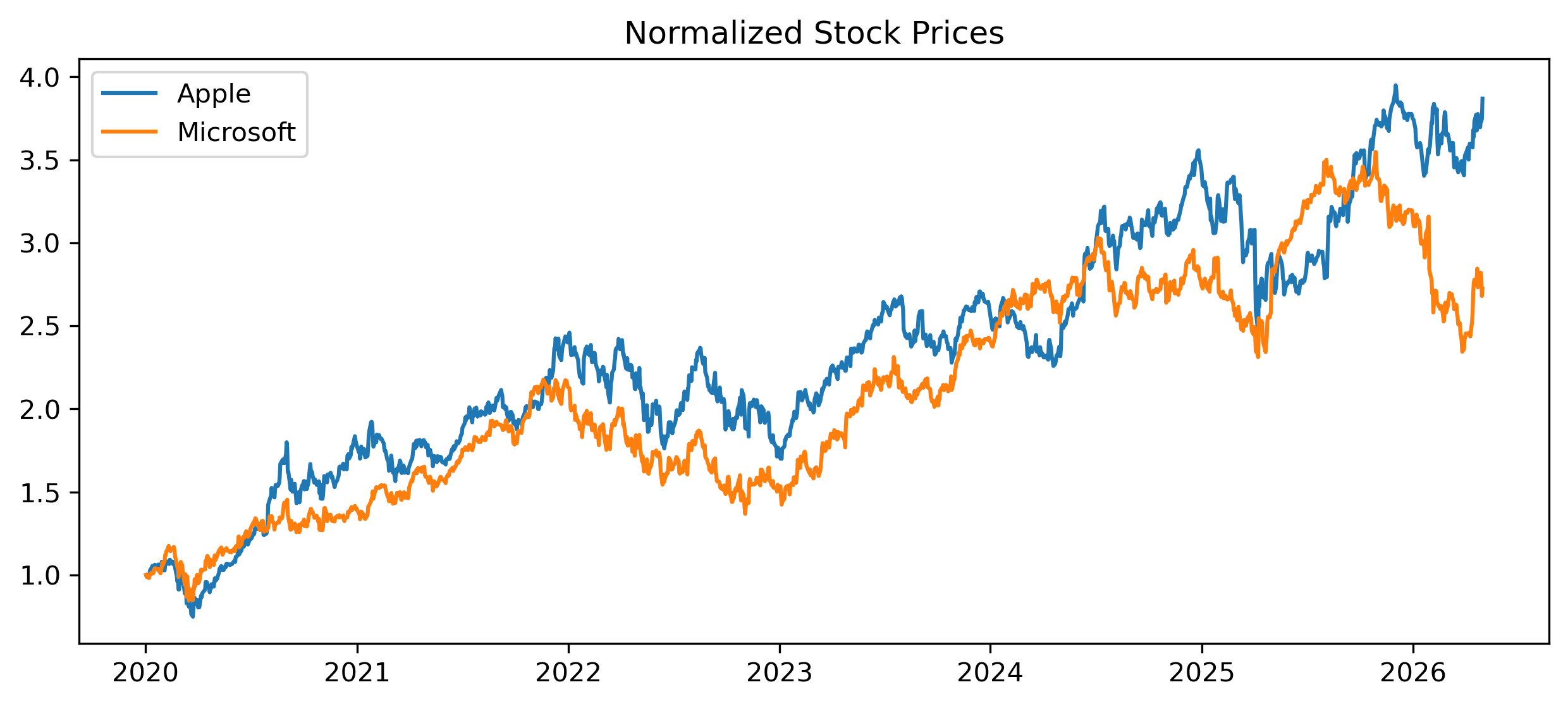

4.13 Comparing Multiple Series¶

Visualization also helps compare multiple variables.

# import yfinance as yf

# import matplotlib.pyplot as plt

aapl = yf.download("AAPL", start="2020-01-01", auto_adjust=False)["Adj Close"]

msft = yf.download("MSFT", start="2020-01-01", auto_adjust=False)["Adj Close"]

plt.figure(figsize=(10,4))

plt.plot(aapl / aapl.iloc[0], label="Apple")

plt.plot(msft / msft.iloc[0], label="Microsoft")

plt.legend()

plt.title("Normalized Stock Prices")

plt.savefig("figs/ch4/twostocks.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

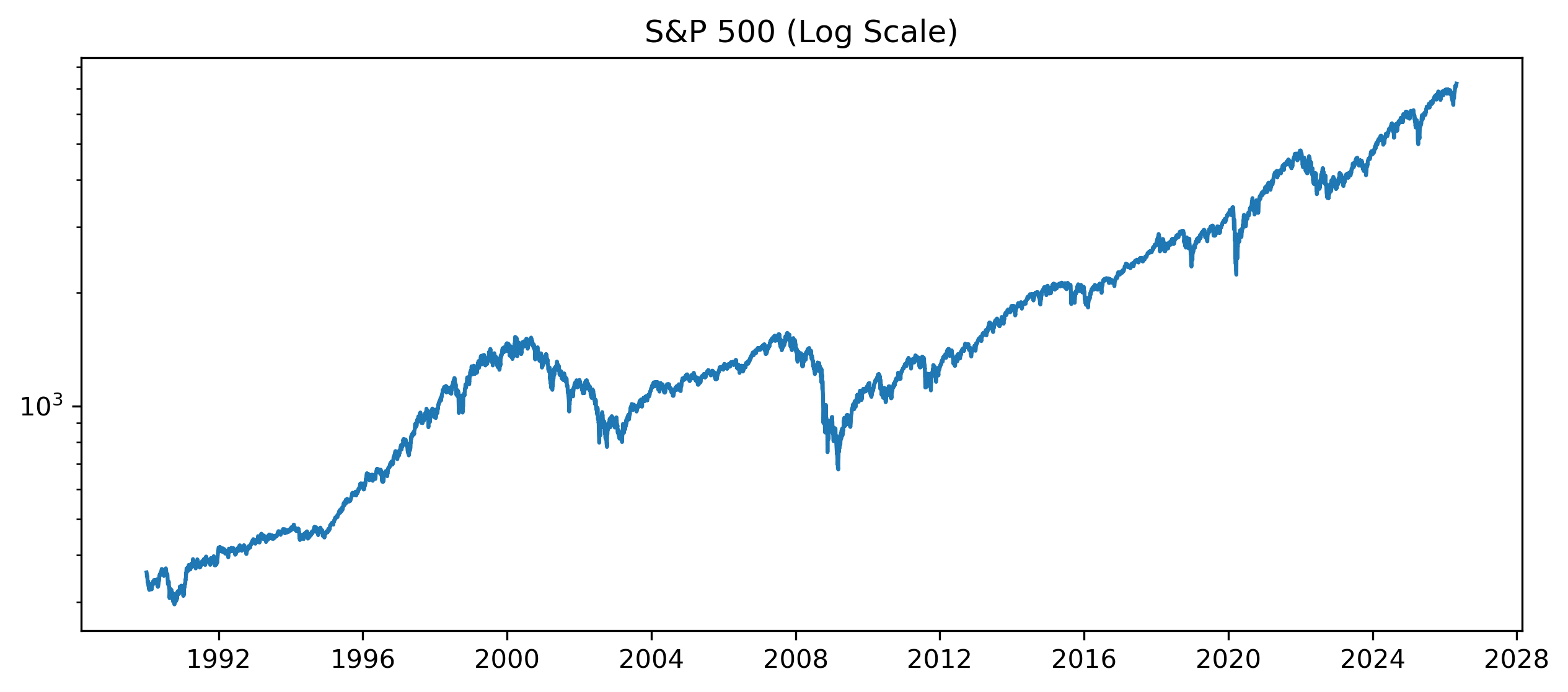

4.14 Log Scales¶

Some time series grow exponentially over long periods.

In such cases, log scales can improve interpretation.

Example¶

# import yfinance as yf

# import matplotlib.pyplot as plt

sp500 = yf.download("^GSPC", start="1990-01-01", auto_adjust=False)

plt.figure(figsize=(10,4))

plt.plot(sp500["Adj Close"])

plt.yscale("log")

plt.title("S&P 500 (Log Scale)")

plt.savefig("figs/ch4/logscale.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

4.15 Visualization and Forecasting¶

Good forecasting begins with understanding the data visually.

Plots may reveal:

trends,

persistence,

seasonality,

changing volatility,

structural breaks.

These features influence model selection later.

4.16 Gretl Example: Plotting a Time Series¶

Gretl provides simple visualization tools.

Step 1 — Open Data¶

Menu:

File → Open dataStep 2 — Plot a Variable¶

Select a variable and choose:

Variable → Time series plot[GRETL Screenshot Placeholder: Time series plot]Step 3 — Add Moving Average¶

Menu:

Add → Moving average[GRETL Screenshot Placeholder: Moving average plot]4.17 Common Mistakes¶

4.18 Looking Ahead¶

This chapter introduced visual exploration of time series data.

The next chapter studies smoothing and trend estimation more formally.

We will examine:

moving averages,

exponential smoothing,

Holt models,

HP filters,

and trend extraction.

Key Takeaways¶

Concept Check¶

Basic¶

What is the purpose of plotting a time series?

What is a trend?

What is a cycle?

Intuition¶

Why is visualization often the first step in time series analysis?

How can a plot help detect patterns that summary statistics cannot?

What is the difference between signal and noise?

Intermediate¶

What does a moving average do to a time series?

Why does smoothing help reveal underlying patterns?

What is the trade-off between smoothing and responsiveness?

Challenge¶

Suppose a time series appears smooth after applying a moving average.

What information might be lost?

Why might this matter for forecasting or trading?

Interpretation & Practice¶

You observe a time series plot with a steady upward movement.

What feature does this suggest?

Why might this create problems for analysis later?

A time series fluctuates randomly around a constant level.

What type of behavior does this suggest?

What might be a suitable model for this?

A time series shows long periods of calm followed by sudden large movements.

What feature of financial data does this illustrate?

Why is this important?

A smoothed series (moving average) lags behind the original data.

Why does this happen?

When might this be a problem?

Challenge¶

Two analysts use different moving averages:

Analyst A: 5-day MA

Analyst B: 50-day MA

Which one reacts faster to new information?

Which one is smoother?

Which one would be better for short-term trading?

Numerical Practice¶

Visual Thinking¶

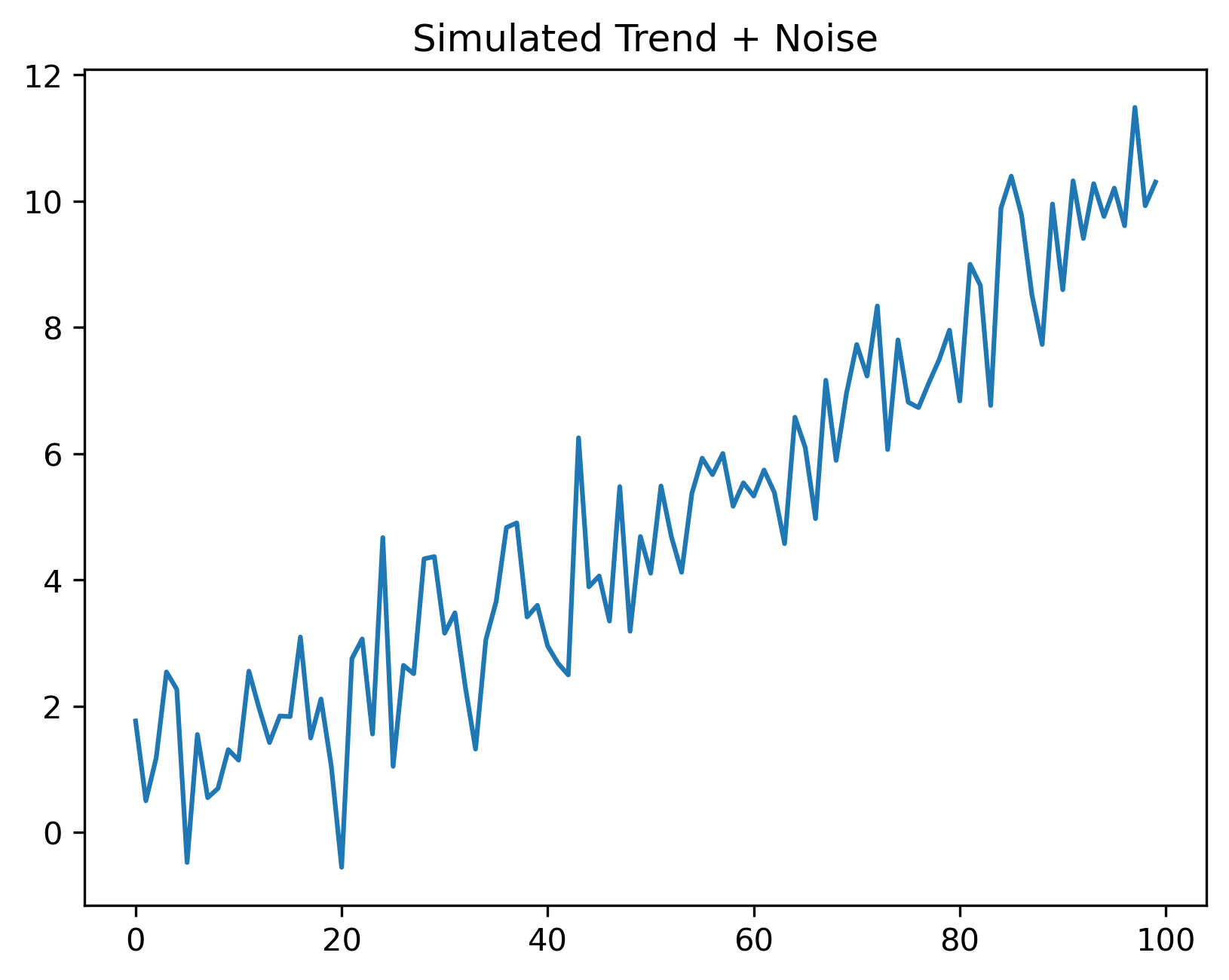

Consider the following simulated time series:

Source

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(0)

t = np.arange(100)

trend = 0.1 * t

noise = np.random.normal(0, 1, 100)

series = trend + noise

plt.plot(series)

plt.title("Simulated Trend + Noise")

plt.savefig("figs/ch3/Q_trent.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

What two components can you identify?

Which part represents signal? Which part represents noise?

Smoothing a Stationary Series¶

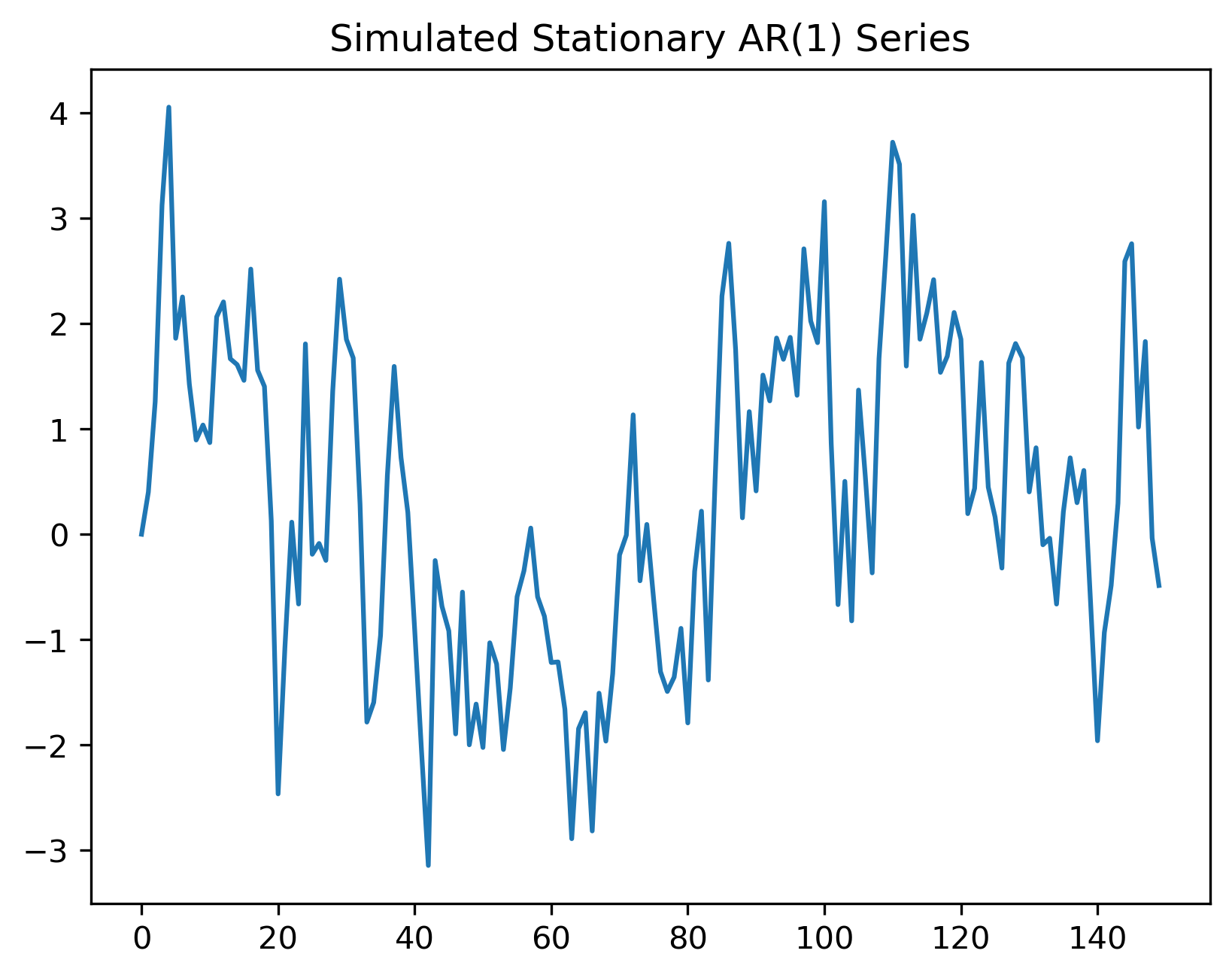

Simulate a stationary AR(1) series:

Source

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(0)

T = 150

phi = 0.7

e = np.random.normal(0, 1, T)

series = np.zeros(T)

for t in range(1, T):

series[t] = phi * series[t-1] + e[t]

plt.plot(series)

plt.title("Simulated Stationary AR(1) Series")

plt.savefig("figs/ch3/Q_ar1.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Does the series have a deterministic trend?

Does it still show persistence?

How is this different from pure white noise?

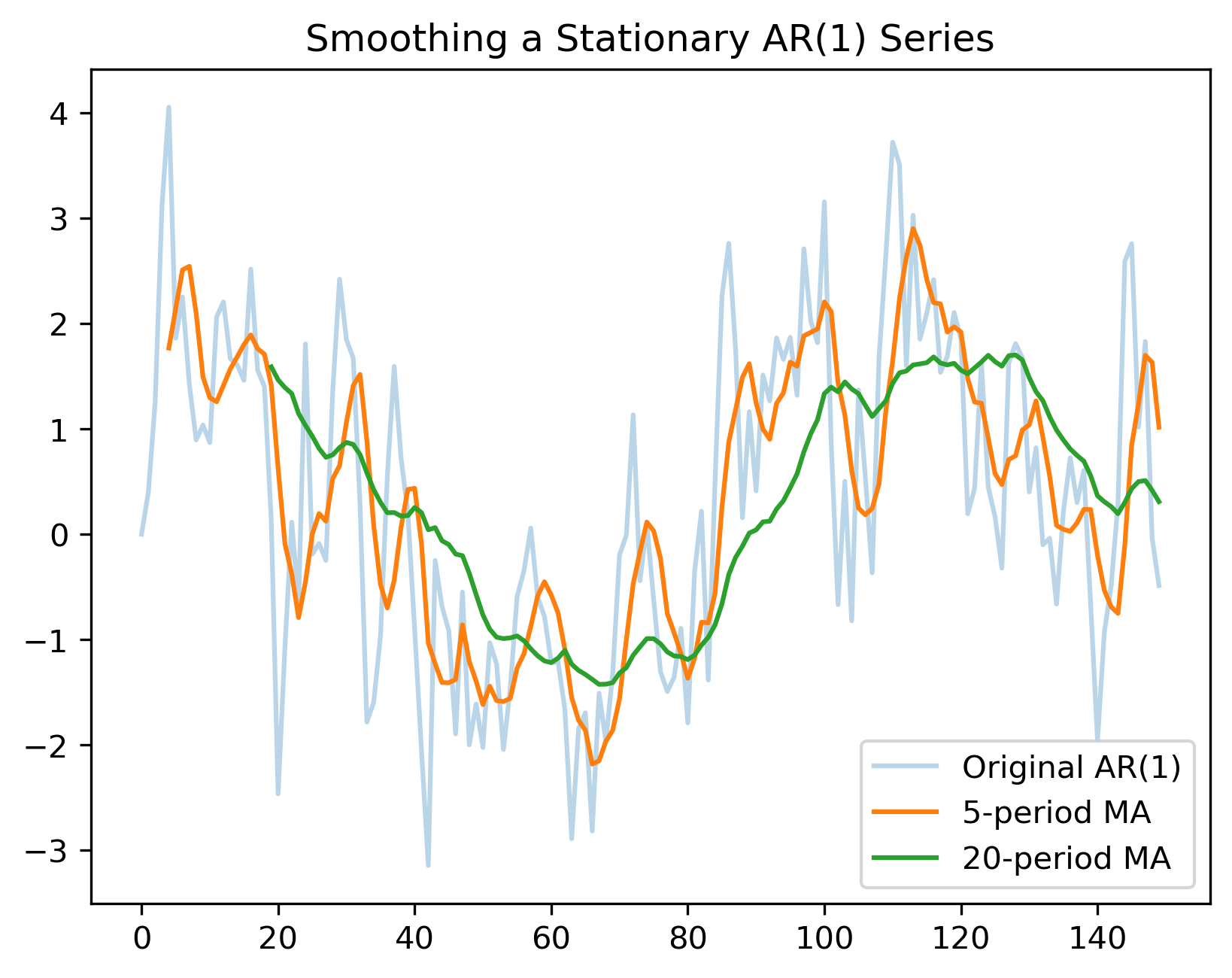

Apply moving averages to the AR(1) series:

Source

ma_short = np.convolve(series, np.ones(5)/5, mode="valid")

ma_long = np.convolve(series, np.ones(20)/20, mode="valid")

plt.plot(series, alpha=0.3, label="Original AR(1)")

plt.plot(

range(4, T),

ma_short,

label="5-period MA"

)

plt.plot(

range(19, T),

ma_long,

label="20-period MA"

)

plt.legend()

plt.title("Smoothing a Stationary AR(1) Series")

plt.savefig("figs/ch3/Q_ar1_ma.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Which moving average is smoother?

Which responds faster to changes?

What is the danger of smoothing too heavily?