Part VIII Capstone — Forecasting Volatility and Financial Risk

In Part VIII, we studied models for time-varying volatility:

ARCH models,

GARCH models,

volatility clustering,

conditional variance,

and volatility forecasting.

This capstone applies these ideas to daily financial returns.

We use SPY, an ETF tracking the S&P 500.

Exercise 1 — Download Price Data¶

import yfinance as yf

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

spy = yf.download(

"SPY",

start="2015-01-01",

auto_adjust=False

)

prices = spy["Adj Close"].squeeze()

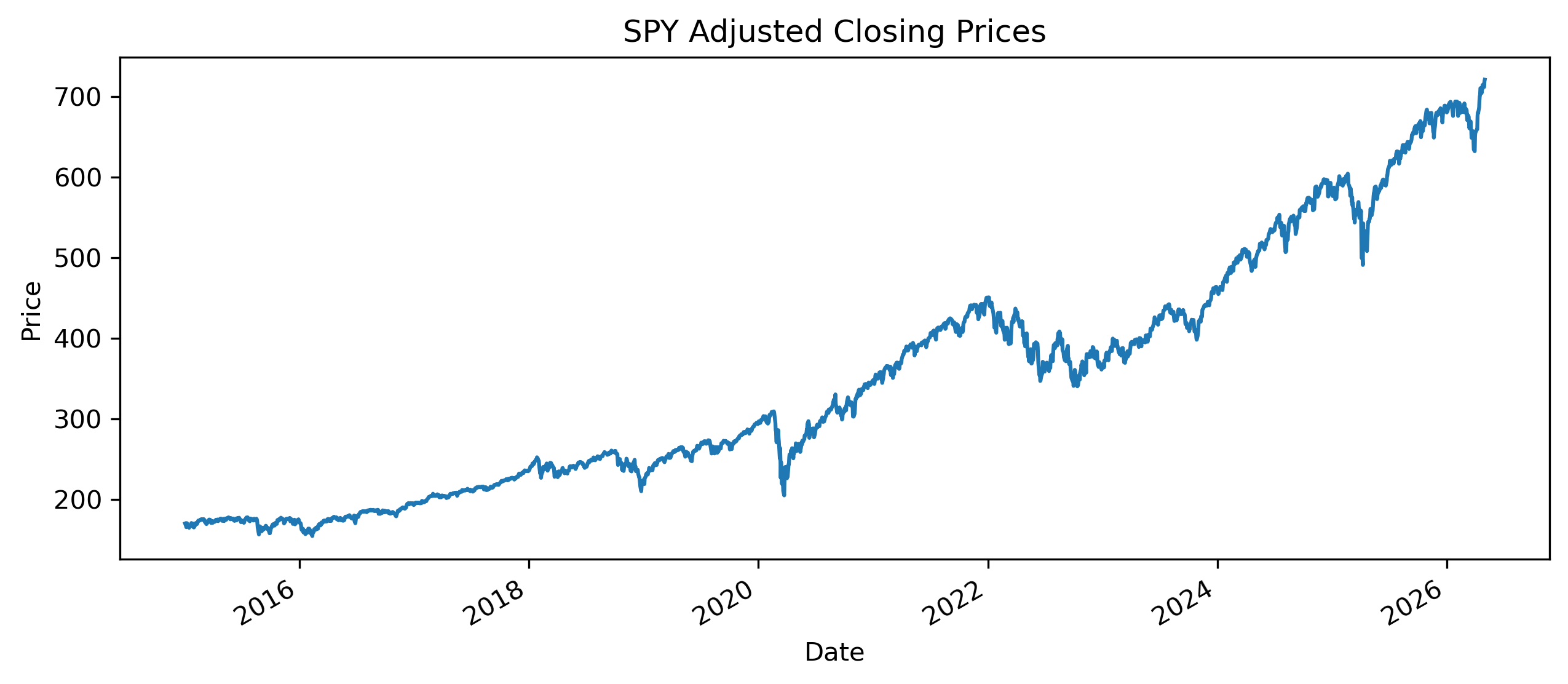

prices.plot(figsize=(10,4))

plt.title("SPY Adjusted Closing Prices")

plt.ylabel("Price")

plt.xlabel("Date")

plt.savefig("figs/ch26_/SPY.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Exercise 2 — Compute Log Returns¶

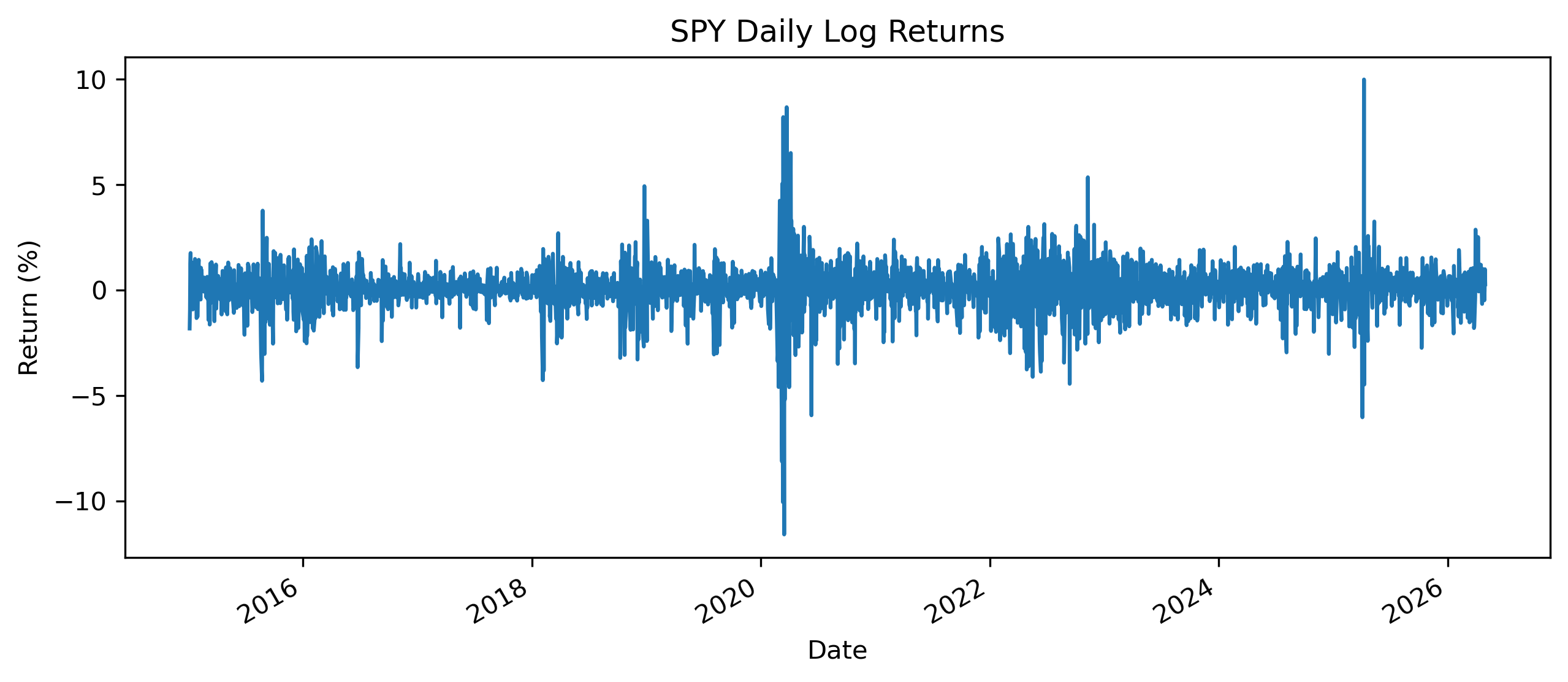

returns = 100 * np.log(

prices / prices.shift(1)

)

returns = returns.dropna()

returns.plot(figsize=(10,4))

plt.title("SPY Daily Log Returns")

plt.ylabel("Return (%)")

plt.xlabel("Date")

plt.savefig("figs/ch26_/rtn.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Exercise 3 — Rolling Volatility¶

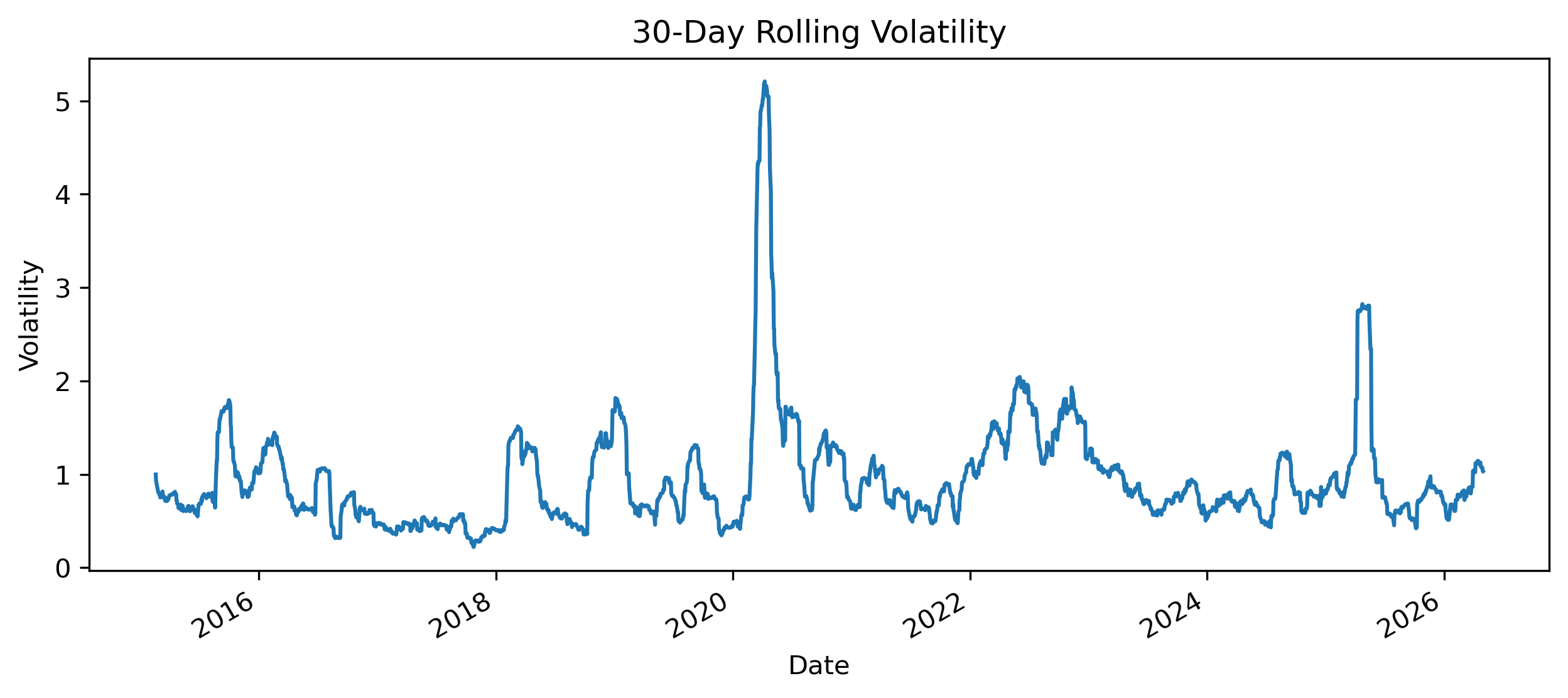

rolling_vol = returns.rolling(30).std()

rolling_vol.plot(figsize=(10,4))

plt.title("30-Day Rolling Volatility")

plt.ylabel("Volatility")

plt.xlabel("Date")

plt.savefig("figs/ch26_/rol_vol.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Exercise 4 — Testing for ARCH Effects¶

from statsmodels.stats.diagnostic import het_arch

arch_test = het_arch(

returns,

nlags=10

)

print("LM Statistic:", arch_test[0])

print("LM Test p-value:", arch_test[1])

print("F Statistic:", arch_test[2])

print("F Test p-value:", arch_test[3])LM Statistic: 848.0078628375993

LM Test p-value: 9.790554714049502e-176

F Statistic: 120.46872866846164

F Test p-value: 1.6667139182935798e-209Exercise 5 — Install and Load the ARCH Package¶

Exercise 6 — Estimate a GARCH(1,1) Model¶

from arch import arch_model

garch_model = arch_model(

returns,

mean="Constant",

vol="GARCH",

p=1,

q=1,

dist="normal"

)

garch_results = garch_model.fit(

disp="off"

)

print(garch_results.summary()) Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: SPY R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: -3671.36

Distribution: Normal AIC: 7350.72

Method: Maximum Likelihood BIC: 7374.53

No. Observations: 2848

Date: Sun, May 03 2026 Df Residuals: 2847

Time: 23:25:08 Df Model: 1

Mean Model

==========================================================================

coef std err t P>|t| 95.0% Conf. Int.

--------------------------------------------------------------------------

mu 0.0851 1.401e-02 6.079 1.208e-09 [5.769e-02, 0.113]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 0.0405 1.034e-02 3.918 8.926e-05 [2.026e-02,6.081e-02]

alpha[1] 0.1764 2.711e-02 6.508 7.629e-11 [ 0.123, 0.230]

beta[1] 0.7907 2.803e-02 28.213 4.059e-175 [ 0.736, 0.846]

============================================================================

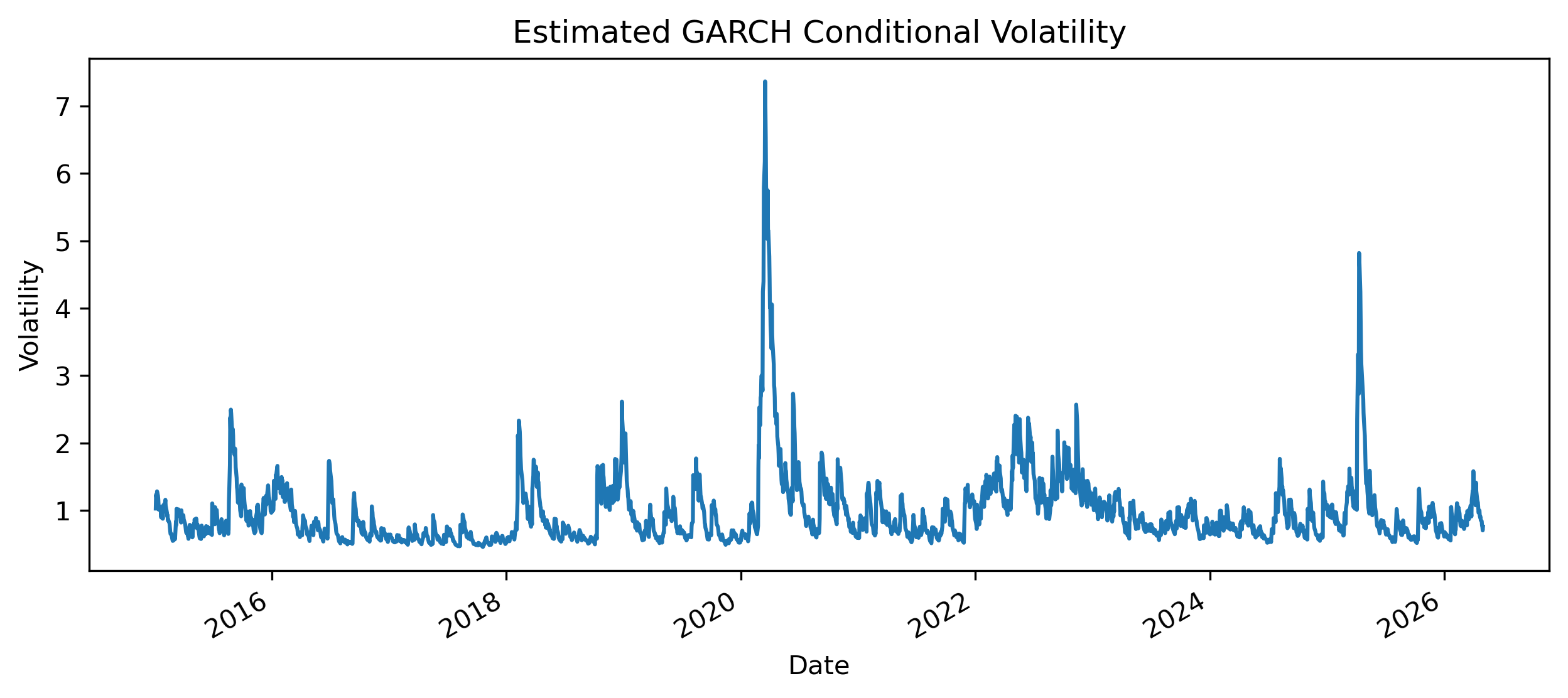

Covariance estimator: robustExercise 7 — Plot Conditional Volatility¶

conditional_vol = garch_results.conditional_volatility

conditional_vol.plot(figsize=(10,4))

plt.title("Estimated GARCH Conditional Volatility")

plt.ylabel("Volatility")

plt.xlabel("Date")

plt.savefig("figs/ch26_/garch11.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

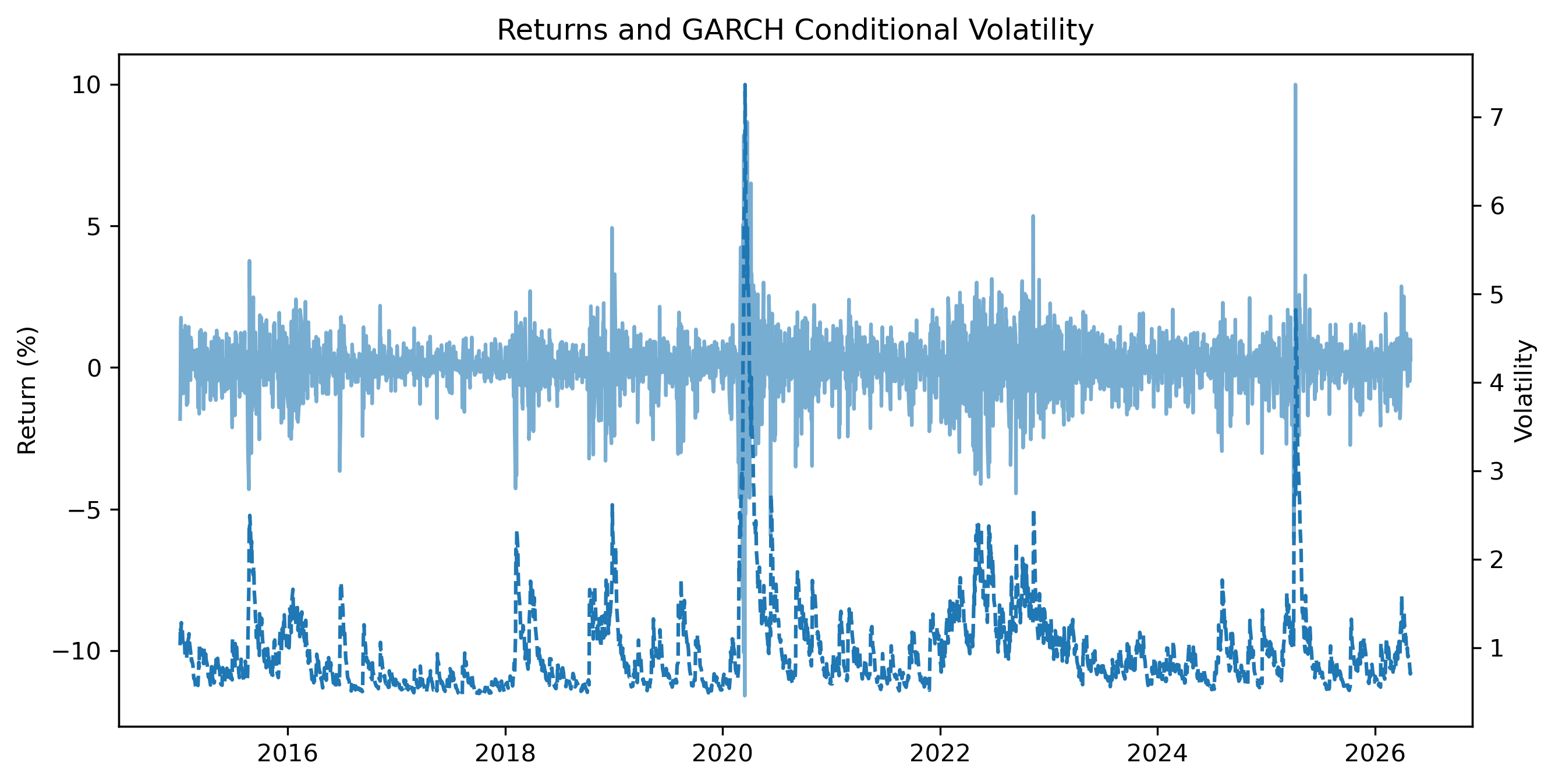

Exercise 8 — Compare Returns and Conditional Volatility¶

fig, ax1 = plt.subplots(figsize=(10,5))

ax1.plot(

returns,

label="Returns",

alpha=0.6

)

ax1.set_ylabel("Return (%)")

ax2 = ax1.twinx()

ax2.plot(

conditional_vol,

label="Conditional Volatility",

linestyle="--"

)

ax2.set_ylabel("Volatility")

plt.title("Returns and GARCH Conditional Volatility")

plt.savefig("figs/ch26_/garch11_r.png", dpi=300, bbox_inches="tight")

plt.close() # replace with plt.show()

Exercise 9 — Forecast Volatility¶

forecast = garch_results.forecast(

horizon=10

)

variance_forecast = forecast.variance.iloc[-1]

vol_forecast = np.sqrt(variance_forecast)

vol_forecasth.01 0.708746

h.02 0.725500

h.03 0.741344

h.04 0.756351

h.05 0.770588

h.06 0.784110

h.07 0.796971

h.08 0.809214

h.09 0.820882

h.10 0.832011Exercise 10 — Plotting Recent Volatility and the Forecast¶

We now compare:

recent estimated volatility,

and the 10-day ahead volatility forecast.

This helps visualize how GARCH models project volatility into the future.

# ==========================================

# Extract recent volatility history

# ==========================================

recent_vol = conditional_vol.iloc[-100:]

# ==========================================

# Forecast future volatility

# ==========================================

forecast = garch_results.forecast(

horizon=10

)

forecast_var = forecast.variance.iloc[-1]

forecast_vol = np.sqrt(forecast_var)

# ==========================================

# Construct forecast index

# ==========================================

forecast_index = range(

len(recent_vol),

len(recent_vol) + len(forecast_vol)

)

# ==========================================

# Plot

# ==========================================

plt.figure(figsize=(10,5))

# Historical volatility

plt.plot(

range(len(recent_vol)),

recent_vol,

label="Historical Volatility",

linewidth=2

)

# Forecast volatility

plt.plot(

forecast_index,

forecast_vol,

label="Forecast Volatility",

linewidth=2,

linestyle="--"

)

plt.title("Recent and Forecast GARCH Volatility")

plt.ylabel("Volatility")

plt.xlabel("Time")

plt.legend()

plt.show()Exercise 11 — Simple Value-at-Risk¶

We compute a simple one-day 5% Value-at-Risk.

latest_vol = conditional_vol.iloc[-1]

var_5 = -1.645 * latest_vol

print("One-day 5% VaR:", var_5)One-day 5% VaR: -1.2482842037087853Exercise 12 — Common Mistakes¶

Key Takeaways¶